SMM7 March 12 News: most of the non-ferrous metals market rose this week, Shanghai Nickel and Shanghai Tin fell back and spit some gains on Friday. From a macro point of view, A-shares have performed well recently, superimposed in June, international commodity prices have picked up, domestic manufacturing industries have recovered steadily, and market demand continues to improve. According to statistics bureau data, PPI rose 0.4% month-on-month in June, the decline narrowed, the macro mood improved, and the overall trend of non-ferrous metals was strong.

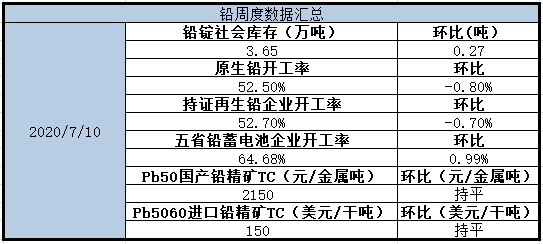

In terms of lead, in terms of fundamentals, in terms of primary lead, in July, Henan Yuguang gold and lead was in a state of replacement production line, and its output was further tightened; while some smelters, such as Chihong in Yunnan and Shuikoushan in Hunan, were overhauled, and the production of primary lead was expected to decline in July. In terms of recycled lead, the profits of recycled lead enterprises have been repaired, the production enthusiasm of smelters is high, and the demand for waste batteries is rising, which makes the supply of waste batteries still tight and it is difficult to increase production. Overall, the supply side is tightening. At the consumer end, the inventory pressure of lead-acid battery products is transferred to dealers. At present, dealers still mainly digest inventory, lack of support for lead consumption, and the lower reaches mostly favor the deep water supply of recycled lead, so the demand for primary lead is limited. SMM believes that the primary lead supply side is slightly tight, downstream consumption is basically in the state of digesting inventory, but affected by capital disturbance, and warehouse receipt inventory is seriously insufficient, the overall trend of Shanghai lead is strong in the short term.

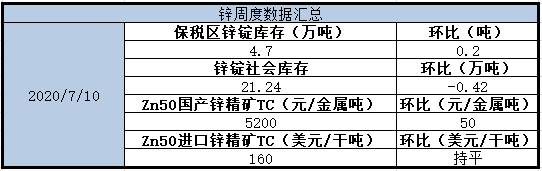

In terms of zinc, from the fundamental point of view, the supply side, the domestic side, in July, the raw material inventory level of domestic smelters returned to normal. At present, the average raw material inventory days is about 28 days, and the problem of raw material shortage in smelters has been basically solved. Mainly to resume work and return to production. The overhaul of the smelter in July is less, and the domestic refined zinc output is expected to increase by 26400 tons to 491800 tons in July compared with the previous month. At present, the consumption of zinc downstream is in the off-season, and there is no bright performance on the consumer side. As for galvanizing, due to the recent rainy season affecting the start of some projects, galvanized pipe terminal orders are lower than before. In terms of structural components, due to the recovery of the epidemic, the iron tower project is basically based on the rush order of last year's project, and many bidding projects have not yet started this year, resulting in a gap in the middle. At present, the tower order is weak. Due to the influence of overseas epidemic situation, external demand orders for die-casting zinc alloy and zinc oxide plates have not improved. Generally speaking, the trend of zinc price depends on the choice of funds. boosted by macro optimism, hot money continues to pour into the market, vigilant against the situation in China and the United States and tightening domestic monetary policy in the future, but the fundamentals are mainly wait-and-see.

Copper:

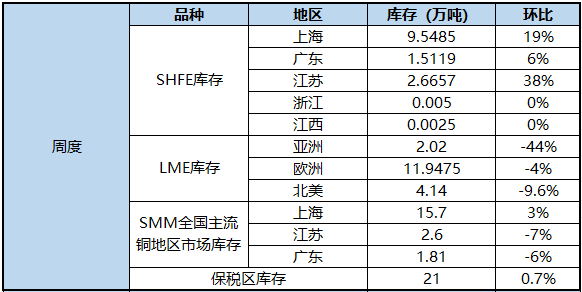

The social inventory of electrolytic copper in the three places of SMM increased by 1400 tons month-on-month this week, which was significantly lower than that of last week, mainly due to the gradual digestion of wet-process copper concentrated in Hong Kong last week, and the pressure on the arrival of imported copper was alleviated this week. It also reflects that domestic consumption still performs well, and it is difficult to return to the discount level in this case, but the continuous expansion of refined waste price gap also has a certain impact on refined copper rod consumption. LME inventories continue to decline this week, giving marginal support to copper prices. The strengthening of overseas structure has led to the weakening of the specific price of electrolytic copper imports, the impact of import premium continues to decline, and the inventory in the bonded area has also increased slightly. Under the optimistic background of the capital market, the interference on the copper mine side intensifies, and the copper price still has the long-term upward momentum. Lun Copper is expected to operate at US $6300 per ton, while Shanghai Copper will run at RMB 52000 per ton.

