The list of high quality bidding units in South China for SMM in 2021 has been announced! You are invited to witness the licensing ceremony.

At the 2021 (9th) Silicon Industry Summit solemnly held by SMM, Zhang Lei, chief of new energy for power equipment of Shanghai Shenyin Wanguo Securities Research Institute, mainly accelerated investment in all aspects of the industry chain from the photovoltaic system high-profile racetrack; medium-and short-term silicon supply and demand is tight balance, long-term capacity release price is expected to fall; dual control policy to enhance energy control requirements, granular silicon is expected to become a breakthrough; N-type battery promotes the upgrading of product quality, and the high purification of silicon material is interpreted in several aspects.

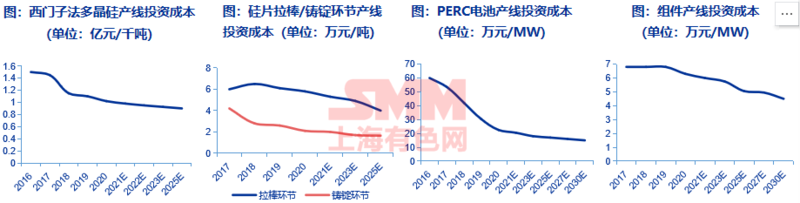

Localization and technological progress have greatly reduced the cost of investment in all links.

The localization of equipment in all links has basically achieved a substantial reduction in investment costs.

Silicon material link: production equipment technology and technology are constantly improving. In 2020, the equipment investment cost of trichlorosilicon Siemens polysilicon production line has been reduced to 102 million yuan / kiloton, a decrease of 7.27% compared with the same period last year.

Silicon wafer link: in 2020, the investment cost of drawing rod and ingot link equipment (including machine processing link) was 58000 yuan / ton and 21000 yuan / ton respectively, down 4.92% and 19.23% respectively compared with the same period last year.

Battery chip link: the key equipment of China's conventional battery production line has basically been localized, and the investment cost of PERC battery production line in 2020 has been reduced to 225000 yuan / MW, down 25.74% from the same period last year.

Component link: all domestic component production equipment has been localized, and the investment in new production line equipment in 2020 is 63000 yuan / MW, down 7.35% from the same period last year. The investment cost of each link of the production line is expected to be further reduced in the future.

The investment intensity of the photovoltaic industry chain significantly increases the new production capacity and accelerates the landing.

The high scene of terminal installation has led to a steady increase in investment in the overall photovoltaic industry chain. Terminal demand promotes all manufacturers in the industrial chain to actively invest and expand production, and the capital expenditure of manufacturers in all links has increased significantly since 2017. In 2020, the cash flow of Longji, Tongwei, Central, Tianhe, Jingao and other leading enterprises purchasing fixed / intangible assets reached 4.83 billion yuan, 5.49 billion yuan, 3.66 billion yuan, 2.02 billion yuan and 3.2 billion yuan respectively.

Benefit from photovoltaic installation with high scenery, the demand for polysilicon is expected to increase.

The demand for polysilicon benefits from the increased demand for photovoltaic installations, and the total demand is expected to reach 1.102 million tons in 2025. From 2021 to 2023, the total demand for newly installed 160GW, 200GW and 240GW materials in the world from 2021 to 2023 is 611000 tons, 756000 tons and 899000 tons respectively. It is estimated that by 2025, the global demand for polysilicon will reach 1.102 million tons, and the five-year CAGR will be about 17.4%.

Short-term silicon materials maintain tight balance and push up prices to an all-time high

The chemical property of polysilicon industry is strong, and the short-term supply and demand structure maintains a tight balance. Due to the long production expansion cycle brought about by the chemical properties of silicon materials, it is expected that polysilicon supply and demand will maintain a tight balance in 2021, with an overall effective capacity of about 640000 tons and an annual effective capacity utilization rate of about 96%.

