At the SMM Indonesia Seminar: Li-ion Battery & Energy Storage hosted by SMM, Lesley Yang, Senior Battery Materials Analyst at SMM, delivered an in-depth analysis of the development prospects of ternary cathode precursor materials and LFP cathode materials in Indonesia.

Downstream Demand: Current Status and Forecast

Global NEV Market Review and Outlook

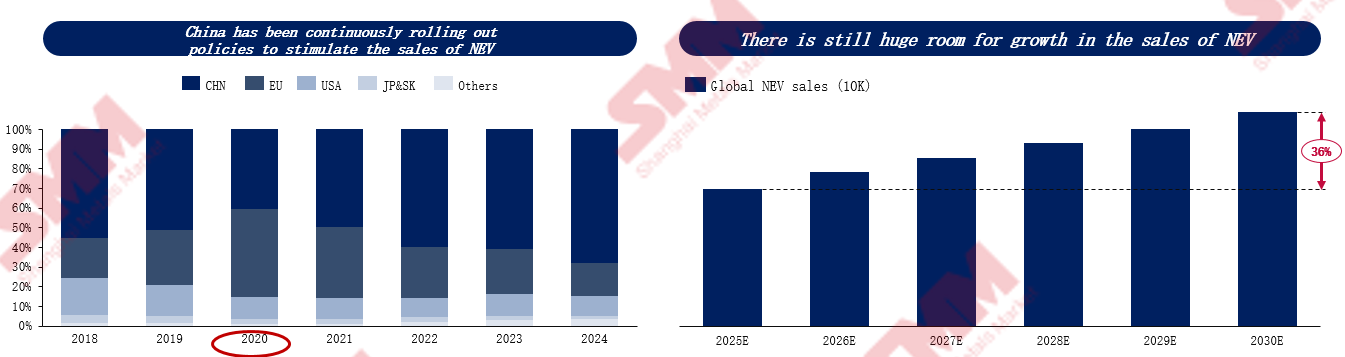

The NEV market has experienced explosive growth over the past six years, with global sales surging from approximately 2 million units in 2018 to nearly 17 million units in 2024, an increase of more than sevenfold. This growth has been primarily policy-driven: Europe has set emission reduction targets for 2030 and plans to ban the sale of internal combustion engine vehicles by 2035, accelerating automakers' transition; China, relying on its "dual-carbon" goals, has effectively boosted market demand through the "dual-credit" policy, purchase tax reduction and exemption, and replacement subsidies. This period can be regarded as a typical "policy-driven expansion phase."

Currently, the NEV penetration rate in China has exceeded 50%. As subsidies gradually phase out, market competition is shifting toward product strength, brand, and innovation. In emerging markets such as India, Southeast Asia, and Latin America, where penetration rates remain below 10%, subsidies and government incentives are still the main drivers. Global NEV sales are expected to exceed 31 million units by 2030, though the growth rate will gradually slow down. In terms of product structure, BEV models will continue to dominate the market, but plug-in hybrid models are performing well in the short term in China and Europe. In emerging markets, affordable small EVs priced below $15,000 are expected to be key to widespread adoption.

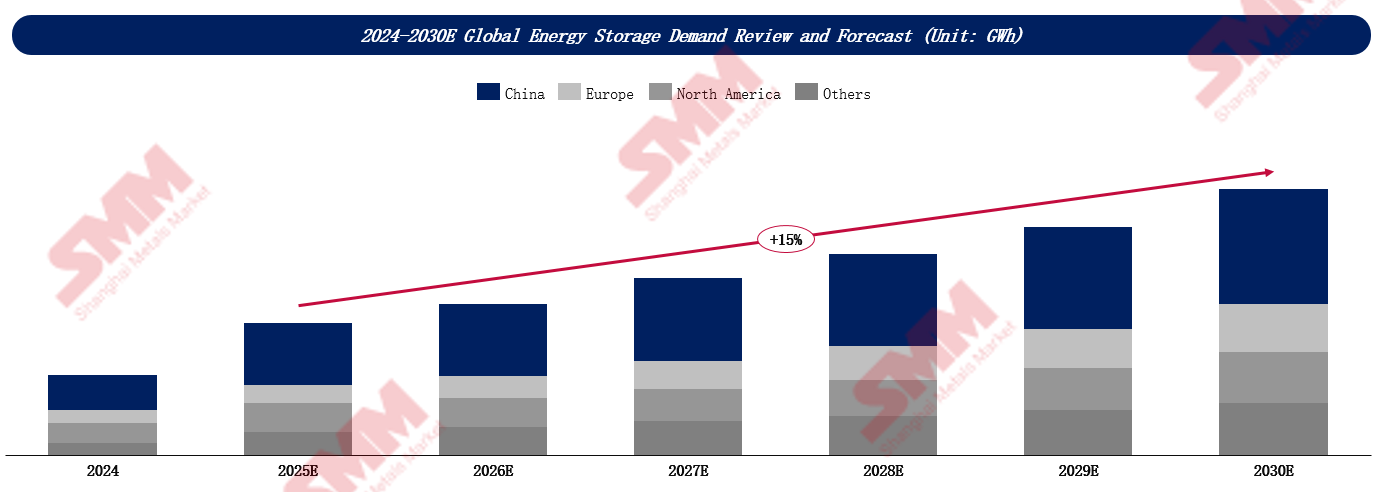

The ESS market is also experiencing rapid growth. SMM expects global ESS demand to grow from 312 GWh in 2024 to over 1,000 GWh by 2030. China remains the largest growth engine, accounting for over 40% of the market share. As power market reforms advance, energy storage systems can achieve profitability through auxiliary services and the spot market, coupled with the increasing proportion of renewable energy and continuously declining costs. The economics of ESS projects have significantly improved, gradually reducing reliance on policy support. The growth of the US ESS market mainly relies on fiscal incentives, with tax credit policies extended to 2034, providing long-term certainty for PV plus ESS and standalone ESS projects. However, its development still faces challenges such as grid connection bottlenecks and inconsistent policies across states. Europe, on the other hand, is driven by regulatory policies, with the EU Renewable Energy Directive requiring a 42.5% share of renewable energy by 2030, where ESS plays a crucial role in ensuring grid stability and energy security.

