SMM7 March 31:

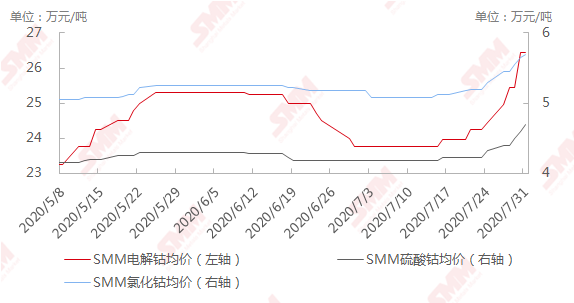

The price of cobalt in the domestic market has risen sharply. Since mid-July, the prices of electrolytic cobalt, cobalt sulfate and cobalt chloride have all increased by nearly 10% Murray 11%, which is higher than that in May-June, and the price increase of electrolytic cobalt, cobalt sulfate and cobalt chloride in May-June is only about 3-4%.

Price change of SMM Cobalt products from May 8 to July 31, 2020

Source: SMM

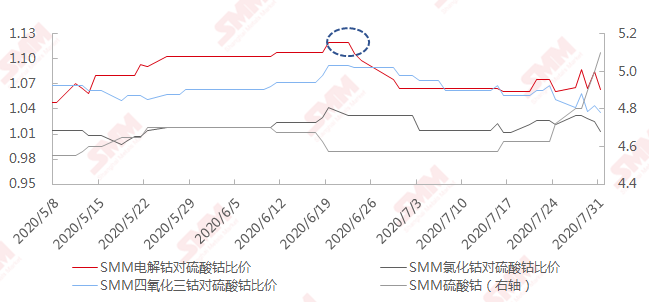

After the middle of June, the specific price of electrolytic cobalt to cobalt sulfate gradually tended to 1, mainly due to the gradual warming of battery material demand.

Price comparison of SMM Cobalt products from May 8 to July 31, 2020

Source: SMM

The supporting price increase in May-June this year is only due to the closure of ports in South Africa in April and the shortage of domestic cobalt raw materials in May-June. However, the fundamentals of smelting products in the domestic market still exceed demand, cobalt sulfate began to appear in the month of inventory, fundamentals improved. Downstream demand did not improve significantly, superimposed 3C digital electronic demand into the procurement off-season, the price increase is small.

The factors supporting price increases have increased since mid-July this year:

1. Cobalt raw material supply end:

The epidemic situation of novel coronavirus in Africa is serious, and confirmed cases have emerged one after another in the mining area, which has not affected production for the time being. although the prevention and control of the epidemic in the mining area is strict and the probability of large-scale spread is small, the market is still worried.

At present, the greater impact is the port capacity of South Africa. South Africa is currently the country with the worst epidemic in Africa, with more than 480000 confirmed cases and an increase of 10,000 new cases per day. It is understood that since the lifting of the ban in South Africa on May 1, the port capacity has been slow to recover, and the earliest shipping date will be issued in mid-May; from June to July, the port capacity is basically only 5-60% of the normal capacity; according to the feedback of cobalt raw material suppliers, because of its special transport channels, the shipping schedule is the same as that of the previous period, but there is no sign of improvement, and it is expected that the situation will continue in at least 2-3 months in the future. The shipping schedule of a few suppliers has deteriorated again in recent August, with other goods and cobalt raw materials seizing the limited capacity of South African ports.

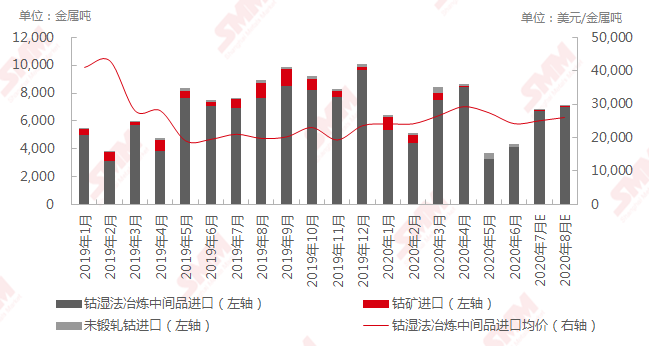

Imports of cobalt raw materials totaled 16800 tons of metal tons in the second quarter of 2020, down 19% from the same period last year. Of this total, cobalt ore imports totaled 100 tons of metal tons, down 92 percent from the same period last year; imports of cobalt wet smelting intermediates totaled 15800 tons, down 15 percent from the same period last year; and unwrought cobalt imports totaled 800 tons of metal tons, an increase of 57 percent over the same period last year.

China's import of cobalt raw materials from January 2019 to August 2020

Source: SMM, China Customs

African governments and industries have rectified the mining of their rivals, and there is news in the market that the full control of manual mining since August this year may affect the import of some cobalt raw materials in the short term, leading to a tightening of supply. However, the annual supply of hand-held ore, according to incomplete statistics, accounts for about 6% of the total global supply of cobalt raw materials, accounting for 10% of the total supply of cobalt raw materials, with little impact.

