SMM November 6 News:

As of October 31, the most-traded SHFE zinc contract closed at 22,355 yuan/mt, down 10 yuan/mt for the month, a decline of 0.04%. In October, zinc prices fluctuated considerably, hitting a low of 21,800 yuan/mt mid-month before rebounding in the second half of the month to a high of 22,540 yuan/mt by month-end. The price center for October saw a slight increase compared to September. However, as November begins, with winter stockpiling underway, domestic zinc concentrate supply appears tight. Will zinc prices continue to rise?

Macro perspective. In October, the US Fed cut interest rates as expected, aligning with prior market expectations. Additionally, progress in US-China tariff negotiations has been positive, with the 24% tariff on China postponed. Market macro sentiment is relatively favorable. However, the ongoing US government shutdown has delayed economic data releases, leading the market to adopt a wait-and-see attitude toward further Fed rate cuts. Recently, macro factors have provided limited support for zinc prices. Continued attention to subsequent US data releases is necessary for more macro guidance.

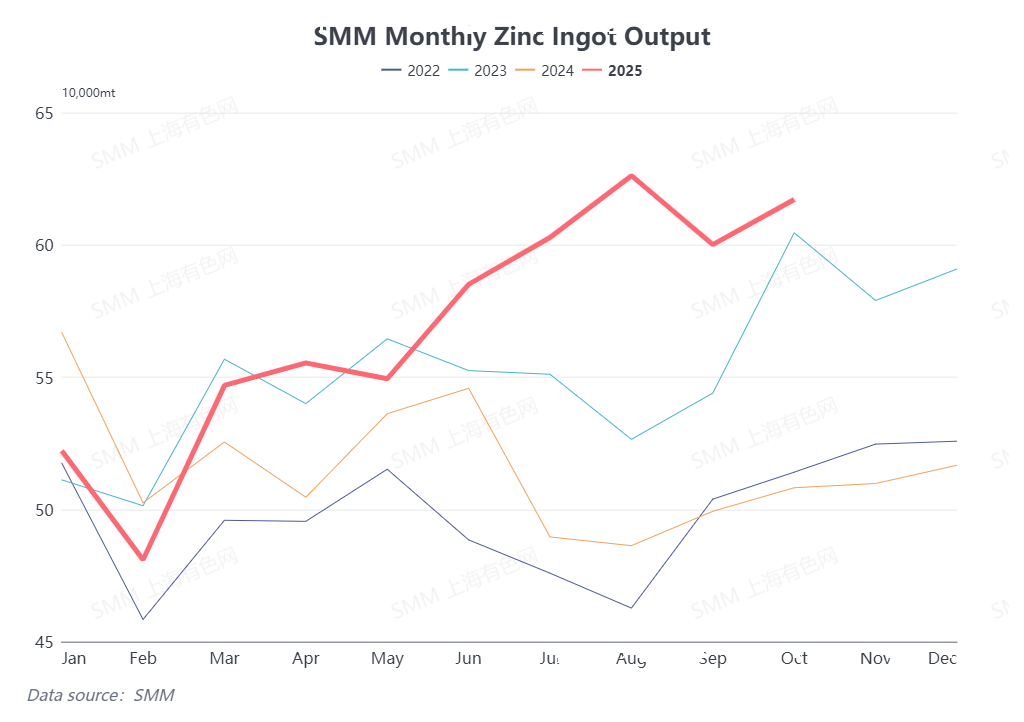

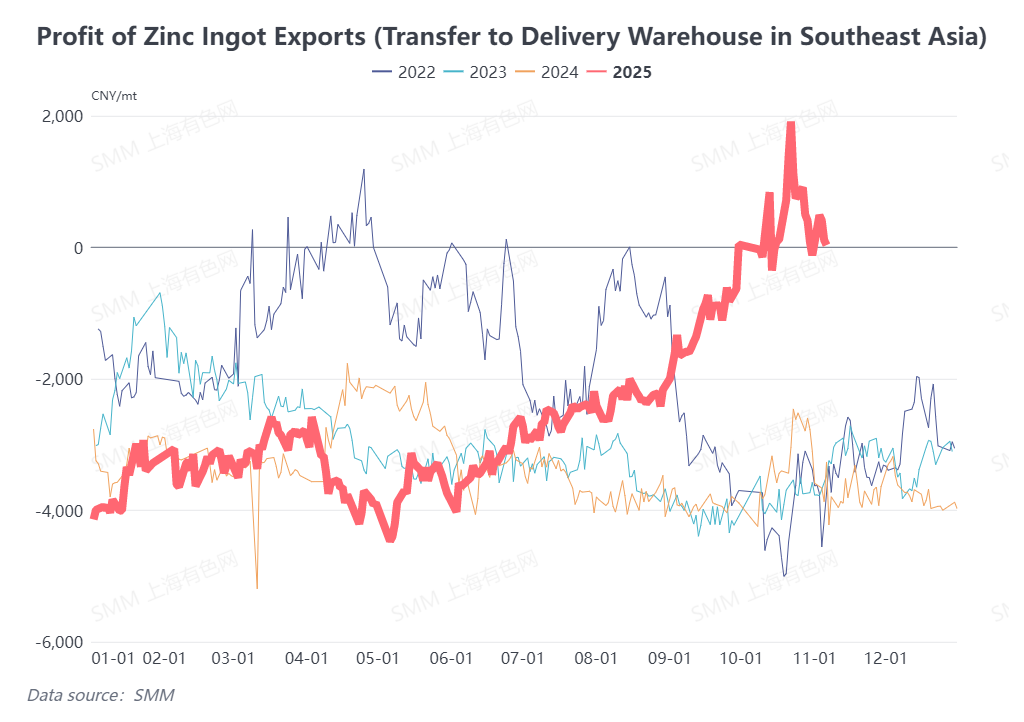

Supply side. According to SMM, China's refined zinc production in October increased MoM to around 610,000 mt, with zinc ingot supply continuing to grow. Entering November, as domestic zinc concentrate TCs fall rapidly, smelters face increased pressure in raw material purchases, and raw material inventory has declined. Some smelters