SMM September 26 News:

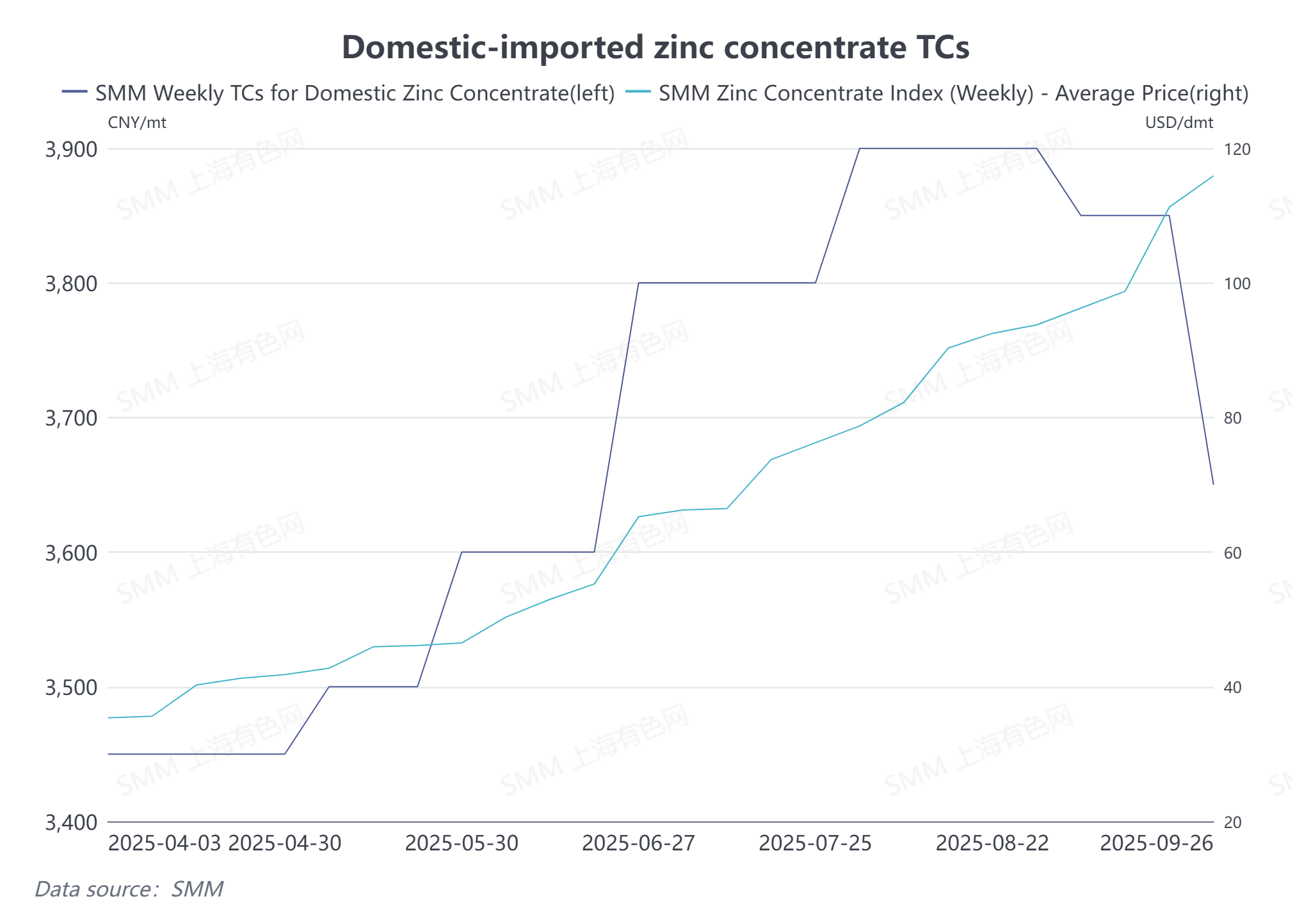

According to SMM data, as of September 26, the weekly average SMM Zn50 TC fell 200 yuan/mt in metal content MoM to 3,650 yuan/mt in metal content, while the imported zinc concentrate index rose $4.65/dmt MoM to $115.9/dmt. Domestic zinc concentrate TCs have already peaked and began a downward trend in October. What are the specific reasons?

