SMM November 18 News:

Entering November, overseas miners have successively released their Q3 reports. In terms of production, the Tizapa mine resumed production in Q3, and the Kipushi mine continued to ramp up, leading to a sequential increase in zinc concentrate output. However, production disruptions such as power outages, earthquakes, and declining raw ore grades persisted, while significant reductions were also observed at mines like Antamina and Red Dog. What are the specific details?

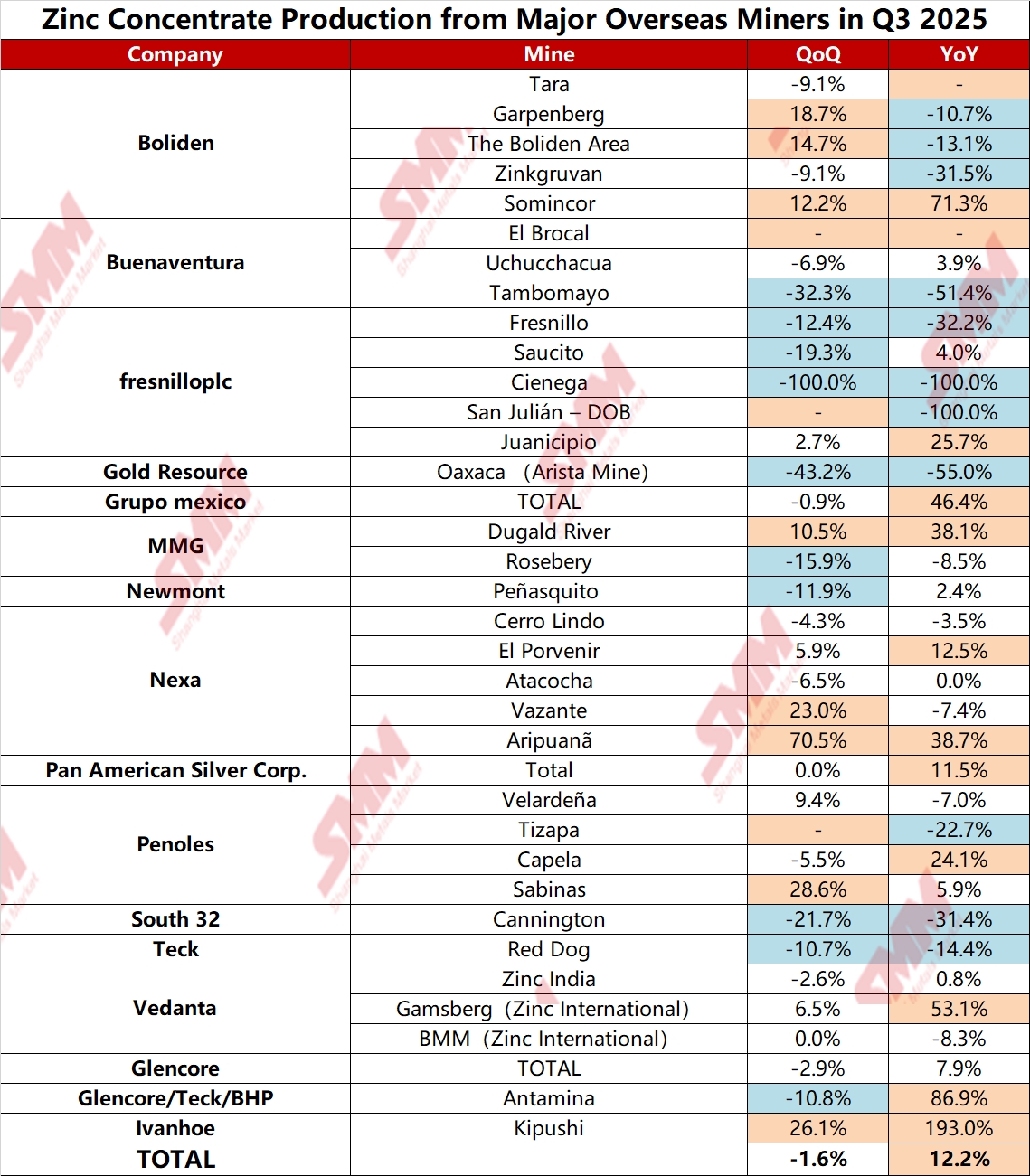

SMM compiled production statistics for 16 major overseas miners. According to the disclosed financial reports, the combined zinc concentrate production of these 16 miners in Q3 2025 totaled 1.3062 million mt, up 141,600 mt (12.2%) YoY compared to Q3 2024, but down 21,500 mt (1.6%) QoQ from Q2 2025. The chart below shows the changes in zinc concentrate production for each miner in Q3 2025 as compiled by SMM.

By miner:

- Boliden: Zinc concentrate production in Q3 totaled 108,000 mt, including production from the Somincor and Zinkgruvan mines, which began to be included from April 16. This represents a 16% increase QoQ and a 140% increase YoY. The report disclosed that zinc concentrate production at the Boliden Area in Sweden was 12,200 mt in Q3, production at the Tara mine was 18,600 mt, production at the Garpenberg mine in Sweden was 27,700 mt, production at the Zinkgruvan mine in Sweden was 20,200 mt, and production at the Somincor mine in Portugal was 29,300 mt.

- Buenaventura: Zinc concentrate production in Q3 2025 was 7,000 mt, down 9% QoQ and down 5% YoY. The report disclosed that the El Brocal mine in Peru produced almost no zinc concentrate in Q3; production at the Uchucchacua mine in Peru was 6,400 mt, and production at the Tambomayo mine in Peru in Q3 2025 was 600 mt.

