SMM7 March 16: today, at the 2020 China (Yingtan) Copper Industry Summit Forum and the 15th China International Copper Industry chain Summit hosted by SMM, Hu Jian, vice president of SMM, delivered a speech on the theme of "Global Copper concentrate Market in the Post-epidemic era". It is mainly carried out from three aspects: the supply and trend of global copper concentrate market, the cost and evolution of global copper concentrate, and China's overseas copper investment.

Supply and trend of global copper concentrate

Global output and distribution of copper concentrate

The world's copper reserves are 870 million tons, mainly distributed in Chile, Australia, Peru, Russia, Mexico and the United States. Its copper reserves account for about 62 per cent of the world's total reserves, while China's copper resources are scarce, accounting for only 3 per cent of the world's reserves.

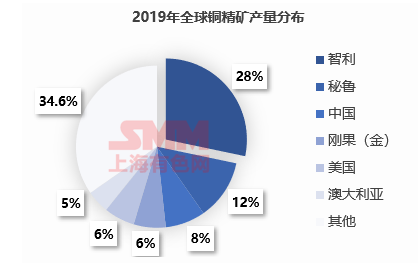

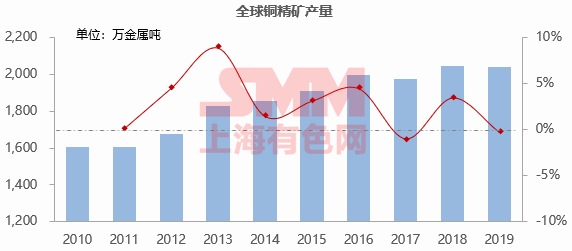

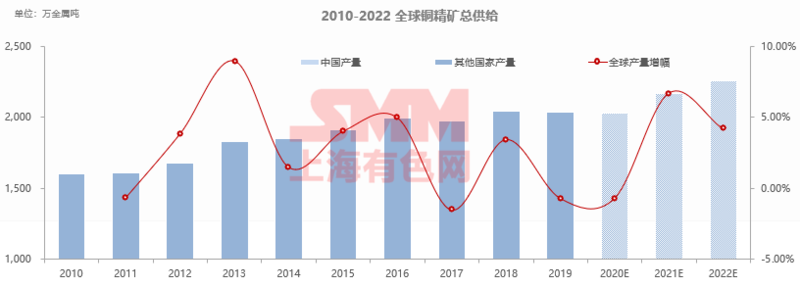

In 2019, global copper concentrate production was 20.37 million tons, mainly concentrated in Central and South America (42 per cent), Asia (18 per cent), North America (13 per cent), Africa (11 per cent), Europe (8 per cent) and Oceania (5 per cent). Chile is the world's largest copper producer, with an output of 5.83 million metal tons in 2019, accounting for 28.3 per cent of global copper production, followed by Peru, China, the Democratic Republic of the Congo, the United States and Australia.

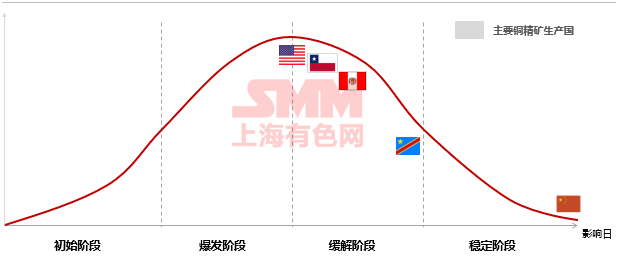

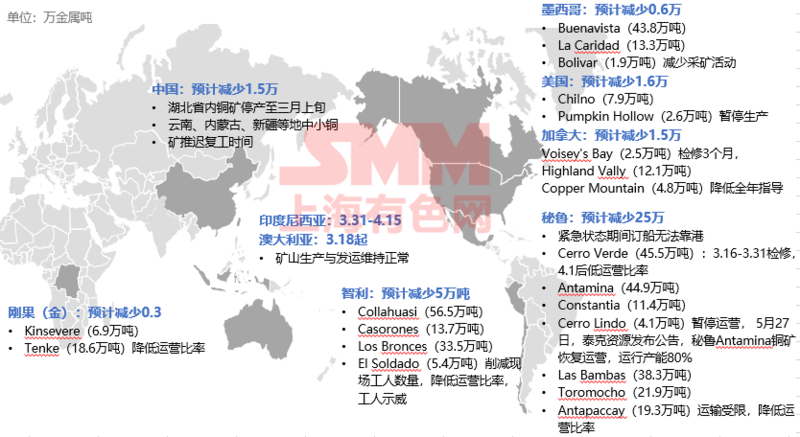

The world's major copper concentrate producing countries are still deeply affected by the new crown epidemic.