have consequently cut production. SMM expects zinc ingot production in November to decrease slightly compared to October, but overall zinc ingot supply remains strong. Furthermore, the zinc ingot export window remained open in October and November, with Chinese zinc ingots continuously being exported to Southeast Asia or shipped to LME delivery warehouses. Smelters still show willingness for future zinc ingot exports, and export expectations are providing some support to domestic zinc prices.

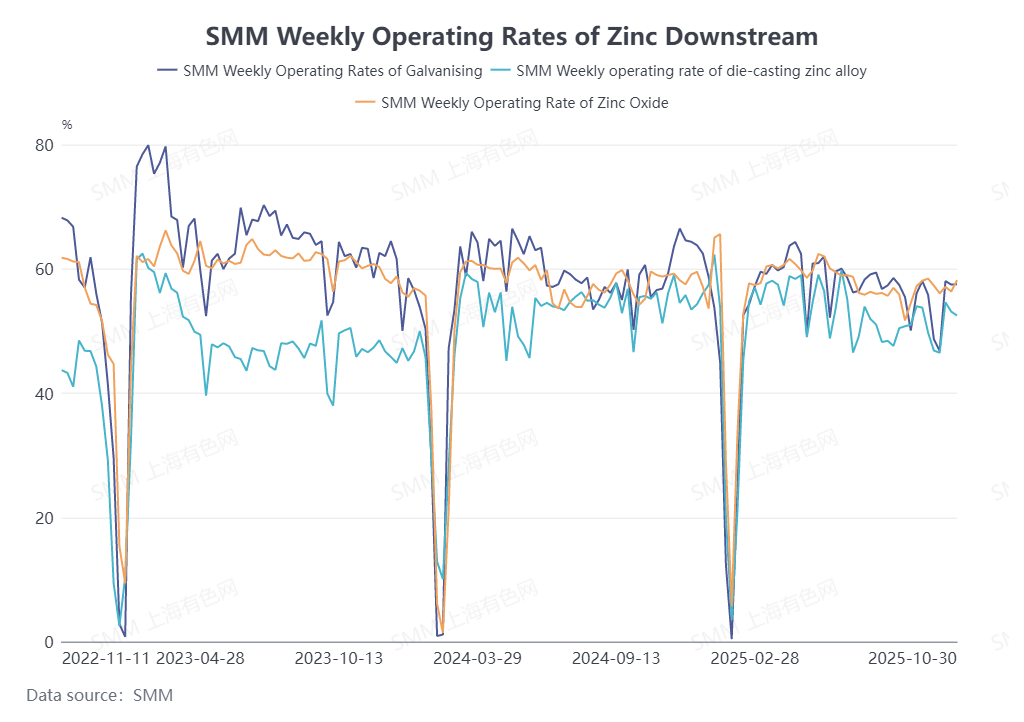

Demand side. As November begins, the conventional peak consumption season has passed. Orders in some galvanizing sectors have already declined, with some enterprises cutting or halting production. The alloy sector also saw lower operating rates, and export orders showed no growth. Zinc oxide orders also face potential reduction risks. Overall, domestic zinc downstream consumption in November is expected to weaken MoM compared to October, with demand providing limited support for zinc prices.

Outlook for November. Currently, there is no clear guidance from the macro perspective, while structural risks from the LME market backwardation persist. With the zinc ingot export window remaining open, domestic zinc prices are expected to hold up well. However, considering the increasing risk of weakening consumption on the fundamentals side, the upside for zinc prices may be somewhat constrained. Continued attention to subsequent zinc ingot export performance is necessary.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)