- MMG: Zinc concentrate production in Q3 2025 was 58,700 mt, up 5% QoQ and up 26% YoY. By mine, benefiting from strong mining and beneficiation plant recovery rates due to operational improvements, Dugald River's zinc concentrate production in Q3 was 48,100 mt, up 38% YoY; due to grade decline from mining sequence, Rosebery's zinc concentrate production in Q3 was 10,600 mt, down 8% YoY. Its 2025 production guidance is 170,000-185,000 mt and 45,000-55,000 mt, respectively.

- Newmont: Zinc concentrate production in Q3 2025 was 59,000 mt. The mine's 2025 production guidance is 236,000 mt.

- Nexa: Total zinc concentrate production in Q3 2025 was 83,700 mt, up 14% QoQ, mainly attributable to improved performance at the Vazante mine and a quarterly production record at the Aripuanã mine, partially offsetting slight production declines at the Atacocha and Cerro Lindo mines.

- Pan American Silver Corp: Total zinc concentrate production in Q3 2025 was 12,600 mt, up 13% YoY. The miner's 2025 zinc concentrate production guidance is 42,000-45,000 mt.

- TECK: Red Dog's zinc concentrate production in Q3 2025 was 122,000 mt, down 11% QoQ and down 14% YoY, both due to lower grades, in line with mining plan expectations. The mine's 2025 production guidance is 430,000-470,000 mt, its 2026 guidance is 410,000-460,000 mt, and its 2027 guidance is 365,000-400,000 mt.

- Vedanta: Total zinc concentrate production in Q3 2025 was 318,000 mt, down 1% QoQ but up 6% YoY. Zinc India's total zinc concentrate production in Q3 2025 was 258,000 mt, up 1% YoY; Zinc International's zinc concentrate production in Q3 was 60,000 mt, up 36% YoY, mainly due to increased tonnage processed and higher grades, with significant output growth at the Gamsberg mine.

- Glencore: Own-sourced zinc production in Q3 2025 was 244,200 mt, up 8% YoY, primarily due to higher zinc grades at Antamina and increased production at McArthur River. Its 2025 own-sourced zinc production guidance has been adjusted to 950,000-975,000 mt.