Therefore, the domestic cobalt raw materials continue to be tight, and will last at least 2-3 months in the future. According to the survey, considering the sea, domestic bonded areas, traders, smelters, battery plants, etc., the domestic cobalt raw material inventory is about 0. 9-11000 tons of metal tons, about 1-1. 5 months domestic cobalt raw material consumption, normal cobalt raw materials to maintain 2-3 months inventory.

The epidemic also increases the hidden costs of mining enterprises, making cobalt raw material suppliers hesitant to sell, with few loose orders and rising prices.

2. Smelting products supply side:

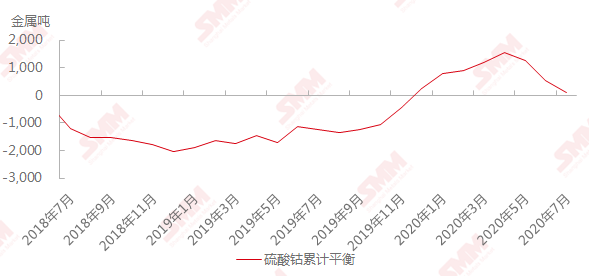

Take cobalt sulfate as an example, China's cobalt sulfate has basically reached the balance of supply and demand in July, and the market inventory of cobalt sulfate is low, supporting the upward quotation of cobalt sulfate suppliers.

From July 2018 to July 2020 E cumulative balance of cobalt sulfate in China

Source: SMM

3. Terminal demand side

3C digital terminal entered the peak of purchasing and stock preparation in the second half of the year. For upstream cobalt salt plants and cobalt tetroxide manufacturers, demand continues to improve. However, it is understood that the inventory of cobalt raw materials in the hands of major battery factories downstream is at least 1500-2000 metal tons, and there are still cobalt raw materials entering Hong Kong one after another every month. Lithium cobalt oxide manufacturers and battery factories have raw material inventory situation, which is more optimistic than the upstream cobalt salt and cobalt tetroxide. of course, there is also a little worry about the subsequent arrival of cobalt raw materials to Hong Kong.

The three-yuan demand began to pick up and is expected to improve in the second half of the year. Considering that the power battery factory is basically a long order for the purchase of ternary materials, at present, the inventory of battery factory and Sanyuan material factory is still in stock, and the demand for upstream raw material procurement has not increased significantly. Downstream orders only gradually recover, the demand growth rate is lower than the upstream raw material price increase, so the price is still difficult to transmit.

4. macro capital inflow, collection and storage catalysis.

Recently, the domestic macro aspect continues to improve, with more capital inflows, which leads to a substantial increase in the market demand for electrolytic cobalt, but there is no sign of improvement in the actual end-consumption demand of superalloys, magnetic materials, chemical industry and other industries. In addition, there are rumors in the market that the collection and storage of electrolytic cobalt has also catalyzed the rise in cobalt prices this round, but the news of collection and storage has not landed for the time being and is expected to have little impact on the market.

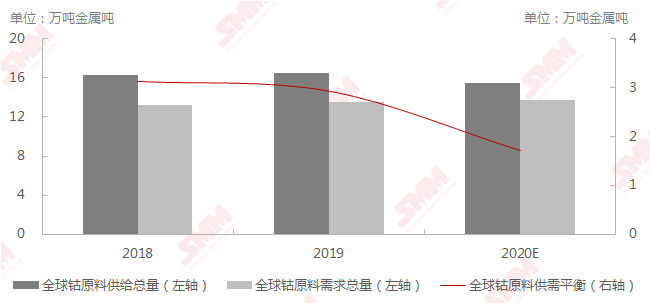

To sum up, affected by the novel coronavirus epidemic in 2020, supply and demand are both weak, the global cobalt supply exceeds demand fundamentals will remain unchanged, but the supply and demand situation may improve significantly, it is expected that the global cobalt raw material supply and demand balance 17000 tons of metal tons.

On the supply side, the Glencore Mutanda copper and cobalt mine has been shut down, some of the new cobalt raw material projects originally scheduled to start production this year may be postponed to next year, and the supply of grasping ore will also be reduced in the short term, so SMM continues to cut its forecast for cobalt raw material supply this year to 155000 tons of metal tons, down 6 per cent from the same period last year. On the demand side, SMM lowered its production forecasts for new energy vehicles, digital and energy storage, and the total global cobalt demand was reduced to 138000 tons of metal tons.

Global Cobalt supply and demand balance in 2018-2020

Source: SMM

Although the demand for 5G, online office, and wearable electronic products has increased, the demand for lithium cobalt and upstream raw materials has increased, but the production and sales of mobile phone terminals with the highest market share affected by the epidemic are expected to continue to shrink, diluting some of the increase in demand for lithium cobalt and upstream cobalt raw materials. Therefore, it does not rule out the possibility that the price increase of upstream raw materials is too large, which may lead to the delay of downstream stock plan batches. Therefore, from the perspective of cobalt supply and demand, the increase of cobalt price in the second half of the year is limited, and the price of electrolytic cobalt may fluctuate between 23 and 320000 yuan / ton.

SMM Cobalt Lithium New Energy Research team:

Qin Jingjing 021-51666828

Mei Wangqin 021-51666759

Huo Yuan 021-51666898