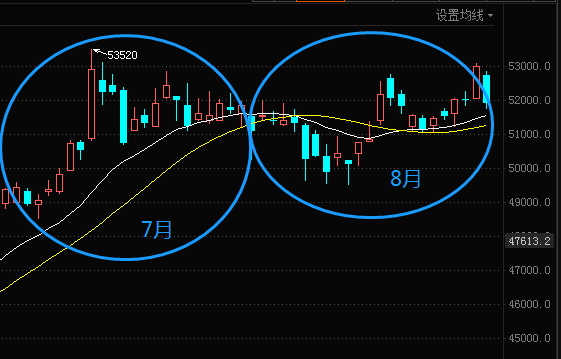

SMM9 March 2 News: Shanghai Copper main contract since July hit a high of 53520 yuan / ton, then gradually cooled down, continued high shock for many days. In mid-August, the center of gravity moved down and then rose slowly, but never broke the high set in July. The recent weak position of the US dollar has contributed to copper prices. The news of the sudden earthquake in Chile in the afternoon of September 1 sent copper prices higher in the short term to the 53000 mark, with Shanghai copper rising 1.92 per cent during the day.

SMM combined with the latest market in the upper and lower reaches of the industrial chain, consumption in the lower reaches has not yet come out of the off-season market, the domestic and foreign trade markets are both weak, domestic social inventory is still rising, and there is no significant disturbance information on the supply side, but the optimistic tone of continuous recovery in overseas markets, LME continues to go to the warehouse, bringing strong support, and copper price shocks are strong in September.

Supply end

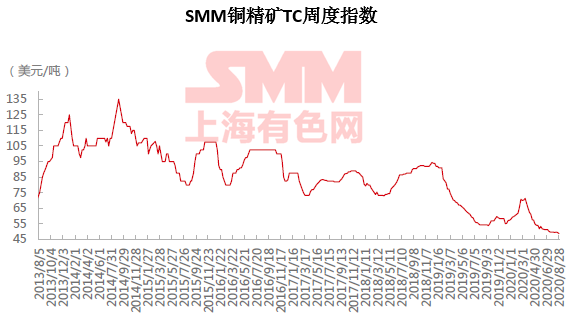

Recently, the biggest disturbance on the supply side has been the protest by workers at Grasberg Copper and Gold Mine in Freeport, Indonesia, but according to foreign media reports, the dispute was resolved on Friday and production at the mine was not affected by the strike. As of Friday, the SMM copper concentrate index (weekly) was at $48.85 / tonne, down 80 cents / tonne from the previous month. According to the latest news, mining activities in Peru have basically resumed, and spot TC may rise slightly, but in the case of tight overall supply, the room for improvement is very limited.

"for more data, please see SMM Copper Industry chain Database.

In terms of copper concentrate import, from the impact of the overseas epidemic situation, the copper supply gradually returned to normal in mid-late May. Combined with the transportation cycle, it has been reflected in the domestic copper concentrate import volume in July, considering that there will be a certain amount of compensation after the shipment resumes. Domestic copper concentrate import volume is expected to be high in September.

In terms of scrap copper, on the eve of the landing of the new solid waste law in September, SMM conducted market research that due to severe penalty provisions, coupled with the lack of news of the implementation date of recycled copper standards, greatly suppressed the trade enthusiasm of imported scrap copper, and domestic waste enterprises fell into a wait-and-see state for the procurement of scrap copper to Hong Kong after September, waiting for customs implementation or relevant departments to issue relevant explanation plans, and the quotation of import sources was low. From this point of view, imported scrap copper should shrink to a large extent in the short term.

Demand side

In September, domestic copper consumption remained in the doldrums, and the "Golden Nine and Silver Ten" did not arrive as scheduled.

According to a survey conducted by SMM, the operating rate of wire and cable enterprises in August was 97.02%, a decrease of 4.60% from the previous month and an increase of 5.86% over the same period last year. Among them, the operating rate of large enterprises is 106.98%, that of medium-sized enterprises is 52.32%, and that of small enterprises is 66.79%. Cable construction decreased significantly in August compared with the previous month. August is the off-season for traditional consumption of copper, especially in the downstream power industry. Due to the influence of high temperature, rainstorm and other weather, engineering orders such as rail transit high-speed rail decreased significantly. In addition, the copper delivery index of the cable factory from the national network in August was lower than that of the previous period, and some cable factories reflected that the earlier delivery plan from the national network was also delayed, and the decrease in the national network and outdoor construction orders was the main reason for the lower cable operation rate in August.

