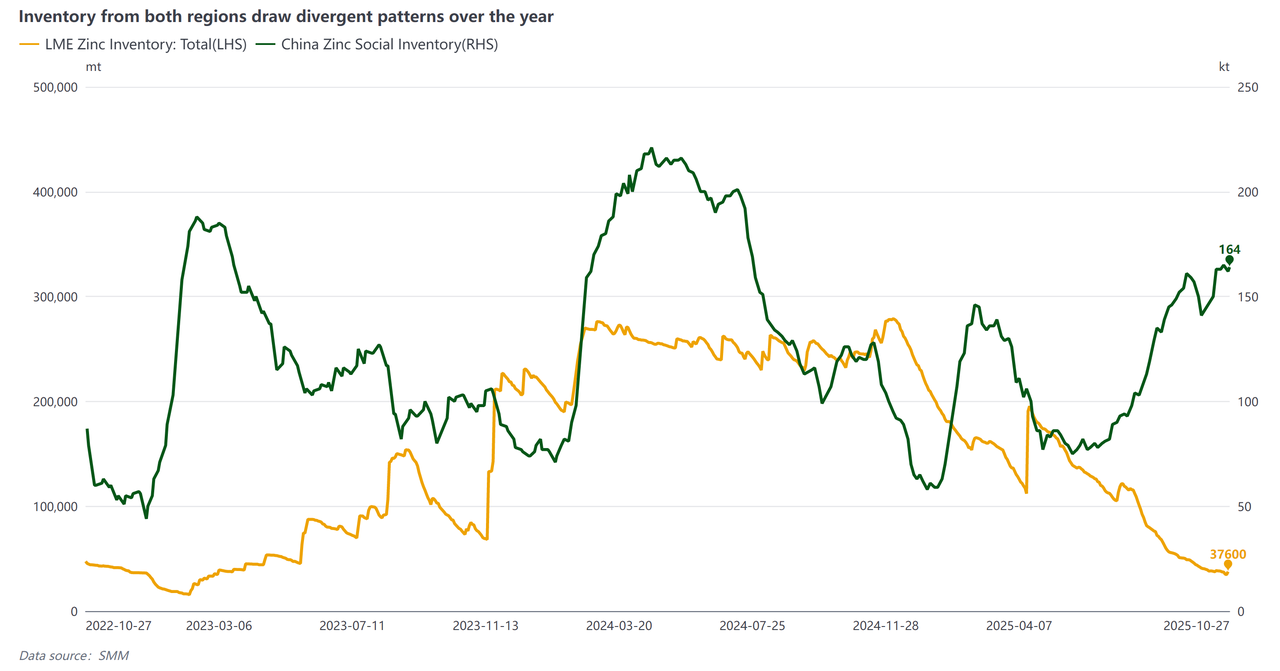

LME inventories at 2-year lows while China's in surplus

Zinc has surprised the market with its strong performance in the recent days, making it hard to believe that its fundamentals were not at all bullish just around 5 months ago. Inventories have plunged to extremely low levels in the global zinc market outside China. As of 22th of October, LME zinc stocks have headed down to roughly 34,700 tons, with only 24,850 tons of on-warrant inventory immediately available for pick up, this is barely sufficient to cover one day of global zinc consumption. Comparing with the level at the start of the year (230,325 tons), LME inventory saw a drawdown by around 85%. Currently, these levels are near 2-year lows since Feburary 2023, seemingly with continued downwards momentum, fueling intense market concern over a supply squeeze.

In contrast, zinc inventories within China have been building: China’s social zinc ingot stocks recently climbed to around 162,000 tons on 23th of October, up sharply from roughly 100,000 tons in the first half of the year. This is leading to a severe divergence – critically low inventories overseas versus rising stocks in China, highlighting a global market that is heading towards two different directions, with acute shortage in the ex-China region and a good level of surplus in China.

