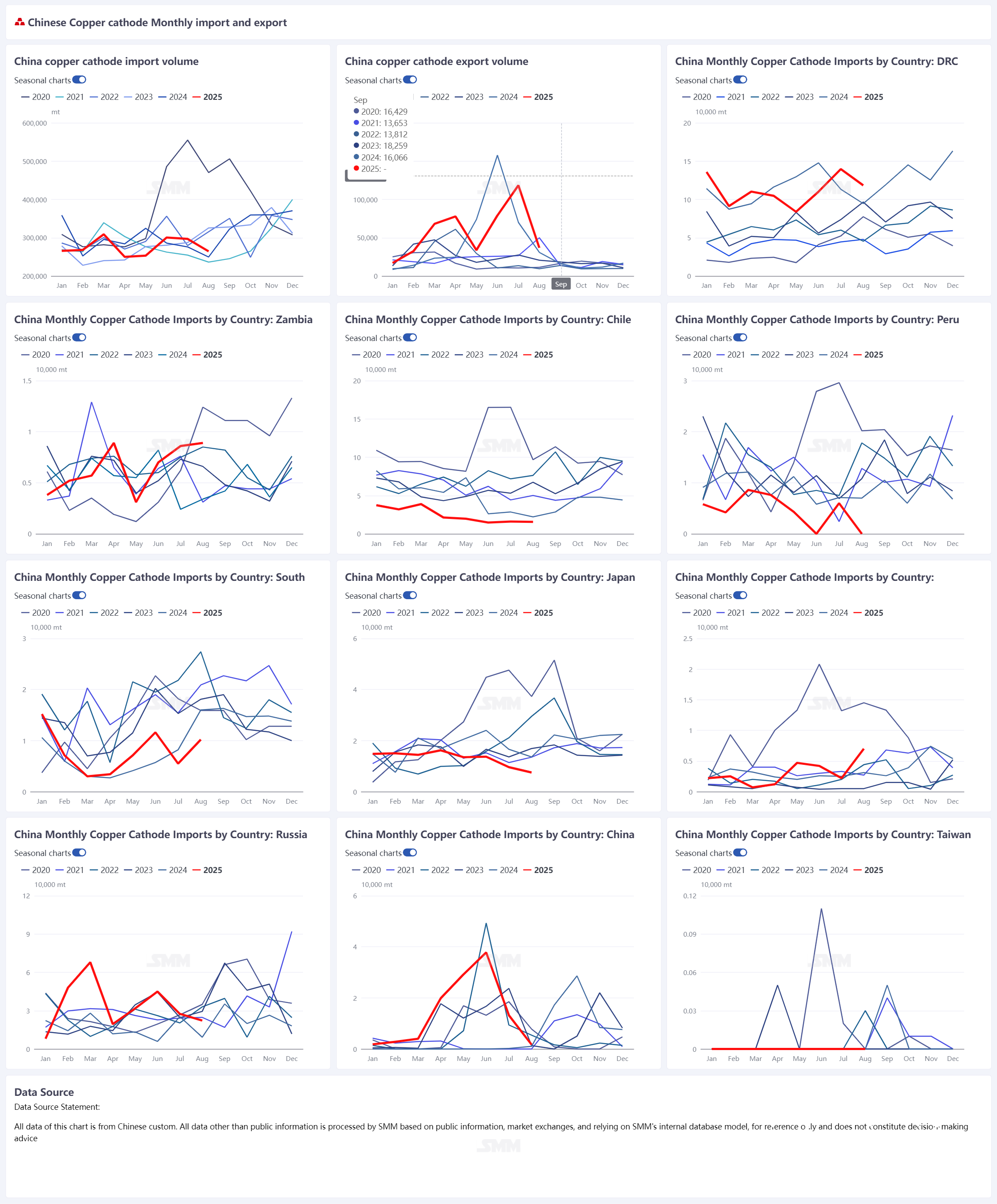

According to customs data, China's total refined-copper imports in August 2025 were 264,300 tonnes, down 10.99% MoM. but up 5.87%YoY. Exports were 36,800 tonnes, down 68.93% MoM and up 19.4% YoY.Overall imports came in below market expectations.

Imports — DRC down; overall arrivals miss expectations

By origin, imports from the DRC totaled 118,300 tonnes in August, accounting for 44.77% of the total and falling 15.22% MoM. The drop is notable. Local power instability and the seasonal peak in reefer season depressed DRC refined-copper output and sailings in July. However, SMM industry contacts report that overseas traders have not broadly felt a reduction in available volumes. Some vessels due at end-August may be delayed and could declear customs in September. Among other source countries, imports routed via the Netherlands mainly reflected Russian material held in Rotterdam warehouses, while overland-importing countries showed broadly stable volumes.

Exports — steep MoM fall; exports to the US effectively stop

China’s refined-copper exports fell sharply in August to 36,800 tonnes (MoM −68.93%, YoY +19.4%). Flows were concentrated to Taiwan and Southeast Asia. With PT Gresik’s maintenance in early August tightening long-term supplies to Southeast Asia, regional premiums rose, and some traders seized the window to export cargoes to the region to fill shortfalls. Singapore still accounted for some export volumes, but its share has noticeably declined. Overall, arbitrage exports to the US have effectively ended—only routine long-term deliveries and a small number of spot lots remain.

Outlook for September and beyond

Arrivals in September are expected to stabilise. As Indonesian output at Manyar increases, Indonesian refined-copper imports into China are likely to rise. Russian material in Rotterdam largely arrived in July–August, so related imports should ease in September. SMM notes that African supply may show reductions from October onward due to power and sulfuric-acid constraints; those impacts are expected to appear in October customs statistics. In sum, total monthly import volumes remain on the order of ~300,000 tonnes/month, with some of the near-term supply being filled from LME Asian warehouses.

![Early-Month Purchasing and Stockpiling Failed to Offset the Impact of Imports, SHFE Copper Spot Premiums Remained Under Pressure [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/OsOmo20251217171709.jpg)

![Market Activity Increased After the Contract Rollover, Spot Premiums Continued to Rise [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/fEiiq20251217171711.jpg)