The SMM copper downstream PMI composite index continued to weaken in August, falling 0.95 to 50.06 from the previous month, at the edge of the contraction range. From a sub-industry point of view, except for the construction and transportation industries, the PMI of other industries is below the expansion area, but the PMI of all industries is lower than that in July. Among them, due to abundant funds and accelerated construction and other factors, the prosperity of the construction industry is relatively high. In August, PMI only dropped by 0.06 to 52.06 compared with the previous month, making it the best among many downstream industries. As the home appliance industry is in a "summer break" state, PMI fell 2.27 to 49.36 in August, making it the weakest industry.

August is the time for air conditioners and upstream and downstream enterprises to arrange maintenance in the off-season. As the major air-conditioning manufacturers end their holidays, the home appliance industry is expected to recover slowly. SMM expects the downstream industry PMI composite index to be 50.87 in September, up 0.81 percent from the previous month. Downstream industries will emerge from the off-season in September, but the pace of recovery will vary. The pace of recovery in the construction industry will be the fastest, and it is estimated that the power industry will not recover significantly until mid-late September, while the recovery pace of other industries such as electronics, transportation and household appliances will be the slowest and the growth rate will be limited; especially in the electronics industry, with the formal implementation of the US ban on ZTE Huawei on September 15, it is expected that this will have a greater impact on China's semiconductor industry.

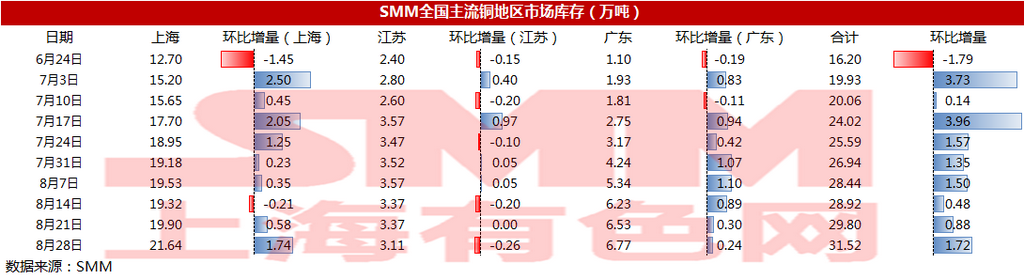

The continued accumulation of domestic inventories also indicates the recent weak state of refined copper consumption. Social inventories have been rising continuously for more than two months. as of the week of August 28, the market inventory of copper in the mainstream areas of SMM totaled 315200 tons, an increase of 153200 tons over the week of June 24, almost doubling.

"View the SMM copper industry chain database

Outlook for the future

On the macro level, the long-term tone of economic recovery remains unchanged. The domestic economy maintained a steady pace of recovery, with the official manufacturing PMI recording 51 in August, slightly down 0.1 percentage points from the previous month, indicating that the manufacturing sector as a whole is running smoothly. The US economic data performed better than expected, and the pace of economic repair did not weaken significantly. Prior to the Fed's transmission of expectations of continued easing, it is difficult to change the weak position of the dollar in the short term, all of which will support the strong pattern of copper prices.

Fundamentally, copper production in most overseas mining companies declined in the first half of the year compared with the same period last year, while copper production in Chile, a big copper producer, declined in July compared with the previous month, and the tight supply and demand pattern remains unchanged this year. September is the traditional peak season, and the improvement of the copper downstream industry is expected to lead to an increase in copper demand.

Guangzhou Futures analyst Licensing Yuan believes that from the perspective of supply and demand, the supply side of copper mine will remain tight in the short and medium term, and spot TC has been maintained in the range of 49-50 US dollars / ton for more than a month. On the demand side, the domestic off-season factors are still there. Last week, domestic explicit inventories fell back, and expectations for the peak season need to be further confirmed; while overseas demand continues to repair, LME European inventories have dropped significantly, returning to the level of early March, and global inventories as a whole are still declining. at present, LME inventories have been at a decade-long low, forming a more obvious support for outer disk prices. It is expected that the short-term external strong and internal weak pattern may continue, and the overall price will probably return to the upstream channel during September.

SMM expects Lun Copper to operate at US $6600-6850 per ton in September and Shanghai Copper at RMB 51600-53200 per ton.

"Click to sign up: 2020 Fifth China Electrotechnical Materials supply and demand Trade Summit

Scan the code to participate in the meeting or apply to join the SMM Electrical Industry Exchange Group