SHANGHAI, Dec 4 (SMM) – Iron and steel capacity in China will gradually shift from the northern to the southern regions, amid the ongoing replacement initiative of the existing capacity.

While overall outdated capacity will be replaced by new capacity of smaller amounts, the capacity of electric arc furnaces (EAFs) will see net increases till 2023, as China promotes the use of more environmentally-friendly EAFs for steelmaking.

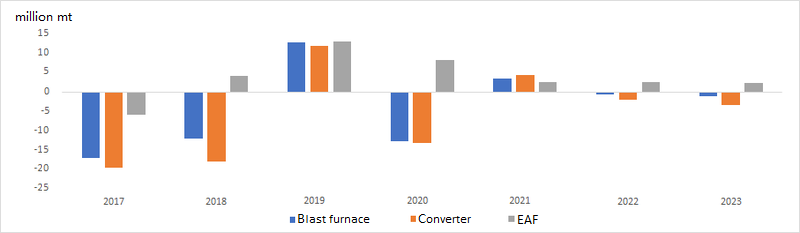

A net increase of 21.41 million mt/year is expected in domestic EAF capacity in 2019-2020, with this year accounting for 13.22 million mt/year and 2020 taking up 8.19 million mt/year, based on replacement approval announcements.

A net increase of blast furnace capacity is expected at of 12.78 million mt/year in 2019, with 12.01 million mt/year of converters and 13.22 million mt/year of EAFs, according to SMM calculations. This is calculated based on the estimated removal of outdated capacity of 29.91 million mt/year, 22.21 million mt/year, and 14.07 million mt/year for blast furnaces, converters, and EAFs respectively.

A net reduction of 12.83 million mt/year of blast furnace capacity and 13.16 million mt/year of converter capacity, but a net increase of 8.19 million mt/year of EAF capacity is expected in 2020, SMM assessed.

The swapped new capacity for blast furnaces, converters and EAFs due to be commissioned in 2020 has reached 101.11 million mt/year, 92.45 million mt/year, and 20.95 million mt/year, respectively. Among this, over 60% will come online in the second half of next year.

Net increase of facility capacity in 2017-2023

In China’s steelmaking hub Hebei province, capacity replacements over 2020-2023 will, in theory, result in a net loss of 31.77 million mt/year of pig-iron-producing capacity and 17.03 million mt/year of steelmaking capacity.

This follows after the completed elimination of 14.03 million mt/year of steelmaking capacity in the province this year.

Jiangsu province, another steelmaking centre in east China, will likely see a net gain of 3.65 million mt/year of pig iron capacity and 2.48 million mt/year of steelmaking capacity in 2020-2023.

During the same period, the southern China region is likely to see a net increase of pig iron capacity by 9.23 million mt/year and steelmaking capacity rising by 10.48 million mt/year, SMM calculations showed. The forecast is based on the total additions of 19.98 million mt/year of pig iron capacity and 26.2 million mt/year of steelmaking capacity through the replacement mechanism.

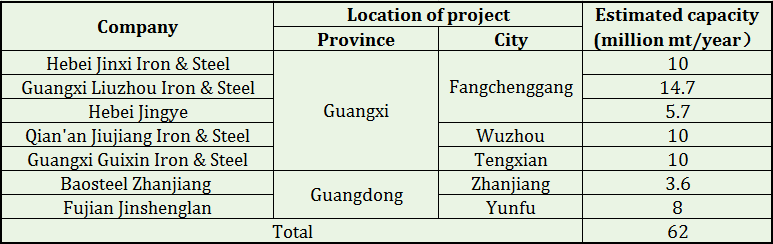

Guangxi province will likely emerge as a new steelmaking hub in south China as several new projects are in the pipeline, according to announcements.

SMM expects domestic production of steel products to continue increasing in 2020 on the back of higher capacity utilisation rates amid capacity replacement.

Rising supplies this year have kept spot prices of steel products lower from a year ago.

According to SMM survey, domestic average prices of spot rebar in the year to December 3 stood at 3,964 yuan/mt, down 204 yuan/mt year on year. During the same period, the average prices of hot-rolled coil in China fell 303.2 yuan/mt and came in at 3,804.3 yuan/mt as of December 3.