SMM September 15 News:

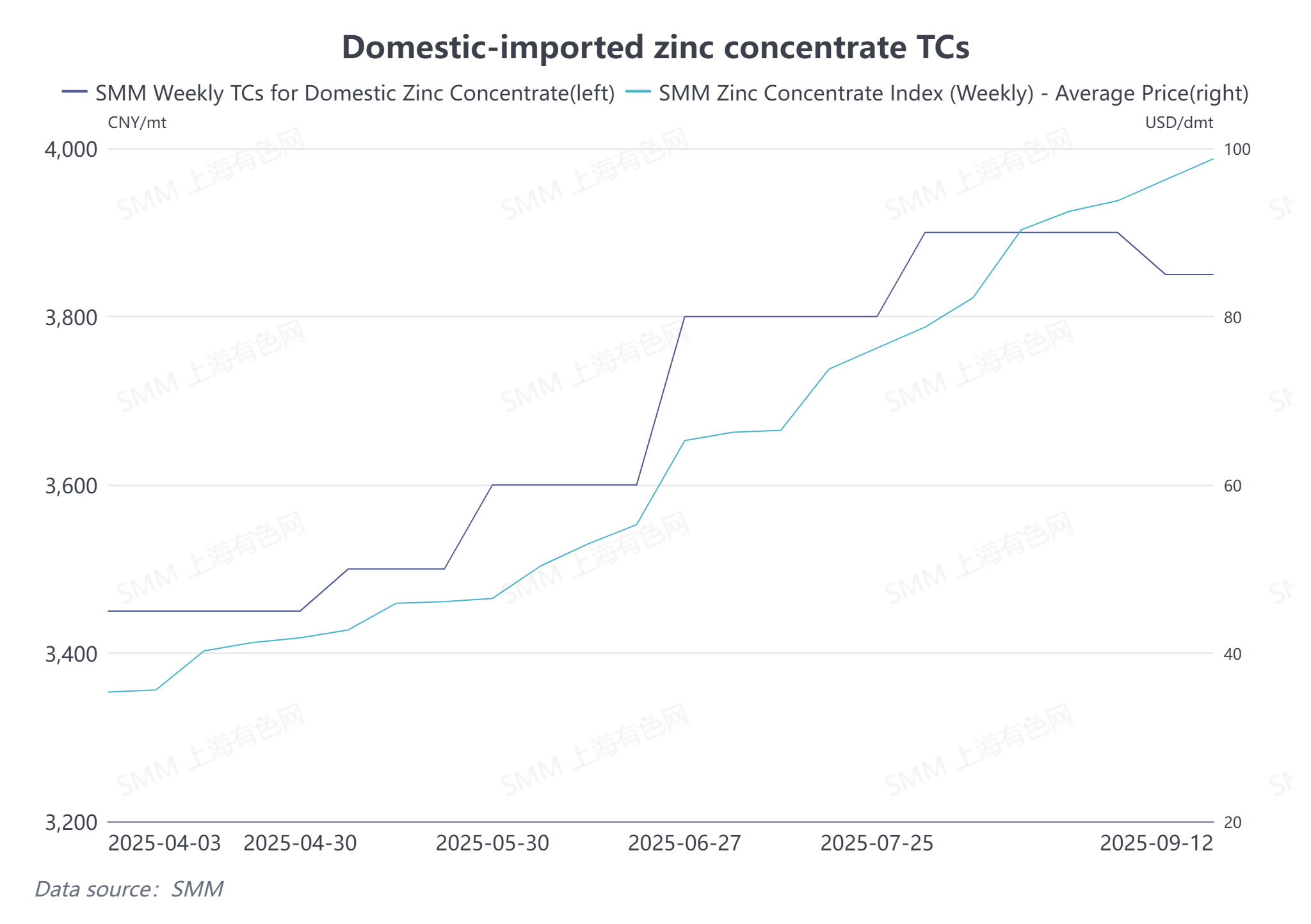

According to SMM data, as of September 12, the weekly average SMM Zn50 TC stood at 3,850 yuan/mt in metal content, down 50 yuan/mt in metal content from August, while the imported zinc concentrate index reached $98.75/dmt. This marks the end of the 10-month upward trend in domestic zinc concentrate TCs, whereas imported zinc concentrate TCs continued to climb. Why did domestic zinc concentrate TCs suddenly reverse course in September? What are the expectations for Q4?