Global Cathode Material Capacity and Competitive Landscape

LFP batteries, due to their cost advantages, are widely used in NEVs and the ESS sector; ternary batteries, however, target the mid-to-high-end market to meet high energy density demands.

In terms of cathode material energy density, ternary materials increase with higher nickel content, with 3-series at about 155 mAh/g and 9-series exceeding 210 mAh/g, suitable for high-performance applications. LFP materials steadily improve energy density through compaction density iterations, with second-generation products reaching 155 mAh/g and fourth-generation expected to exceed 160 mAh/g. Although LFP materials have lower energy density compared to ternary cathode materials, they are widely adopted due to their cost, safety, and cycle life advantages.

China dominates the LFP material supply chain, with domestic LFP cathode material capacity expected to exceed 6.7 million mt by the end of this year. The market concentration of LFP cathode materials is declining, with the top five enterprises' market share dropping from 61% at the beginning of 2024 to 55% in 2025, making the speed of technological iteration a key factor for companies to capture the market.

Internationalization has become an important strategy for leading LFP producers. By 2028, overseas LFP material annual capacity is expected to reach 600,000 mt, with the global supply landscape becoming more diversified. Chinese enterprises lead this process, establishing production sites in the US, Spain, Poland, Malaysia, and Indonesia, while Japanese and South Korean companies also join the competition. This year, Lopal and Lithium Source will achieve 120,000 mt of capacity in Indonesia, marking that although the current LFP market is dominated by China, the future landscape will also depend on global cooperation and overseas manufacturing layouts.

For ternary cathode precursors, in 2025, China will still account for nearly 80% of global capacity, followed by Japan, South Korea, and Indonesia. Especially in Indonesia, with continuous investment from Chinese enterprises, capacity is expected to grow significantly. Despite the slowdown in the NEV industry and domestic overcapacity, Chinese producers are accelerating their overseas expansion, with Southeast Asia and Europe becoming the key regions for new capacity. From 2024 to 2030, the global ternary cathode precursor capacity is expected to have a CAGR of 0.7%.

In 2025, China's share of global ternary cathode material capacity will be 65%, followed by South Korea, Europe, and Japan. Europe, with its geographical advantages, local battery capacity, and trade policies, becomes the preferred destination for Chinese enterprises' overseas expansion. By 2030, overseas ternary cathode annual capacity will increase from the current 980,000 mt to 1.28 million mt, while China's new capacity will be less than 100,000 mt. From 2024 to 2030, the global ternary cathode material capacity is expected to have a CAGR of 3.6%.

In ternary cathode materials, mid-nickel and high-nickel ternary materials are the trend. By 2030, the market share of 8-series and 9-series ternary materials is expected to exceed 50%, with 6-series accounting for about 30%. NCA remains a niche, with a 9% market share expected by 2030. Currently, the Chinese market is dominated by 6-series and 8-series, accounting for more than two-thirds of demand; the overseas market, however, is highly inclined towards 8-series (over 55%), with NCA still holding about 20% of the market share.

Strategic Position of Battery Materials in Indonesia

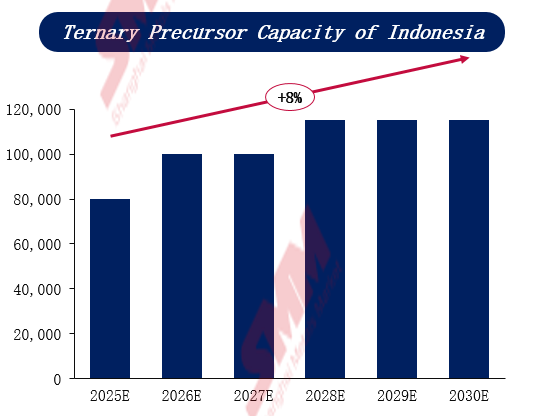

Indonesia not only boasts the world's richest nickel resources, with annual production exceeding 1 million mt, primarily laterite nickel ore, a key raw material for producing ternary cathode precursors, but it is also transforming from a resource supplier into a strategic hub for the global battery and NEV ecosystem. According to public data, CATL, BTR, Huayou Cobalt, Gotion High-tech, Lopal, BYD, and LG Energy Solution have all established a presence there.

According to SMM forecasts, by the end of 2025, Indonesia's annual ternary cathode precursor capacity is expected to reach 80,000 mt, and further increase to around 115,000 mt by 2028. Meanwhile, the capacity growth rate for LFP cathode material is even more significant, projected to surge from 120,000 mt in 2025 to 260,000 mt in 2030, with an average annual compound growth rate of 17%.

![[SMM Analysis] ITC Rejects Tariffs on Chinese Graphite Anodes, Final Duties Not Imposed](https://imgqn.smm.cn/usercenter/lzgUR20251217171731.jpg)