Summary of basic Metal production in China in May 2019

Electrolytic copper:

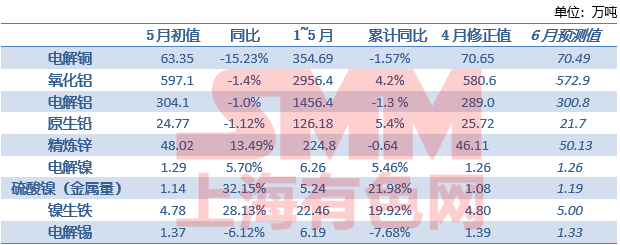

According to SMM data, China's electrolytic copper production in May 2019 was 633500 tons, down 10.33 percent from the previous month, down 15.23 percent from the same period last year, and the cumulative output from January to May was 3.5469 million tons, down 1.57 percent from the same period last year. The output in May was lower than expected, mainly due to the sudden failure of the Chifeng Jinfeng acid system and the local security inspection of Wuxin in Xinjiang, and the copper industry in eastern Shandong was damaged by the joint guarantee incident.

The increase in maintenance and the release of new expansion capacity are the main reasons for limiting production growth this year. According to SMM statistics, the output affected by maintenance from January to May is close to 192000 tons for the whole of last year. Up to now, the capacity utilization rate of Chinalco Ningde is less than 80%. The refeeding time of Guangxi Nanguo Copper Industry has been moved back to late June, and the Chifeng Jinfeng Phase I project will not be officially fed until around 18 May. The whole new expansion project has been put into production and the time to reach production has shifted backward. The reclaimed copper smelter in operation has also experienced a decline in capacity utilization because of the narrowing of the price difference between scrap copper and refined copper.

In June, the output of copper industry in eastern Shandong is still difficult to recover, Zhongyuan gold smelter, Qingyuanjiang copper, rich metallurgy group, purple gold copper and other smelters have maintenance arrangements; In addition, some smelters said that due to the shortage of scrap copper and copper concentrate, due consideration will be given to extending maintenance time and reducing production. According to production schedules, production will return to 704900 tons in June due to the end of centralized maintenance in May, still down 2.43 per cent from the same period last year, and 4.2518 million tons in the first half of 2019, a cumulative decrease of 1.72 per cent.

Alumina:

According to SMM data, in May (31 days), China's alumina (metallurgical grade) output was 5.971 million tons, down 1.4 percent from the same period last year, and its annual operating capacity was 70.304 million tons, down 336000 tons from the previous month and 991000 tons from the same period last year. The average daily output was 193000 tons, down 1000 tons from April, and China's alumina production from January to May 2019 was 29.564 million tons, an increase of 4.29 percent over the same period last year.

The average daily output and operating capacity continued to decline in May. In May, the overhaul of Huayin in Guangxi affected part of the output. Lingshi hopes that the technical transformation will stop production one line, and Xinfa in Guangxi will stop production in May. Jiaokou Xinfa and Xiaoyi Huaqing were ordered to stop production and rectify due to environmental protection problems. Xinghua science and technology operation capacity dropped to 350000 and gradually resumed production. At the same time, Guizhou Huafei, Lu Yu Bochuang and Bosai Shuijiang resumption projects continued to contribute new output. Shandong Weiqiao operating capacity in May compared with April slightly lifted, Chinalco Huaxing operating capacity is also gradually rising.

In June (30 days), the delivery of messages basically no longer produces alumina, but it is expected that recovery projects such as Lu and Yu Bochuang and Bosai Shuijiang will continue to contribute to the new output, and at the same time, the overhaul of Huayin in Guangxi is over, and Xinghua Science and Technology will gradually return to full production. The operating capacity of Chinalco Huaxing, Chinalco Mining Industry, Sanmenxia Hope, Guangxi Xinfa and other alumina plants have all recovered. SMM expects alumina production to be 5.729 million tons in June, down 4.0 percent from the same period last year, and an annualized operating capacity of 69.703 million tons. It was down 2.884 million tons from the same period last year and 601000 tons from the previous month.

Electrolytic aluminum:

According to SMM data, China's electrolytic aluminum production in May (31 days) was 3.041 million tons, down 1.0 percent from the same period last year, and the total domestic electrolytic aluminum production from January to May was 14.564 million tons, down 1.3 percent from the same period last year.