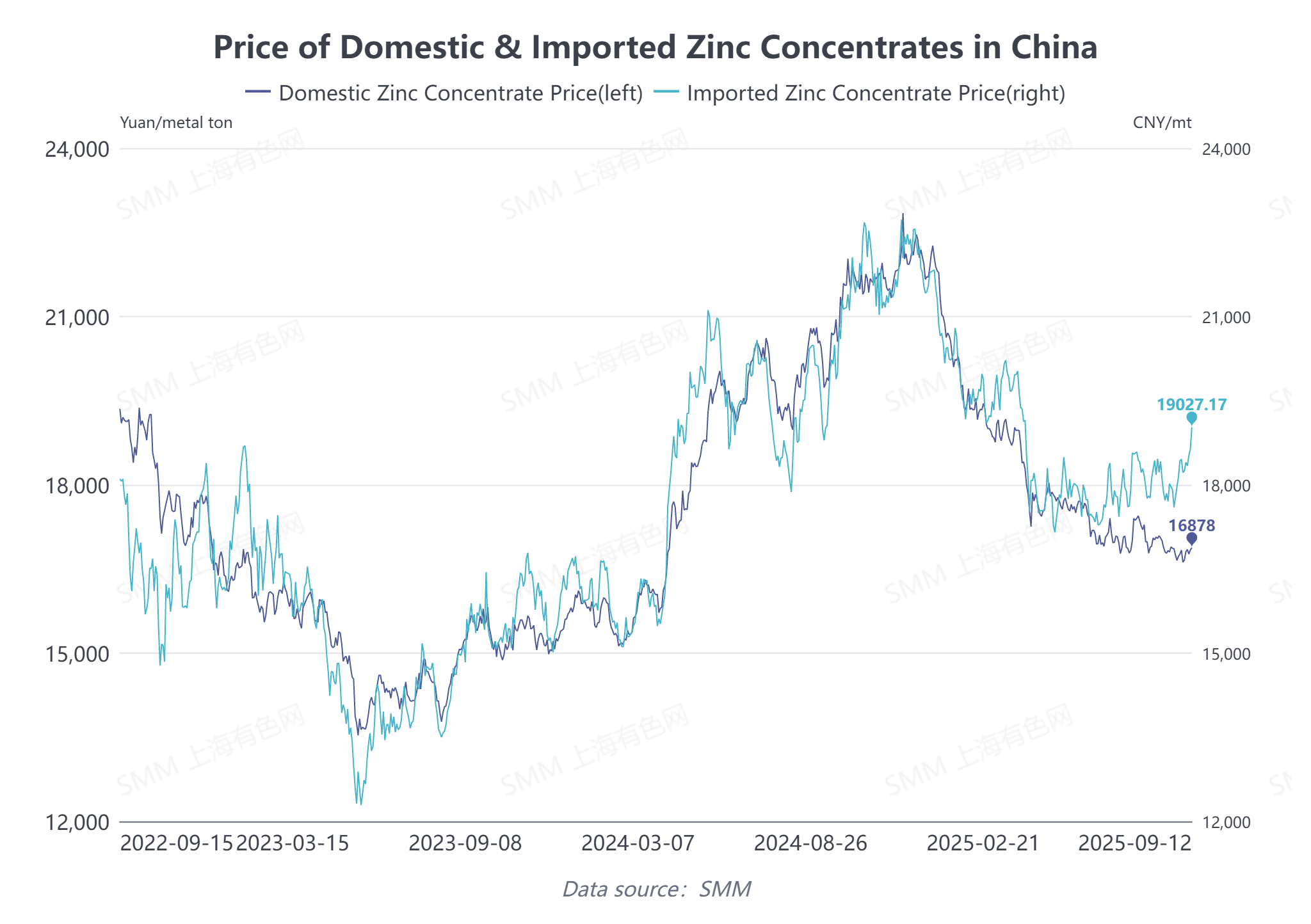

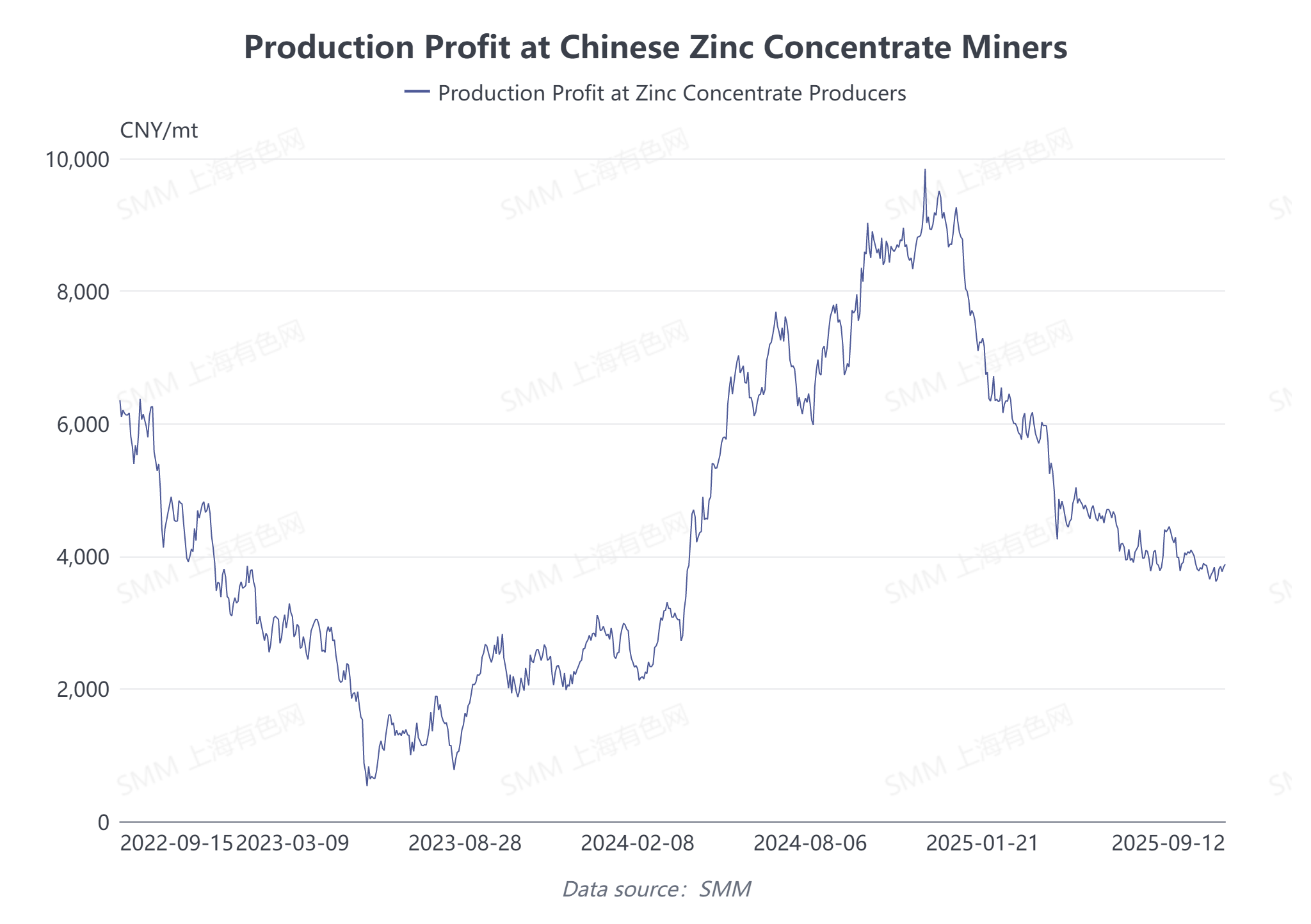

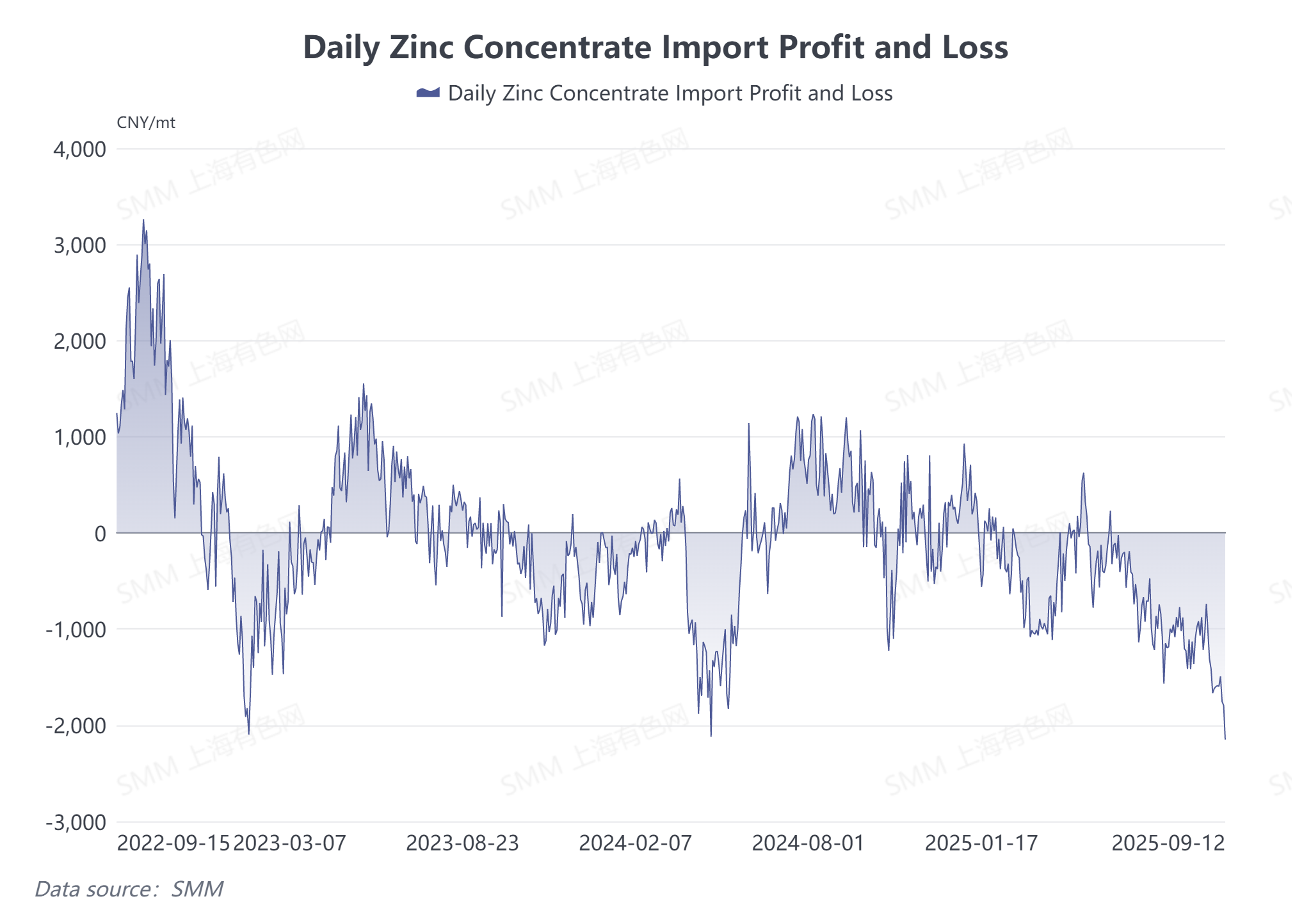

Entering September, based on current domestic and international zinc prices and TC calculations, the price spread between imported and domestic zinc concentrate has widened to over 2,000 yuan/mt in metal content. Driven by this price advantage, domestic smelters are actively competing for domestic zinc concentrate. However, according to SMM, as domestic zinc prices continue to decline, production profits for Chinese zinc mines have been further compressed, dropping by approximately 5,000 yuan/mt from the beginning of the year to date. Miners have low willingness to further increase TCs for September. Additionally, domestic smelters currently enjoy production profits exceeding 1,000 yuan/mt, including by-products. Strong profitability has incentivized smelters to maintain high production enthusiasm and robust demand for raw materials. Under the influence of these combined factors, domestic zinc concentrate TCs struggled to rise in September, with some regions already experiencing adjustments downward, leading to a divergence in trends between domestic and imported zinc concentrate TCs.