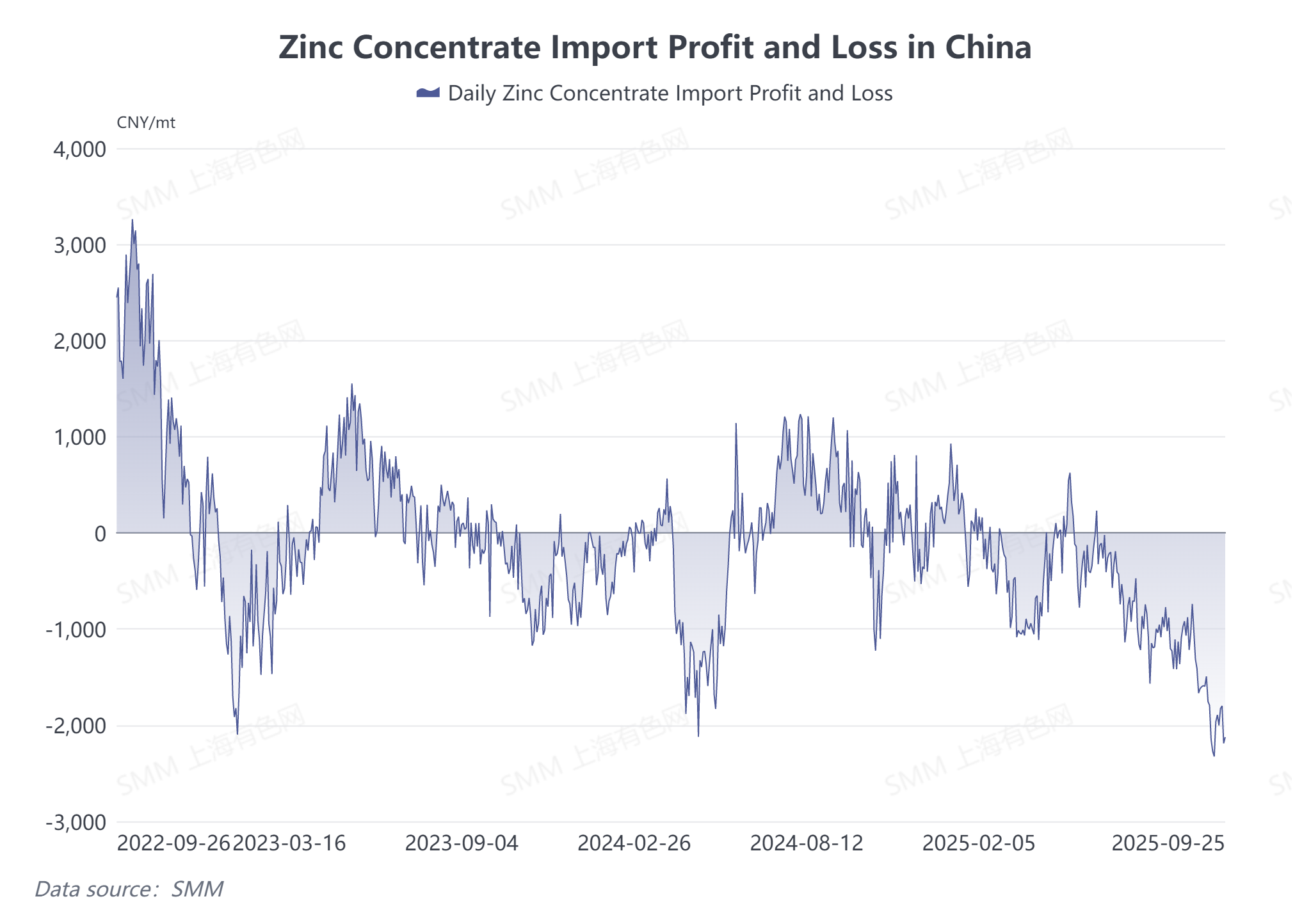

From the SHFE/LME price ratio perspective, China's zinc concentrate import profit margin has been continuously declining since May. By September 25, the import loss had widened to 2,000 yuan/mt in metal content. For smelters, this means that, for the same grade and metal content, the price of imported zinc concentrate is about 2,000 yuan/mt in metal content higher than domestic zinc concentrate recently, giving domestic zinc concentrate a significant price advantage. Against this backdrop, domestic smelters are actively procuring domestic zinc concentrate, showing strong demand for it.

From a timing perspective, following the usual annual pattern, some zinc mines in northern China will gradually reduce or halt production starting in November, with domestic zinc mine production expected to decline in Q4. In response, some domestic smelters have begun winter stockpiling, actively purchasing zinc concentrate raw materials to mitigate the impact of reduced supply. However, the resulting robust raw material demand is exerting some inhibitory pressure on domestic zinc concentrate TCs.