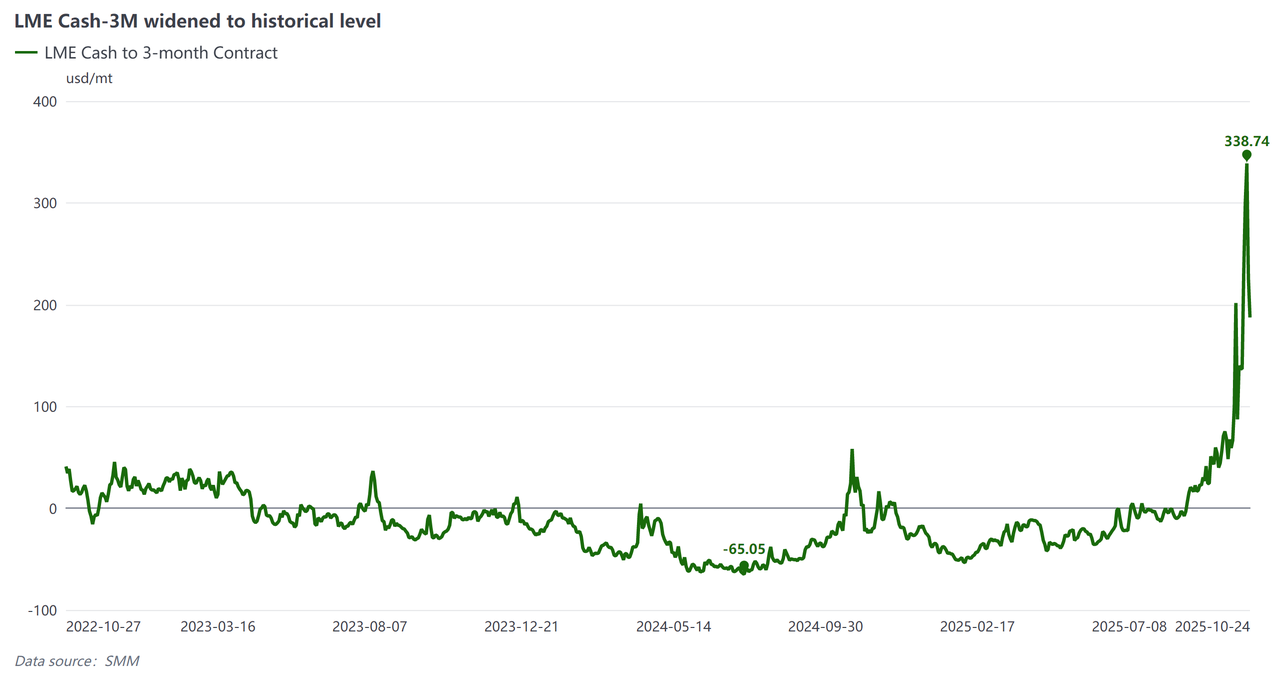

Record backwardation and short squeeze now playing out at LME

Following the continued destocking of inventory, LME zinc market has swung into an unprecedented backwardation, signaling a short squeeze. On 21th October, LME Cash-3M zinc spread once exploded to a $323 per ton – the widest level since at least 1997. This extreme price inversion is a sign of acute near-term shortage, and it indeed also suggests towards a classic squeeze. According to the data reported by LME, the top six entities with long positions in near-term contracts are collectively holding more than 300% of the available stock in LME warehouses. With so little metal on hand, short position holders without physical metal handy are facing steep losses, evidenced by the fact that Tom/Next spread is spiking to $30/ton – the highest since the 2022 squeeze. With backwardation still deepening and rolling cost building up to this level, bears now head into a dilemma: Either cover now and take the loss, or bear with the rolling cost and roll into later months, risk getting squeezed even harder, none of which seems to be a good option.

Where did the metal actually go to?