Although the domestic electrolytic aluminum operation capacity rebounded in May, the overall supply continued to maintain a negative growth. Based on the May output, the domestic electrolytic aluminum annualized operation capacity increased by 643000 tons to 35.805 million tons compared with April. There was a decrease of 377000 tons compared with the same period last year. Some new and reproducing aluminum plants in Gansu, Yunnan, Guangxi, Qinghai and other provinces have become the main motivation for the recovery of operating capacity. After June, the new and resumed electrolytic aluminum manufacturers mainly include Suyuan, Zhaotong, Meixin and Zhongrun and other aluminum plants. The total net production capacity is expected to increase by 210000 tons. SMM expects China to produce 3.008 million tons of electrolytic aluminum in June (30 days). Compared with the same period last year, the total domestic production of electrolytic aluminum is expected to be 17.573 million tons in the first half of 2019, down 1.2 per cent from the same period last year.

Primary lead:

In May 2019, China's primary lead production was 247700 tons, down 3.69 percent from the previous month and 1.12 percent from the same period last year. Primary lead production was 1.2618 million tons from January to May 2019, up 5.4 per cent from a year earlier.

According to the investigation of SMM, in May, the maintenance and recovery of primary lead smelting enterprises were in parallel, such as Yunnan Chihong and so on. At the same time, Hunan Jingui, Yinxing, Chifeng Mountain Gold, Silver and lead entered the maintenance in the middle and late May one after another, increasing less and decreasing more, so the output decreased by nearly 10,000 tons compared with April, basically in line with the expectations of the previous report.

In addition, due to the different months of the Spring Festival holiday, and the production restrictions caused by environmental protection or (blizzard) and other bad weather in the same period last year, the cumulative output growth in the early period (January-April 2019) was relatively high, so the cumulative increase continued from January to May compared with the same period last year.

Looking forward to June, according to SMM, the number of maintenance of primary lead smelting enterprises has increased, such as Hunan Jingui, Chifeng Mountain Gold, Silver and lead, Hechi South, etc. (the maintenance time runs through May and June), others such as Hanzhong Zinc Industry and Western Mining Industry, Shandong Hengbang and so on began to overhaul, because most of the overhauled smelting enterprises are medium and large enterprises, the output has a great impact; In addition, due to the downturn in the lead market and the decline in lead concentrate processing fees, some enterprises have also made seasonal adjustments to production. Taken together, SMM expects primary lead production to fall by about 30, 000 to 217000 tons in June.

Refined zinc:

In May 2019, SMM China produced 480200 tons of refined zinc, an increase of 4.14 percent over the previous month and an increase of 13.49 percent over the same period last year. The SMM survey sample has a production capacity of 6.085 million tons.

In May, under the stimulation of high profits and the gradual recovery of environmental protection and relocation of some large enterprises, the output of refineries increased significantly.

Although there are still new maintenance in western mining and Mengzi mining and metallurgy enterprises in May, the output of Chihong zinc germanium, silver nonferrous headquarters and other routine maintenance ended, and the output increased more. At the same time, the further recovery of the output of Zhuzhou smelting, Hanzhong zinc industry and other large plants also contributed to the increase. And there are still some refining enterprises due to the increase of concentrate into the furnace taste and part of the small capacity of refining enterprises under the joint action of high profit production recovery, the whole output increased significantly compared with the previous month.

In June, the new maintenance is mainly Anhui copper crown and Chengzhou mining and metallurgy, but the western mining, Huludao zinc industry maintenance ended, Zhuzhou smelting the second production line further put into production, contributing to the main increment. At the same time, some enterprises continue to increase production slightly under the stimulus of profits, and their output is expected to increase further in June from a month earlier, an increase of 21100 tons to 501300 tons from May, an increase of 16.56 percent over the same period last year, and an increase of 4.4 percent from the previous month. It is estimated that the cumulative refinery output from January to June will change from negative to positive, with a cumulative year-on-year rate of 2.1%.

Electrolytic nickel:

In May 2019, the national natural monthly output of electrolytic nickel was 12900 tons, an increase of 5.70 per cent over the same period last year. In May, the national electrolytic nickel production increased by 2.62% over April. The production of electrolytic nickel remained normal in May, and the slight increase in production was mainly due to the increase of natural days. According to a preliminary investigation by SMM, electrolytic nickel production continued to be stable in June, with production falling by about 2.56 per cent from May to 12600 tons, also affected by the reduction in natural days.