Outlook for Q4

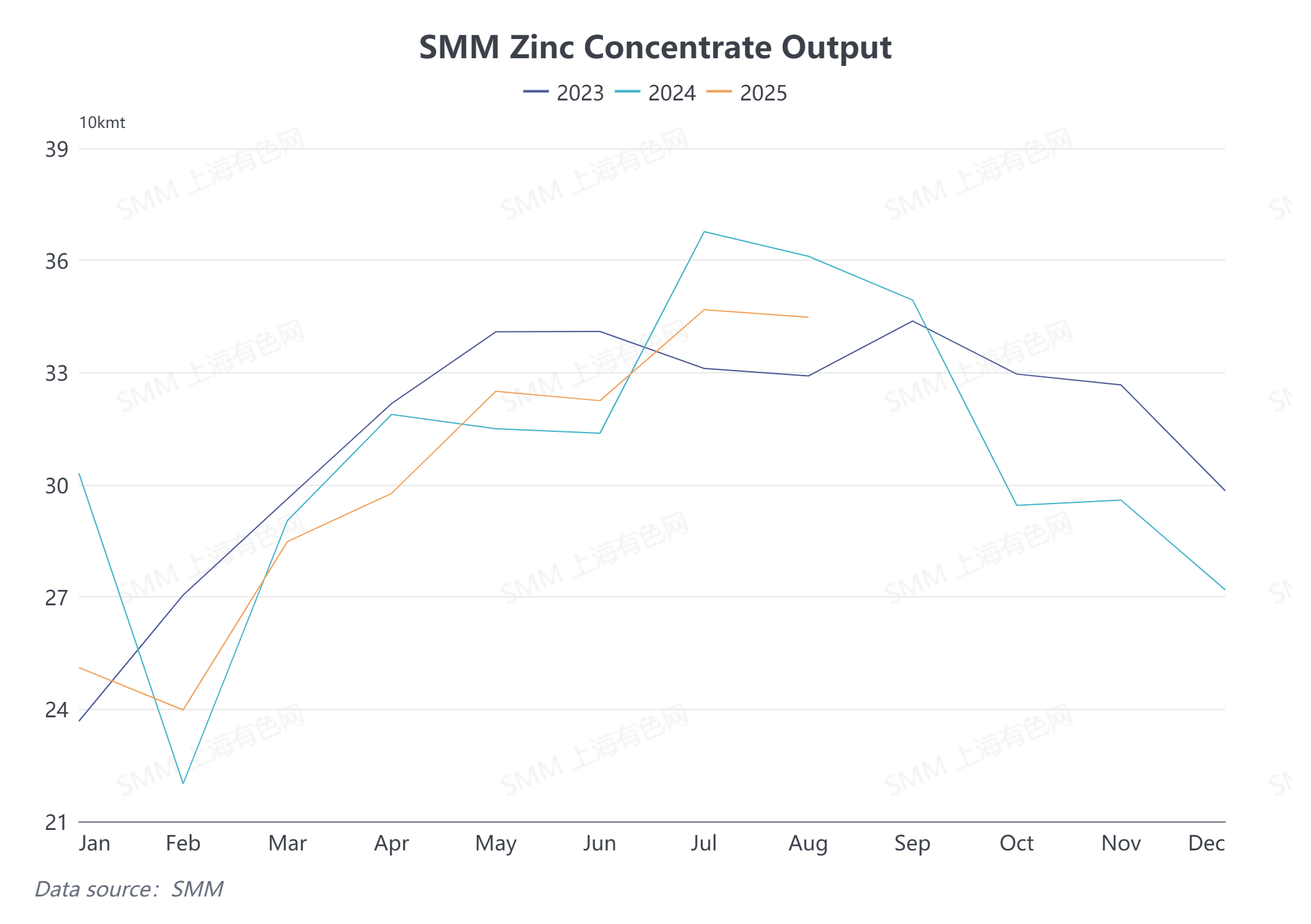

Regarding domestic TCs: Q4 is typically the season for routine mine suspension in China. Historically, some mines in northern China begin to reduce or halt production starting in November. Domestic zinc concentrate production is expected to decline QoQ in Q4, potentially weakening the supply of domestic zinc concentrate. Simultaneously, Q4 coincides with the winter stockpiling period for domestic smelters. Coupled with their active production, the average monthly production of refined zinc in China during Q4 is likely to exceed 600,000 mt, sustaining robust demand for zinc concentrate raw materials. Against the backdrop of weak supply and strong demand, domestic zinc concentrate TCs are expected to continue decreasing in Q4.

In contrast, for imports: According to SMM, LME zinc ingot inventory has recently destocked to around 50,000 mt. The SHFE/LME price ratio continued to deteriorate in September, and the loss on importing zinc concentrate into China has now widened to over 2,000 yuan/mt, indicating persistently poor economics for imported zinc concentrate. Without improvement in the price ratio, traders may continue to raise their TC offers to facilitate transactions for imported zinc concentrate. Therefore, there remains some upside potential for imported zinc concentrate TCs in Q4.

In summary, Chinese smelters primarily sourced domestic zinc concentrate in September, leading to a downward adjustment in domestic zinc concentrate TCs and a divergence in trends between domestic and imported materials. Looking ahead to Q4, with the arrival of the winter stockpiling period, domestic zinc concentrate TCs may continue to decline, while imported zinc concentrate TCs still have room for increase. SMM will continue to monitor the subsequent trends in TCs.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)