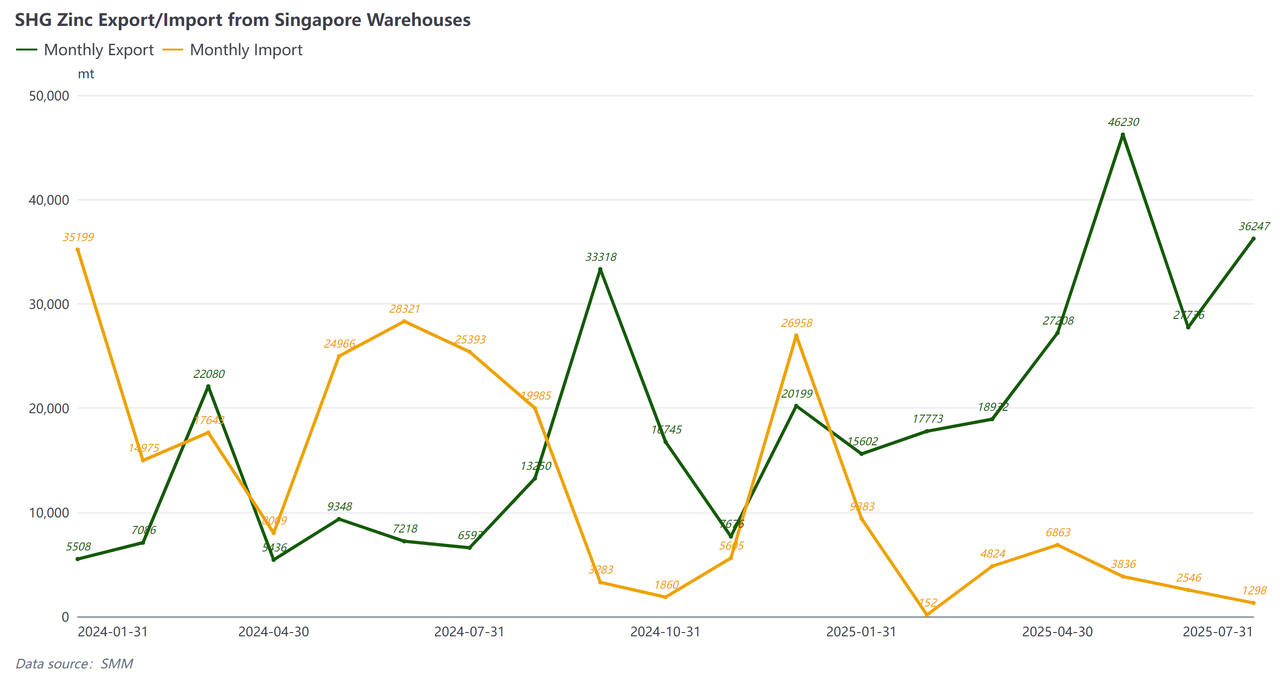

Historically speaking, in the year of 2024, we saw large volumes of metal being cancelled and then re-warranted in LME warehouses, namely the Singapore warehouse, as trading houses and warehouse operators engaged in “rent-sharing” deals that shuttled metal in and out to split storage fees. This would eventually lead to fluctuating stock levels and changing structure, while the actual metal does not necessarily need to clear the border. This year, however, the zinc leaving LME warehouses has not flowed back as before. Once warrants are cancelled, the metal does not return to the LME system anymore.

According to the customs data from Singapore, where most of the LME zinc inventories are being held in the past couple of years, the total export on SHG zinc ingots has risen dramatically after May 2025, reaching over 50,000 tons in August. Meanwhile in comparison, the total import has gone all the way downwards. In the first 7 months of 2025, the total export volume reached 189,700 tons, already exceeding the full-year export volume from Singapore in 2024, which stood at only around 154,500 tons; the YTD import volume in 2025, however, remained at 28,900 tons, representing a substantial YoY decrease of 81.3%. Metals are physically flowing outside of Singapore this time, and do not seem to come back to our sight.