Nickel pig iron:

In May, the national nickel pig iron decreased by 0.31 per cent to 47800 nickel tons, an increase of 28.13 per cent over the same period last year. In terms of taste, the output of high nickel pig iron in May decreased by 1.58 to 41000 nickel tons compared with April. Although the output of large factories in Shandong continues to be released, due to the impact of environmental protection at the end of May in Shandong and Jiangsu, factories have been overhauled in North and South China. The increment was offset and production fell. Production of low nickel pig iron increased by 8.14 per cent to 6800 nickel tons in May, mainly due to the resumption of production at a low nickel iron plant in East China at the end of April and the end of maintenance at the Northern Steel Plant in late May.

National nickel pig iron production is expected to increase by 4.59 per cent to 50000 nickel tons in June compared with the previous month, of which high nickel pig iron production increased by 5.20 per cent to 43100 nickel tons, mainly due to the fact that the factory maintenance plan in June was less than that in May, and no environmental incidents have been heard yet. The production of low nickel pig iron increased by 0.94 per cent to 6900 nickel tons compared with May, mainly due to the continued production of the North Steel Plant and the East China recovery Plant, but partly offset by the conversion of the East China Plant and the overhaul of the South Steel Plant.

Nickel sulfate:

In May, China produced 11440 tons of nickel sulfate, with a physical output of 52000 tons, a month-on-month ratio of 5.8 percent, an increase of 32.15 percent over the same period last year. On the one hand, the increase comes from a nickel sulfate plant in the north, where production was limited in April, while production resumed in late May and increased compared with the previous month; on the other hand, new nickel sulfate capacity built in several precursor plants and nickel sulfate plants continued to release increments. However, affected by the imminent end of the subsidy transition period for the new energy industry and the fire incident, the supply and demand side of nickel sulfate has initially shown signs of weakening this month, and the overall sales situation is not satisfactory. Some of the precursor integration plants have reduced production of their precursors and nickel sulfate, while plants with previous plans to expand production have also suspended the construction of new production capacity. National nickel sulfate production may continue to increase in June, with a month-on-month increase of 3.62 per cent to 53900 tons, mainly due to the resumption of production in the northern nickel sulfate plant.

Refined tin:

Refined tin production in May was 13734 tons, down 1.27 per cent from April. In May, the output of most smelters was relatively stable, and some smelters reduced their production due to the shortage of tin ore and waste materials, while the output of some tin factories in Jiangxi decreased in May due to equipment maintenance, but normal production has now returned to normal. At present, the supply of tin ore raw materials has remained tight. Due to drought, some concentrators in Myanmar have suspended production. If the rainy season comes in the future, the transportation of raw materials will also be affected. It is expected that in the future, the short-term raw materials will continue to maintain a tight state to affect the production of the smelter, and the domestic refined tin production is expected to drop to 13300 tons in June.

Description:

1. The value with * is the modified value, and the value of italics is the predicted value.

2. The output of nickel pig iron refers to the data after the physical quantity is converted into metal.

Research methodology:

1) Research methods

SMM production survey is conducted by professional analysts by telephone, field research and other methods, regular monthly tracking of Chinese metal production enterprises, and based on this to issue a report on China's metal production.

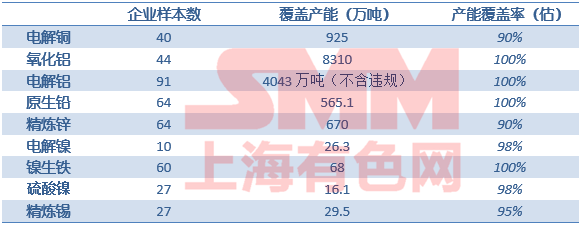

In the process of research, ensure the basic coverage ratio of the sample, and continue to expand; at the same time, consider the production capacity scale, regional distribution, enterprise nature and other detailed factors to reasonably select and distribute the sample, so that each itemized data is representative.

The production data include last month's output (initial value), the previous month's output (revised value) and the forecast for the current month's production. In general, SMM rarely modifies the output, that is, the correction value = the initial value, but still retains the possibility of correction.

Before the 10th of each month, it was released through the official website of SMM (www.smm.cn), WeChat Subscription account (Today Nonferrous), mobile phone station (m.smm.cn) and other official channels.

2) sample introduction

"[investment must see] Trade friction news flying all over the metal how to win in chaos?

"Click to enter the registration page

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business