Global copper production under the influence of epidemic situation

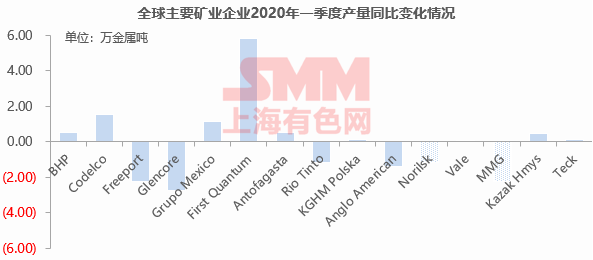

Copper production by the world's major mining companies fell 0.6 per cent in the first quarter of 2020 compared with the same period last year, with limited recovery in the later period.

So far, mining companies such as Freeport, Rio Tinto, Antofagasta and Vale have all cut their full-year production forecasts.

According to estimates, the output of overseas copper mines affected by the epidemic reached 333500 tons, and the output affected for the whole year is expected to be about 450000.

Growth is expected to fall to-0.3 per cent in 2020, compared with a global increase of about 400000 tons in 2020.

Output and distribution of copper concentrate in China

Between 2020 and 2021, the world is expected to add 1.39 million metal tons of copper concentrate capacity, mainly in Indonesia and China, accounting for 45 per cent of the total.

The overseas epidemic continues to spread, economic operation is blocked, the process of projects under construction slows, and in response to the decline in income, some mining companies began to cut capital expenditure, affecting the supply of medium-and long-term copper mines.

According to the China Mineral Resources report 2019, the national copper reserves are 114.43 million tons, and the company's copper resources reserves are about 57.25 million tons in 2019, mainly distributed in Yunnan, Inner Mongolia, Jiangxi, Tibet and other regions.

There are more small and medium-sized copper deposits in China, and there are few large and super-large copper mines; the average grade of domestic copper resources is about 0.8%, and the proportion of copper reserves with a grade of more than 1% is not high; the mining conditions are relatively complex.

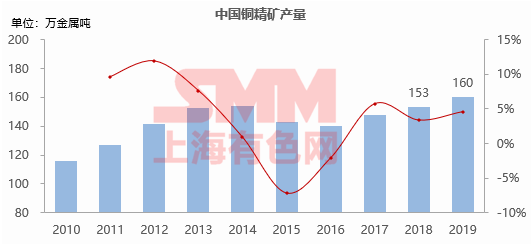

In 2019, China produced 1.6 million tons of copper concentrate, mainly in Jiangxi (21%), Yunnan (14%), Anhui (11%), Gansu (10%), Xinjiang (8%) and Inner Mongolia (7%).

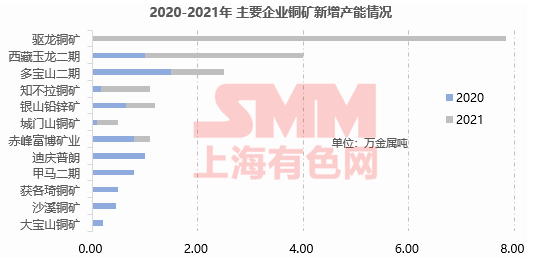

New expansion of Copper Mine in China in 2020-2021

The new output of future copper projects will mainly be in Tibet, Heilongjiang and Yunnan, of which Tibet accounts for 68% of the increase.

Compared with overseas copper mines, the domestic copper mine supply is not much affected by the epidemic, and the domestic copper mine output is expected to increase by about 70,000 tons in 2020. In 2020, the main project of domestic contribution increment is the second phase expansion project of Duobaoshan Copper Mine in Heilongjiang, with an estimated increment of 15000 tons. With Zijin Mining's acquisition of Julong Copper, the commissioning of the project is expected to accelerate, and the first phase of the project is expected to be completed and put into production by the end of 2021, which may contribute to an important increase in domestic copper supply in the future.

With the mitigation of the epidemic and the commissioning of new expansion projects, global copper concentrate production is expected to resume growth in the future, an increase of 470%.

Cost and evolution of global copper concentrate

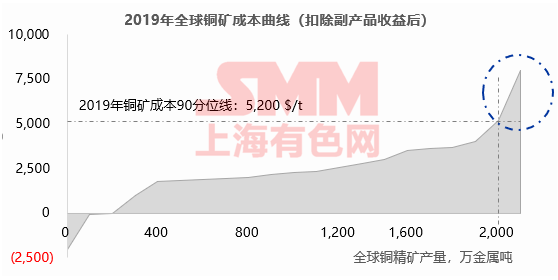

In 2019, the 90-percentile line of the world's copper mines is around 5200 US dollars per tonne, and the center of gravity is expected to shift downward in 2020 due to the fall in oil prices.

In the cost distribution, Chinese mines above the 90 quartile account for more than 50%, mainly some small and medium-sized mines.