So, where have they gone? According to Singapore’s customs data, these metal outflows have been directed primarily to the emerging markets with downstream demand to absorb the material, for example major Southeast Asia countries (Vietnam, Malaysia, Indonesia, etc.), Middle East and India. These regions are traditional net importers of refined zinc, where the actual demand for this galvanizing metal stays strong, yet the local capacity remains limited. Presumably, while the amount of metals sent to these regions is more than enough to supplement the local demand, a portion of this metal might have went directly into the local spot market for consumption, another portion was re-exported to other end users further down the supply chain, with the rest of it ended up held as off-warrant inventory outside the LME system. According to ILZSG’s latest figures, demand from these regions is projected to rise by only around 0.8%. With this in mind, it is highly likely that a significant proportion of the products entering these markets was eventually re-exported elsewhere, or remained within the local off-warrant inventory system.

It is also worth noting that in August 2025 alone about 20,000 tonnes of zinc were shipped from Singapore to the US. A part of the zinc stocks appears to have been shipped early to the United States in anticipation of a potential Section 232 tariff action on zinc. The US government launched a Section 232 investigation into critical minerals, including zinc, in April 2025, raising expectations that tariffs on refined zinc imports might be imposed. Facing this policy uncertainty, some traders might have enough motivation to move metal into the US ahead of the investigation’s conclusion – aiming to take advantage of the high US zinc premiums while getting ahead of any potential import tariffs.

Behind the regional imbalance - Why is China outperforming ex-China?

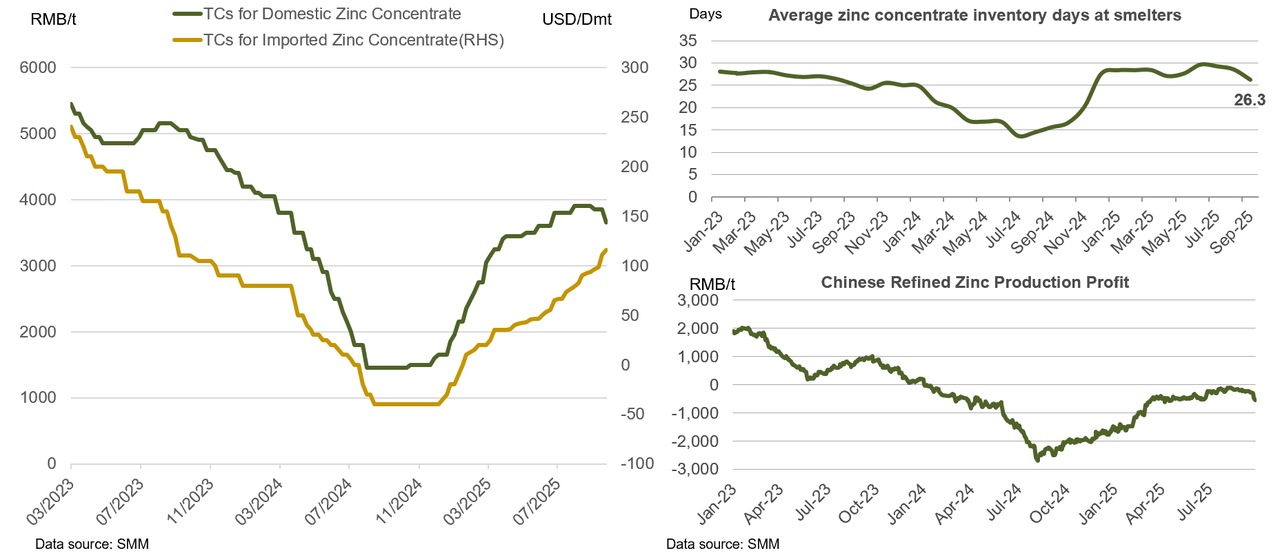

Since 2025, Chinese zinc smelters have quickly recovered from the pain from last year. Benefitted by increasing level of raw material supply from both domestic mining projects and imported zinc concentrates, smelters on average have around 1 month's raw material ready in their inventory, according to SMM survey. Gaining more power in the negotiations, spot TC also started to climb up. With by-products' prices (e.g. Silver, gold, sulphric acid) also fairly solid and favourable, the refining margin for Chinese producers has been quite decent.