Tight supply and demand pushed up the price of polysilicon, reaching an all-time high in 2021. Since the silicon material accident in the second half of 2020, the price of silicon material has continued to rise, the high price of silicon material caused by the accident has raised the expectation of the price downstream, and the mismatch between supply and demand caused by the outbreak of photovoltaic demand has been superimposed. The price of silicon material has continued to rise in 2021. As of September 2021, the price of polysilicon densifier reached 214 yuan / kg,. Compared with January 2020, the price of polysilicon densifier has increased by 193%. Considering that the pace of capacity release can not effectively ease the relationship between supply and demand in the short term, polysilicon prices are expected to remain relatively high in 2021.

Medium-and long-term supply and demand structure is expected to balance prices are expected to fall gradually

The new production capacity of polysilicon is put on schedule, and the price of silicon is expected to meet the inflection point. Polysilicon is expected to maintain tight supply and demand in 2022. It is estimated that the utilization rate of effective capacity of 2022Q1-Q4 is 83%, 75%, 77% and 89% respectively, and about 86% for the whole year of 2022. With the gradual release of production capacity, the tight situation of supply and demand will gradually ease after 2023. According to estimates, the utilization rate of effective capacity from 2023 to 2025 is about 65%, 63% and 64%, respectively. Prices are expected to gradually fall back to a reasonable range despite the improvement in the structure of supply and demand.

Strict policy of double control of energy consumption polysilicon manufacturers need to continue to save energy and reduce consumption

The energy consumption of polysilicon production is expected to continue to decline. Reducing the core concerns and long-term development direction of polysilicon links in the department, in recent years, manufacturers have gradually improved energy efficiency, thereby reducing comprehensive production energy consumption and overall production costs, and the unit production cost has been reduced from 60 yuan / kg in 2016 to 40-42 yuan / kg at the end of 2020. At present, the comprehensive energy consumption of the improved Siemens method is about 11kgce/kg-Si, and there will be a decline space of 1kgce/kg-Si in the next 2-3 years. By 2030, the reduction power consumption and comprehensive power consumption of the improved Siemens process are expected to decrease from 49 kWh/kg-Si,66.5 kWh/kg-Si in 2020 to 44 kWh/kg-Si,60 kWh/kg-Si, in 2020 to further reduce the cost of polysilicon preparation.

N-type battery is expected to become the mainstream technology to break through the efficiency bottleneck.

N-type battery breaks through the bottleneck of efficiency and is expected to become the mainstream technology in the future. N-type monocrystalline silicon battery has the advantages of high minority carrier lifetime, no light-induced attenuation, good weak light effect, low temperature coefficient and so on. With the gradual localization of equipment to achieve cost reduction, the market acceptance of N-type batteries is expected to increase year by year. According to ITRPV2019 estimates, the permeability of N-type batteries is about 5.22% in 2019, 14.11% in 2022, and is expected to exceed 25% in 2030, becoming one of the mainstream technology directions in the market.

Battery manufacturers actively layout N-type battery capacity

Battery manufacturer N-type battery capacity layout opened. N-type battery has high conversion efficiency and high double-sided performance-price ratio. The representative technical routes include N-TOPCon and N-HIT (heterojunction). Longji shares plan to issue convertible bonds in 2021 to raise 7 billion yuan for the construction of 18GW single crystal efficient battery, the project also uses N-type high-efficiency single crystal battery technology; Tongwei shares for Meishan Phase 2 and Jintang Phase 1 total 15GW battery projects have reserved the location of N-type TOPCon equipment upgrading; Zhonglai shares of the N-type TOPCon battery project is actively under way.

Domestic manufacturers actively expand the production capacity of electronic-grade polysilicon

Domestic manufacturers actively promote the localization of electronic-grade polysilicon. The "made in China 2025" plan proposes that the core basic components and key basic materials of semiconductors should be guaranteed by 40% by 2020, and the self-sufficiency rate should reach 70% by 2025. By the end of 2020, the main domestic electronic-grade polysilicon manufacturers include Jiangsu Xinhua 5000 tons, Yellow River hydropower 3300 tons, Tianhong Ruike 1000 tons and so on, with a total production capacity of more than 15000 tons per year. At the same time, a number of leading enterprises in the field of polysilicon have launched electronic-grade polysilicon projects with an annual production capacity of 30000 tons, Daquan Energy A-share IPO raised funds to build 1000 tons of semiconductor-grade polysilicon, and new special energy expansion projects totaling 100000 tons all meet the requirements of electronic-grade applications.