【SMM Scrap Aluminium Market Analysis】 SMM Global Aluminium Scrap Markets Analysis (1) The EU's Scrap Aluminium Scare - Export Policies and Protectionism

The European Market on Scrap Metal

The European Union (EU) is one of the key exporters of scrap metals such as aluminium and copper globally. Amidst the ever-changing global political and economic market, the European market has been slowly inching towards a relatively careful approach towards their exports of scrap metal, which are key materials for the development of local industries, especially towards low carbon emission goals.

Ever since the American government’s 25% tariffs on steel and aluminium product imports in March, which were later raised to 50% in June and came with a new tariff on copper products in August, the European market has been acting defensively to prevent their already scarce recycled, raw materials from endlessly flowing into the American market. As the scrap metals were not included in the tariffs outlined in Section 232, they are included under the general tariffs of 15% for EU exports to the US. Under this circumstance, European Aluminium acted as one of the biggest voices of the EU aluminium industries, actively highlighting how the USA’s tariffs make it an unfairly favourable export destination. This might lead into, not only the EU, but the global flow of scrap metal being preferentially exported to the US, leading to a larger shortage of metal scrap when markets are already struggling to fulfill their domestic demand for scrap as a raw material, creating pressure for local businesses and industries to stay afloat.

Energy Costs and Lack of Supportive Policies: A Weakened European Industry

According to European Aluminium, energy costs in the EU have been rising out of hand since 2020, stemming from the COVID 19 Pandemic and the Russian invasion of Ukraine. In the years 2021 to 2022, Germany and France have has their average electricity costs rise tenfold, with other countries like the UK rising twofold. This is compounded with closures of nuclear reactors that were used for energy: studies showed that out of 56 reactors, EDF only has 24 of them operating as of August 2022 as a result of corrosion issues that come from the plant’s reactions. Due to the EU’s heavy reliance on fossil fuels for the production of energy, which was heavily disrupted by the Russian invasion and COVID-19, when compiled with a decrease in the availability of other energy sources such as nuclear, leads to upward pressure on the industry’s costs and the shrinking of industry profit margins.

Even though rising energy costs have threatened the stability of the European aluminium and metal markets, the EU have not pushed any policies to solve this issue since 2022; on the other hand, the EU has pushed out the EU Carbon Border Adjustment Mechanism (CBAM), a carbon import tax for 6 carbon intensive industries in the EU, which happens to include aluminium and iron/steel. Starting in 2023, the 6 industries are to report their emissions to the EU, and by 2026 the EU will make decisions whether or not to expand the scope of CBAM to other related products and downstream industries. Starting from 2026, the EU will the impose import duties that is burdened by both the importer and exporter on high carbon imported materials and products. Even though CBAM is still in its observational phase and the import duties have not been set in stone, it is already a widely discussed topic in the EU metals market, especially when it might add fuel to the fire in increasing costs for local aluminium and iron/steel industries within the EU’s borders when there has already been upward pressure from other influences such as energy.

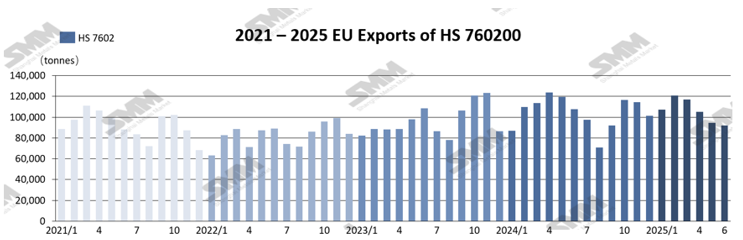

EU Exports of HS760400 Waste and Scrap of Aluminium, Q1-2 2025

SMM compiled data from various sources of the European Union’s exports of aluminium scrap, starting from 2021 and ending in the most recent sources in June 2025. According to the data, the EU has exported a total of 636,672 tonnes of HS760200 in January to June 2025, which is a 4% YoY decrease compared to the same period in 2024, which saw a total of 661,238 tonnes of aluminium scrap exports. Based on monthly data, the downward trend in export volumes in 2025 began earlier than in previous years, with a decline starting in March. However, the overall decrease was relatively moderate, and subsequent months largely followed the typical pattern of a gradual and stable decline seen in the same period of past years.