Meanwhile, ex-China smelters are still struggling with high operating costs, lower TCs, and several shutdowns or outages. Nyrstar’s Hobart plant previously announced a 25% production cut starting from April 2025. Young Poong’s Seokpo smelter has just resumed operations after a two-month suspension due to environmental compliance issues, while Teck’s Trail operations voluntarily lowered its production plan for 2025.

Low raw material availability and high energy costs remain common challenges for European smelters. Odda’s 150 ktpa expansion project is the major addition to the ex-China refining market; however, its ramp-up progress has been negatively affected by a shortage of intermediates.

With demand staying relatively flat in both China and ex-China, divergence between regional supply has eventually led to regional imbalance. SMM estimates that there will be a huge surplus in refined zinc of around 290,000 tons in China, whereas ex-China still has a deficit of about 90,000 tons.

China’s export window - What and when shall we expect?

With an evident regional imbalance, a key question is when Chinese smelters will seize the arbitrage and start exporting zinc in volume. As the price gap between LME and SHFE widens, export economics improve.

Refined zinc ingots in China are subject to a 13% value-added tax (VAT). The tax rebate for exported zinc ingots was removed in 2008, meaning that exporters must bear this cost themselves. SHG zinc ingots are nominally subject to a 20% export tariff, the rate has been temporarily set at 0% for 2025. As such, in order for Chinese producers to initiate bulk export, the exporting profit needs to be wide enough to cover:

1) 13% VAT;

2) Shipping fee (Ocean freight + Inland freight);

3) Insurance premium (Based on CIF terms);

4) Miscellaneous charges where applicable.

By the time of writing (24th October), SHFE/LME ratio is at about 7.35, Chinese zinc imports would incur losses of 5,000–6,500 yuan/t. The theoretical profit for exporting zinc to LME Singapore warehouse was at 1,128 yuan/t, and to Southeast Asia spot market was 1,769 yuan/t, which is already enough to support export to both spot market and LME system.

However, the issue of quotation period (QP) is still a crucial factor in determining the actual export margin. Under the current backwardation structure, most local buyers from southeast Asia are reluctant to price their cargoes against the LME cash quotation. Instead, they prefer to fix the QP on a forward month such as November. However, for Chinese exporters, only pricing on the LME cash basis would be profitable. If the deal is priced on a forward QP, the exporter will effectively lose the backwardation — the profit will be eroded by the deep spread between cash and 3-month price, which weighs on Chinese exporters’ interest of shipping their zinc ingots abroad.

Based on China Customs statistics, China has exported 2,478 tons of refind zinc in September, marking a MoM increase of 696.96%. YTD China has exported 15,602 tons of refined zinc in 2025, representing a culmulative YoY increase of 32.75%. SMM estimates that the export volume could rise to roughly 10,000 tons in October, which could further alleviate the LME’s extreme tightness and abnormal spreads.

However, we do not think that China would be a net exporter of zinc in the upcoming year, neither do we think that the export window will remain open for long. The last time Chinese producers initiated export was in 2022 when the energy crisis heavily struck the production of refined zinc in Europe, leading to curtailment of smelters' production (e.g. Nyrstar Budel、Glencore Portovesme) and a long-lasting situation of undersupply. Window remained open for 3-4 months before price rebounded in China, SHFE/LME ratio headed up from around 6.3 to 7.8 and arbitrage window closed down. This time around, the production problem in ex-China is not as severe as it used to be in 2022 energy crisis. The price spread is likely to narrow quickly once visible improvements in inventories emerge, arbitrage window for export is therefore not expected to last long.

