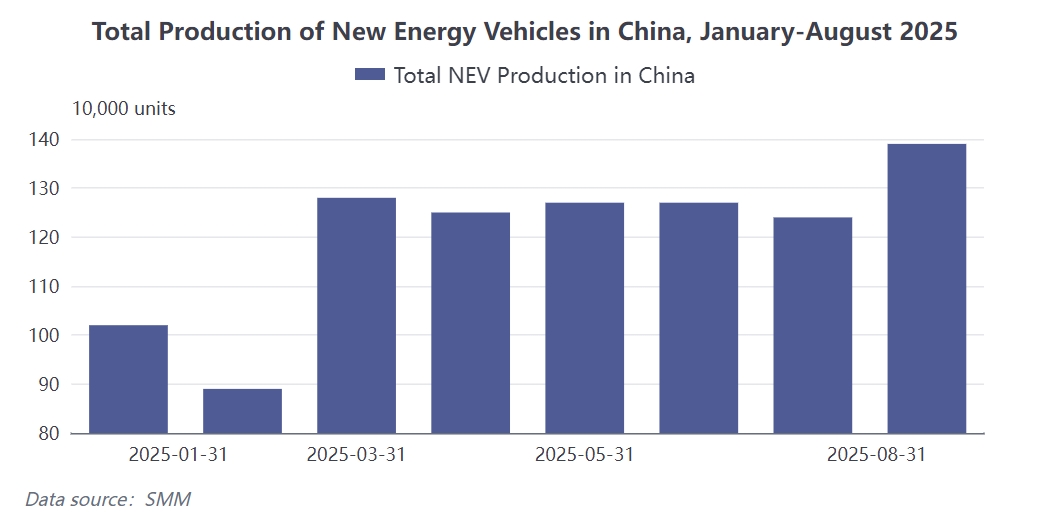

In August 2025, China's NEV production reached 1.39 million units, up 12% MoM and 27% YoY. This data indicates that NEVs have further solidified their position as the largest end-use consumption sector for rare earth magnetic materials.

According to SMM statistics, from January to August 2025, China's EV sector consumed approximately 40,800 mt of NdFeB permanent magnets. With the arrival of the traditional September-October peak season, NEV production in September is expected to reach 1.55 million units, up 11.5% MoM, corresponding to a consumption of approximately 6,638 mt of magnetic steel.

The NEV industry has entered a stage of large-scale, rapid development, driving sustained growth in demand for magnetic materials. The annual growth rate of NEVs in 2025 is projected to be between 20% and 25%, slightly lower than the 34.75% in 2024 and 35.31% in 2023, but still maintaining a relatively high level. This growth directly translates into robust demand for magnetic materials. The NdFeB demand per NEV ranges from 2.7 kg to 7.0 kg, influenced by factors such as the car model, electric drive technology solution, magnetic material technology solution, and rare earth prices. Generally, lower-end vehicles use less, while commercial vehicles and high-end cars require more NdFeB. This variation in demand reflects the value stratification of magnetic materials across different vehicle price segments. The cumulative consumption of 40,800 mt of NdFeB permanent magnets from January to August 2025 underscores the position of NEVs as the largest application field for magnetic materials. With the continuous increase in NEV penetration, the structural growth in demand for magnetic materials has become a major driver of industry development.

With the arrival of the traditional consumption peak season of September-October, the NEV market has entered a new growth cycle. The expected production of 1.55 million units in September, up 11.5% MoM, demonstrates strong demand momentum during the peak season. Correspondingly, the consumption of magnetic steel is projected to reach 6,638 mt, indicating that the scale of monthly demand continues to expand. The peak season effect is reflected not only in volume growth but also in the optimization of the demand structure. The technical requirements for magnetic materials in NEVs are significantly higher than those in traditional application fields. Due to the need for temperature and corrosion resistance in electric drives, traditional low-end grades cannot meet these demands; only high-end grades of UH level and above can effectively fulfill the requirements. This elevation of technical thresholds is driving the continuous upgrading of the magnetic material product structure. The increasing proportion of high-end magnetic materials reflects the stringent performance requirements imposed by the NEV industry on material properties.

Driven by both demand boost and technological upgrades, the magnetic material industry is undergoing profound structural changes. Further concentration has become the most notable trend. Currently, UH-grade and above products are increasingly concentrated in the hands of top-tier and leading mid-tier manufacturers. According to incomplete statistics from SMM, the proportion of UH-grade and above products in some top magnetic material enterprises can account for over 90% of their monthly production. This trend toward concentration stems mainly from two pressures: on one hand, new energy vehicle manufacturers are imposing increasingly stringent cost-reduction requirements; on the other hand, rising rare earth prices have intensified cost pressure. Under these circumstances, large enterprises with strong technical capabilities and significant scale advantages are more competitive. Top-tier enterprises are outpacing mid-tier ones in terms of orders and capacity, leading to a concentration of resources in dominant players. This divergence is expected to accelerate industry consolidation and drive the magnetic material industry toward high-quality transformation. From the perspective of the industry chain, magnetic material enterprises need to simultaneously address the dual challenges of upstream raw material price fluctuations and downstream customer demand changes. This requires enterprises not only to possess R&D capabilities but also to have supply chain management expertise and advantages in large-scale production.