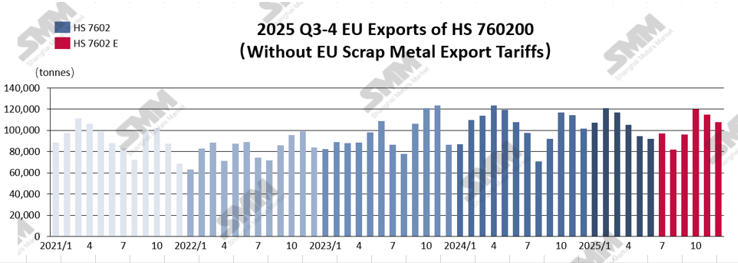

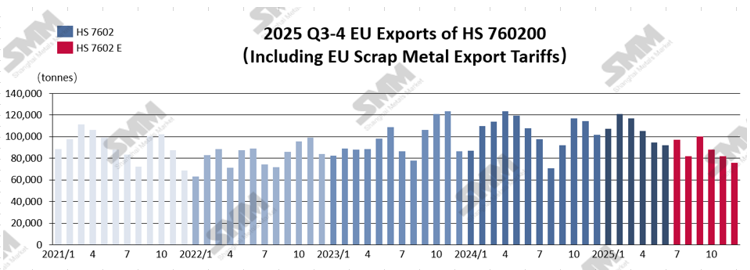

EU Exports of HS760400 Waste and Scrap of Aluminium, Q3-4 2025 Estimates

Among the speculations of possible policies the EU might enact at the end of the 3rd quarter, export tariffs on scrap metals are some of the most widely discussed methods to keep metal scraps flowing within the EU market. European Aluminium and EUROFER have recently in September come together to push the EU for a 30% export tariff on scrap metals, to prevent already scarce raw materials from being exported to foreign markets, which creates pressure on local EU industries. European Aluminium Director General Paul Voss has also spoke extensively about higher energy and labour costs in Europe, leading to a decrease in competitiveness of the market when compared to emerging and strong Asian markets like China and India, creating a need for action from the EU like export tariffs and restrictions to better protect the European market from unfair competition in other regions and markets.

Therefore, when forecasting export volumes for HS760200 in the second half of 2025, SMM divided the analysis into two scenarios: one assuming a 30% EU tariff and one without the tariff. This approach aimed to provide a more comprehensive assessment of the panic and challenges triggered by the potential tariff, and to better understand how the projections would differ under each scenario—thus highlighting SMM’s evaluation of the possible impact of a 30% EU tariff.

Without EU Scrap Metal Export Tariffs: Based on current market conditions, SMM analysis suggests that if the EU does not go through with proposed export tariffs for metal scraps in Q3 of 2025, export volumes of HS760200-coded waste aluminum are expected to increase in the second half of 2024. Specifically, due to anticipation of potential EU tariff measures, the market may experience a phase of stockpiling and advance procurement from the European market in August and September, partially offsetting the impact of falling prices in August. From September onward, as seasonal demand recovers, export volumes of waste aluminum are projected to rise to around 100,000 tonnes, reaching approximately 120,000 tonnes in October. Toward year-end, due to base effects from the same period in 2023–2024, export volumes in November and December are expected to decline moderately. SMM forecasts that total waste aluminum exports in 2025 will remain broadly in line with 2024 levels, with a slight increase possible, bringing the annual total to around 1.26 million tonnes.

With EU Scrap Metal Export Tariffs: If the EU introduces an export tariff policy on scrap metals by the end of Q3, it will directly suppress the export momentum of waste aluminum under HS code 760200. Following the same forecasting logic as the no-tariff scenario, SMM anticipates that uncertainty surrounding the potential policy may trigger short-term market volatility in August and September, prompting EU exporters to release inventory in advance. This could lead to a temporary spike in waste aluminum export volumes during those two months. Should the tariff be officially implemented in October, export volumes are expected to decline significantly from that point onward and continue trending downward through December. Based on scenario modeling, SMM projects that total EU waste aluminum exports in 2025 will decline by approximately 5%–10% year-on-year compared to 2024, with the absolute volume potentially falling to around 1.16 million tonnes.

Interpretation of EU’s Conservative Sentiment

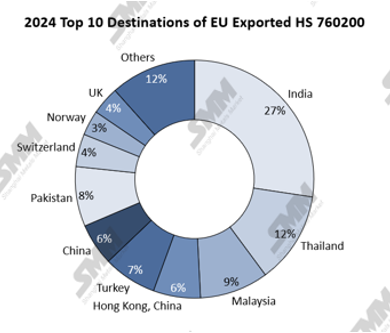

According to 2024 data on EU waste aluminum exports under HS code 760200, the United States did not even rank among the EU’s top ten export destinations. Specifically, of the EU’s total 1.26 million tonnes of waste aluminum exports in 2024, only 9,400 tonnes were shipped to the U.S., accounting for just 0.75%.

Based on the EU’s latest cumulative data for 2025, although U.S. imports of EU waste aluminum showed a notable increase between March and May, the actual transaction volume remains insufficient to support the claims that U.S. tariffs are driving EU waste aluminum flows toward the United States. Notably, if export tariffs were implemented at this time, they could significantly suppress imports of EU waste aluminum by major Asian economies from the EU market, particularly India, Pakistan, Turkey, and China. Data shows that these four countries have maintained steady growth in imports of EU waste aluminum from 2023 through 2025.

Conclusion

Given Asia’s high dependence on EU waste aluminum, the EU market will be a critical area to monitor in global waste aluminum trade throughout 2025. SMM will continue to track developments in the EU market, especially regarding whether export tariffs are introduced by the end of Q3 and how the market evolves thereafter. In addition, SMM will closely monitor the implementation of the EU’s Carbon Border Adjustment Mechanism (CBAM) in early 2026 and continue to follow policy trends and market changes in the region.