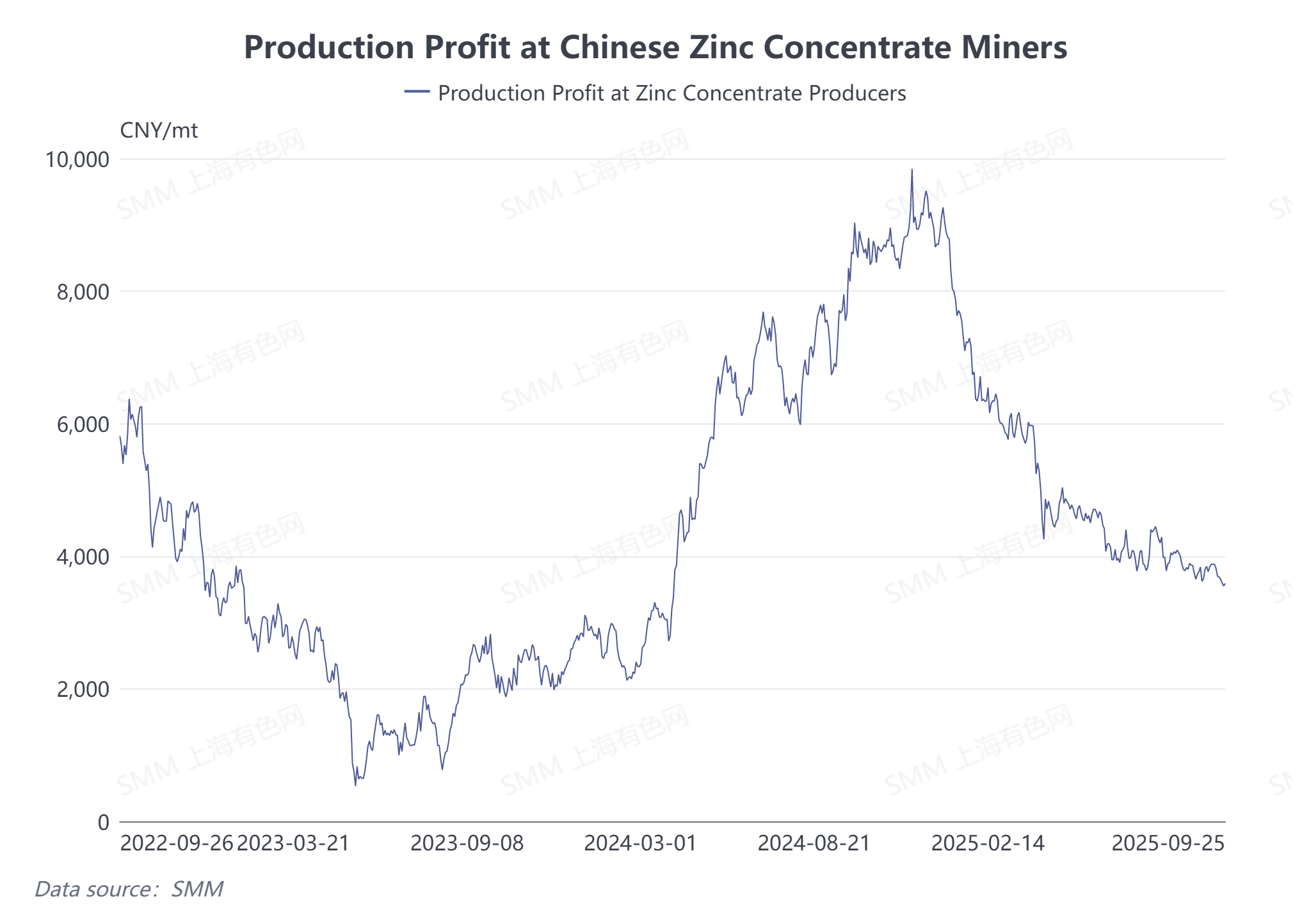

From the mine perspective, domestic zinc prices have been pulling back since the beginning of the year, while TCs have been climbing steadily, significantly compressing the production profits of Chinese zinc miners. Profits have decreased by approximately 5,500 yuan/mt since the start of the year. With zinc prices recently falling again to below 22,000 yuan/mt, miners, considering their profitability, have a strong inclination to lower zinc concentrate TCs in October.

In summary, the interplay of reduced zinc concentrate supply and winter stockpiling expectations, coupled with the buying fervor for domestic concentrate driven by the SHFE/LME price spread, led to a significant reduction in domestic zinc concentrate TCs in October. With the pattern of weak supply and strong demand persisting, domestic zinc concentrate TCs are expected to continue declining in Q4.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)