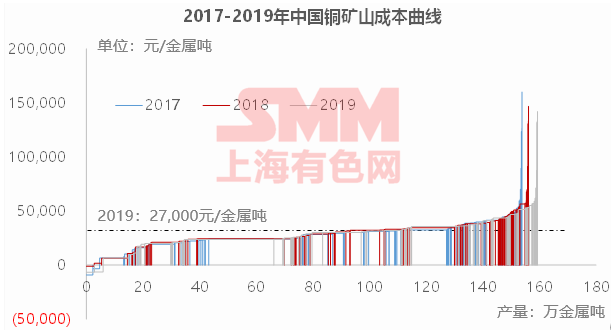

In 2019, the weighted average cost of China's copper mines after deducting by-product income was 27000 yuan per metal ton, an increase of about 1200 yuan per ton compared with 2017.

The costs of enterprises in different regions and different sizes are different. The production costs of copper mines in Jilin and Xinjiang are relatively low, while those in Anhui and Yungui are relatively high.

The production cost of copper concentrate in China is on the rise for the following reasons: 1. The mine grade decreases year by year, and the mining depth increases 2. Labor costs have increased by 3. Affected by environmental factors, the cost of pollutant treatment and investment in environmental protection equipment increased.

Global copper mine costs will continue to rise

Inflation: although energy and other prices affected by the epidemic fell sharply in 2020, the cost will continue to rise as energy and manpower enter a new inflation cycle in the future.

Raw ore quality: the global high-quality copper resources have been basically carved up, and the taste of mining raw ore continues to decline year by year.

Environmental protection and safety: green mine construction, tailings reservoir upgrading, underground mine safety.

Overseas Investment of Chinese Copper concentrate

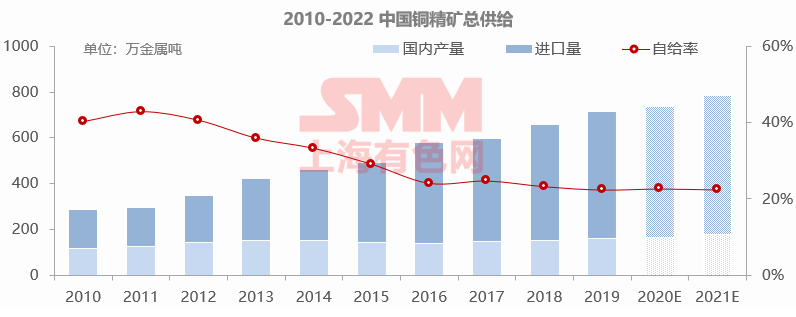

Self-sufficiency in Chinese copper concentrates fell from 40 per cent in 2010 to 22 per cent in 2019.

With the continuous expansion of China's smelting capacity, the demand for copper materials continues to grow, and limited by the lack of domestic copper resources, China's copper concentrate is highly dependent on imported resources. With the commissioning of a number of new domestic copper mine expansion projects, it is expected that the annual supply capacity of domestic copper concentrate will increase by 14% from 2020 to 2022, but the increment is still limited. Imported copper concentrate will still be the main supply of copper concentrate in China.

The investment route of Chinese enterprises in foreign copper mines

Although the proven reserves of the DRC copper deposit account for a relatively low proportion in the world, the copper ore grade is high and the degree of development is low, so it has the potential to increase reserves and production, so it has attracted a large number of Chinese enterprises.

At the same time, Africa is an important partner of the Belt and Road project.

China Metallurgical, Chinalco, Minmetals, Luomo Molybdenum, Zijin, Tongling Nonferrous, Jinchuan and China Nonferrous are the main forces in overseas copper acquisitions, accounting for about 80% of China's overseas equity copper reserves.

The development of Chinese enterprises' projects in Africa is mainly affected by infrastructure, environmental protection, electricity, taxation, geopolitics and other factors.

The Las Bambas copper mine in Peru, jointly funded by Minmetals Group, Guoxin International and CITIC Metals, is the largest copper project built by Chinese enterprises abroad, with an annual output of about 400000 tons of copper concentrate.

The projects of MCC and Jiang Copper in Afghanistan are moving slowly, which is affected by the local political environment, cultural relics transfer, environmental protection and other problems, causing frequent stagnation of the project.

The project of Jiang Copper and Minmetals in Peru was originally scheduled to be completed and put into production in 2012, but it has not yet been put into production due to environmental assessment and land purchase and other reasons.

In addition to the listed independent construction or operation projects, Chinese enterprises often participate in overseas mining projects through financial investment or leasing operation.

Scan the code to apply for admission to the SMM Copper Industry Exchange Group:

![[SMM Analysis] The "Counter-Cyclical" Logic of Copper Smelting: When Sulfuric Acid Becomes the Main Product](https://imgqn.smm.cn/production/admin/news/cn/thumb/cWPFD20180621153942.png?imageView2/1/w/176/h/110/q/100)

![BC Copper 2604 Closed Lower with a Wide Trading Range, Pressured by Both Geopolitics and Interest Rate Cut Expectations [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)