Outlook: Spreads, Inventories and regional rebalancing

From the global perspective, refined zinc market all over the globe is still in a surplus, with 200,000 tons of surplus projected for this year and 280,000 for 2026. In the mid to long term, the zinc market’s extreme structure is likely to adjust and normalize over time, but the exact timing will hinge on several key triggers.

The foremost catalyst is the Chinese export. If the arbitrage window remains open, many expect China’s zinc exports to grow in the coming months. As more Chinese metal reaches LME warehouses, LME stocks should eventually bottom out and start rising, easing the immediate physical squeeze and narrowing the steep spreads. On 23th October, LME warehouses in Singapore received an inflow of around 2,500 tons. Although the volume is not large, it serves as a signal that fresh metal is starting to arrive in the LME system.

Secondly, the potential return of ex-China smelter capacity could lift supply. Given that Hobart received government funding to support its smelting business, Trail reported improved Q3 profit margin and Seokpo smelter still on its way of recovering, together with higher zinc prices and TCs, ex-China smelters are discovering their own ways to come back to the game. Although such relief is rather limited in the near term and more focused on the long term, these could potentially increase refined supply and help rebuild inventories.

Thirdly, high zinc prices may possibly attract invisible stocks to flow back into the LME system. However, if most of the physical metal is controlled by dominant player who maintains substantial long position and is under no immediate liquidity pressure, there is little incentive for them to release material into the market. The current ratio of open interest to on-warrant inventory gives them strong leverage over the near-term market. By withholding stocks they can tighten the nearby market and short-squeeze to extract greater returns from the backwardation. There is also a possibility that some market participants may be motivated to keep zinc prices elevated ahead of annual benchmark and long-term contract negotiations for 2026. Maintaining a stronger LME cash price or a tighter nearby spread could help strengthen the seller’s position in discussions on TCs, premiums or annual pricing formulas. Given the current market concentration and the limited liquidity, such an incentive-driven tightening cannot be ruled out, there still remains a big question mark over how much off-warrant inventory can actually be encouraged to return to the LME system.

Another “X-factor” that could influence the pace of LME stock replenishment is the outcome of the ongoing US Section 232 investigation. Since the US government is apparently "on holiday", we might need to wait longer before the result unveils. If the investigation concludes that import tariffs will be imposed on SHG zinc ingots, US domestic supply tightness will likely persist, and the LME system could face another setback as metal inflows into the US would remain constrained. Conversely, if the outcome shows no additional tariffs, the high US premiums may soften. In that case, high zinc price could attract some of the metal currently sitting in the US to be delivered into the US LME warehouses, supporting the recovery of visible inventories.

In all likelihood, metals need to find their way from all over the world back to the LME system, no matter where they come from, which allows LME inventory to stabilize. Until then, continued spread volatility and squeeze risks should remain. Ultimately, after the gradual global rebalancing happens and the deep backwardation gets softened, the zinc market should revert to fundamentals-driven pricing and a more normal forward structure – but the speed of that normalization will depend on how the above triggers actually unfold.

Author: Yueang He, Zinc & Lead Analyst of SMM UK

Contact: yueanghe@smm.cn | +44 (0)7522 173725

![Strong Bottom Support in Zinc Fundamentals, Limited Downside Expected [SMM Zinc Morning Comment]](https://imgqn.smm.cn/usercenter/ipTIN20251217171755.jpg)

![Persistent Global Inflation Concerns; LME Zinc Posts Five Consecutive Down Sessions [SMM Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/cirme20251217171754.jpg)

![Stronger US Dollar Weighed on SHFE Zinc, Which Slipped in Daytime Trading [SMM Zinc Futures Brief Commentary]](https://imgqn.smm.cn/usercenter/EviJV20251217171754.jpg)