Aluminum:

Inventory of aluminum rods has increased in East China this week, down 900 tons from last Thursday to 72300 tons. Inventory in Wuxi, Changzhou and Nanchang declined, while inventory in Foshan and Huzhou increased, with a large increase in inventory in Foshan. Inventory in Guangdong and Henan Province-East China continues to go to the warehouse, SMM statistics domestic electrolytic aluminum social inventory fell 4000 tons compared with last Thursday to 715000 tons.

Lead:

The bullish logic of the domestic market, first, the peak season of traditional consumption; second, the macro environment is still good. From the point of view of the market's current willingness to deliver positions, inventory situation, spot rising performance, and scrap price difference, the fundamentals of lead are not obvious, but from the willingness of bulls to receive goods in recent months, there is no willingness to leave before delivery, and it is expected that the contract may continue to do Borrow in August. The lead futures contract is expected to run at 14950Mui 15350 yuan / ton.

Zinc:

In terms of Shanghai zinc, the domestic stock market rose brightly this week, driving a pick-up in macro sentiment in the market, hot money promoted a strong rebound in non-ferrous metals, and zinc prices basically deviated from the fundamentals in the second half of the week. But on Friday, it was reported that the United States will resume imposing 25% tariffs on some Chinese goods, and Sino-US trade relations still sow a lot of uncertainty to the macro mood. From the perspective of next week, the fundamentals of zinc in Shanghai are still weak. On the supply side, smelters such as Tongguan in Anhui, Sanli in Hunan and Taifeng in Hunan have been overhauled and normal production has resumed. Superimposed zinc prices have returned to high levels in the first half of the year, and smelters are willing to ship goods. The overall pressure on the supply side is on the high side. On the consumer side, under the high zinc price, most downstream enterprises mainly consume inventory, hold a wait-and-see attitude to the price, and their willingness to buy is very weak under the influence of the off-season of domestic consumption. orders are also slightly weaker than the previous month, the overall market demand is poor, and there is still no support from a fundamental point of view. From a technical point of view, Shanghai zinc jumped on the Brin Road, it is expected that there will be some bullish exit next week, zinc prices may have a certain pullback, but the support of the Qiqi pass is still strong. Next week, we still need to pay attention to the impact of Sino-US relations and the epidemic in Kazakhstan on macro-sentiment. Overall, next week, Lun Zinc is expected to run at US $2,180 per ton at 2120Mel; 2008 of the main contract for Shanghai Zinc is expected to run at RMB17,250,17,850 per ton, and the spot side is expected to raise water at around RMB40 per ton in August.

Nickel:

The main 2010 contract of Shanghai Nickel opened at 106030 yuan / ton at the beginning of the week. after the opening of trading at the beginning of the week, the bulls actively entered the market to try more, and then funds continued to pour into the nickel market, and the long position greatly increased to push the Shanghai Nickel Station above 107000 yuan / ton. In the middle of the week, the center of gravity of Shanghai nickel revolves around 107300 yuan / ton first-line shock consolidation, during which several times it rushes up to 108000 yuan / ton and then falls back under pressure. On Thursday night, due to the sharp fall in the price of US crude oil, the heightened risk aversion sentiment of funds near the weekend made Shanghai nickel give up its weekly rise, falling to the 10-day moving average of 105200 yuan / ton to be supported. In the end, Shanghai Nickel closed at 105450 yuan / ton, down 390 yuan / ton, or 0.37%. Although Shanghai nickel has fallen back, there are still many positions in the main force, and under the policy of sustained easing of funds, if Shanghai nickel can be consolidated at the 105000 yuan / ton line next week, it is still expected to break through again. This week, the average weekly price of SMM1 nickel is 106000 yuan / ton, Jinchuan nickel is 106500 yuan / ton, and Russian nickel is 105490 yuan / ton. As nickel prices continued to fluctuate at high levels this week, nickel prices did not fall back until Friday, so the spot trading atmosphere was light, and traders made deals only on Friday. In terms of the discount, the spot still quoted a price for the Shanghai Nickel 2008 contract. Due to the high turnover of the stock, the Russian Nickel discount remained stable within the week, and most traders quoted prices between RMB400 and RMB5000.The rising water of Jinchuan Nickel showed a gradual downward trend during the week. from the beginning of the week, the rising water gradually fell back to 300 yuan / ton, on the one hand, due to the sufficient supply of goods in the market, and consumption continued to be weak; On the other hand, Jinchuan company actively shipments, trade nickel prices are strong, in the high hedging, so Jinchuan nickel rising water gradually lower. Nickel beans, the discount range remained stable at-1500 yuan / ton, steel mills every bargain during the week, inventory has been reduced. As delivery is approaching next week, and as the supply of low-priced goods in the market decreases, the spot discount may be firm, traders will consider a monthly offer after delivery.