- Antamina: Zinc concentrate production in Q3 2025 was 126,700 mt, up 87% YoY. Its 2025 zinc concentrate output guidance is 422,000-467,000 mt.

- Ivanhoe: The Kipushi mine's zinc concentrate production in Q3 was 52,700 mt. Its 2025 production guidance target is 180,000-240,000 mt of zinc.

Market Outlook

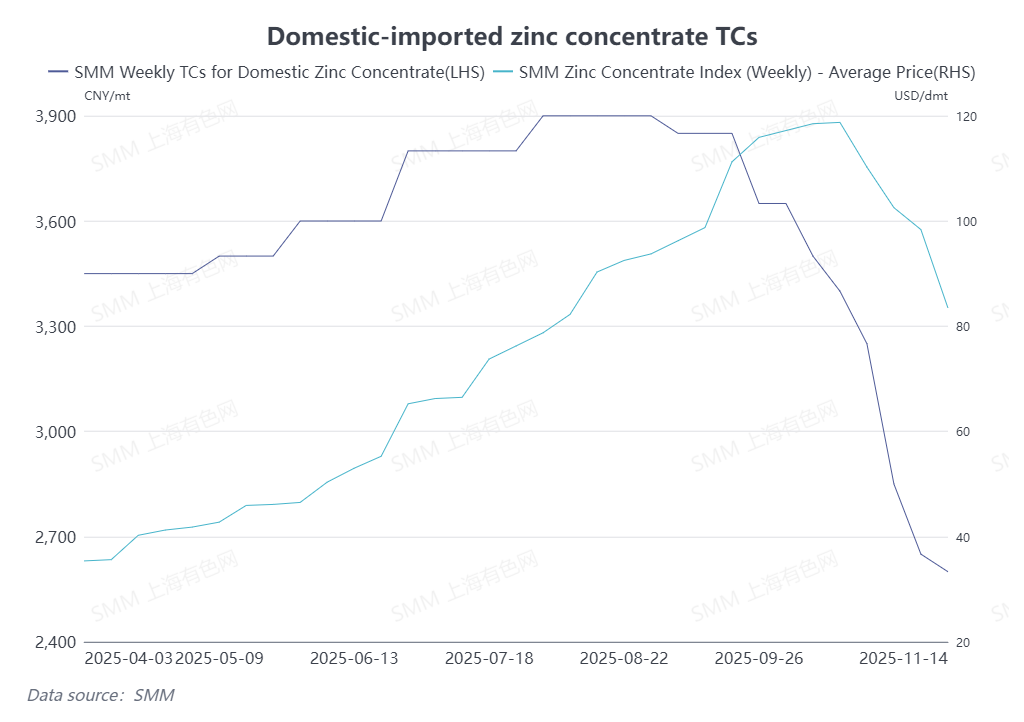

On a YoY basis, overseas zinc concentrate production continued to grow in Q3, and China's zinc concentrate imports remained high this year. However, entering Q4, as domestic smelters enter the winter stockpiling phase, domestic zinc concentrate supply has become periodically tight, and both domestic and imported zinc concentrate TCs have shifted to a downward trend. Looking ahead, zinc mine capacity at projects like Gamsberg, Ozernoye, and Kipushi is expected to continue increasing next year, the Romina zinc mine is scheduled to commence production in 2026, the Endeavor zinc mine's output is expected to continue recovering in 2026, and domestically, mines like Huoshaoyun will continue ramping up. Overall, SMM expects global zinc concentrate production to increase by over 400,000 mt in metal content YoY in 2026. However, considering that smelter production both domestically and overseas is also expected to grow significantly next year, the global zinc concentrate supply-demand balance is projected to tighten slightly in 2026 compared to 2025, with China's zinc concentrate market expected to be in a deficit. Under this scenario, there is a risk of the center of domestic zinc concentrate TCs declining next year.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)