Tin:

This week's Shanghai tin 2009 contract, guided by the stock market and macro sentiment at the beginning of the week, rose sharply after opening, hitting a year-to-date high of 142800 yuan / ton before peaking a pullback. In the middle of the week, it was mainly affected by bulls leaving the market, and tin in Shanghai showed a downward trend of concussion. It opened high and left low on Friday night, and the decline continued unabated after opening in the morning. during the last trading period, the lowest point in the week was 138610 yuan / ton, closing at 138900 yuan / ton. During the week, it fell 890 yuan / ton, or 0.64%, to 167000 hands and 29567 positions, an increase of 406 hands. The weekly line level is a small Yin line, and the physical part is above all moving averages. In terms of indicators, the weekly-level MACD opening is upward, the K-line has the intention to impact on the upper rail of the Bollinger belt, but there is pressure above, and the daily-level MACD index forms a dead fork, and the K-line breaks through the upper rail of the Bollinger belt at the beginning of the week and then goes down under pressure. The bulls on the disk have obvious departure and profit-taking trend, but they have not yet fallen below the previous platform line, and there is still a 20-day moving average at the bottom of the platform line. Next week, we need to continue to pay attention to whether the main bulls return to the market, the lower support level is expected to be located near 137500 yuan / ton in the middle rail of the day-level Bollinger belt, and the upper pressure level is around 143000 yuan / ton. This week, the Shanghai-tin spot market generally follows the Shanghai tin market, showing a trend of rising first and then suppressing it. Affected by the good news of the stock market at the beginning of the week, tin in Shanghai rose sharply at the beginning of the week, and the spot price rose by about 1000 yuan / ton. the price of tin was high, and the downstream just needed to collect goods. Traders held a wait-and-see attitude, and the overall spot market of Shanghai and tin was afraid of heights and wait-and-see. The futures market rose sharply, the spot price rose less than the spot price, and the rising water decreased greatly compared with last Friday. Yunxi rose 1500 yuan / ton to around 500 yuan / ton, Yunzi rose 1000 yuan / ton to near flat water, and the ordinary small brand dropped from flat water to 1000 yuan / ton. Subsequently, the futures market fell somewhat, showing a concussive downward trend, and the spot price also fell. On Friday, the Shanghai tin futures opened high and opened low from the night market, hit the lowest point of the week below, and the spot price also fell. On Friday, the average spot price of Shanghai tin was about 140000 yuan / ton. In terms of discount, Yunxi and Yunzi of Shanghai tin 2008 contract fell by about 1000 yuan / ton compared with last week, while the small brand dropped from near flat water to 1000 yuan / ton.

"Click to participate in the second China (Yingtan) Copper Industry Summit Forum and the 15th China International Copper Industry chain Summit"

Scan the code to sign up for the summit or apply to join the SMM industry exchange group:

![[SMM Analysis] The "Counter-Cyclical" Logic of Copper Smelting: When Sulfuric Acid Becomes the Main Product](https://imgqn.smm.cn/production/admin/news/cn/thumb/cWPFD20180621153942.png?imageView2/1/w/176/h/110/q/100)

![BC Copper 2604 Closed Lower with a Wide Trading Range, Pressured by Both Geopolitics and Interest Rate Cut Expectations [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)