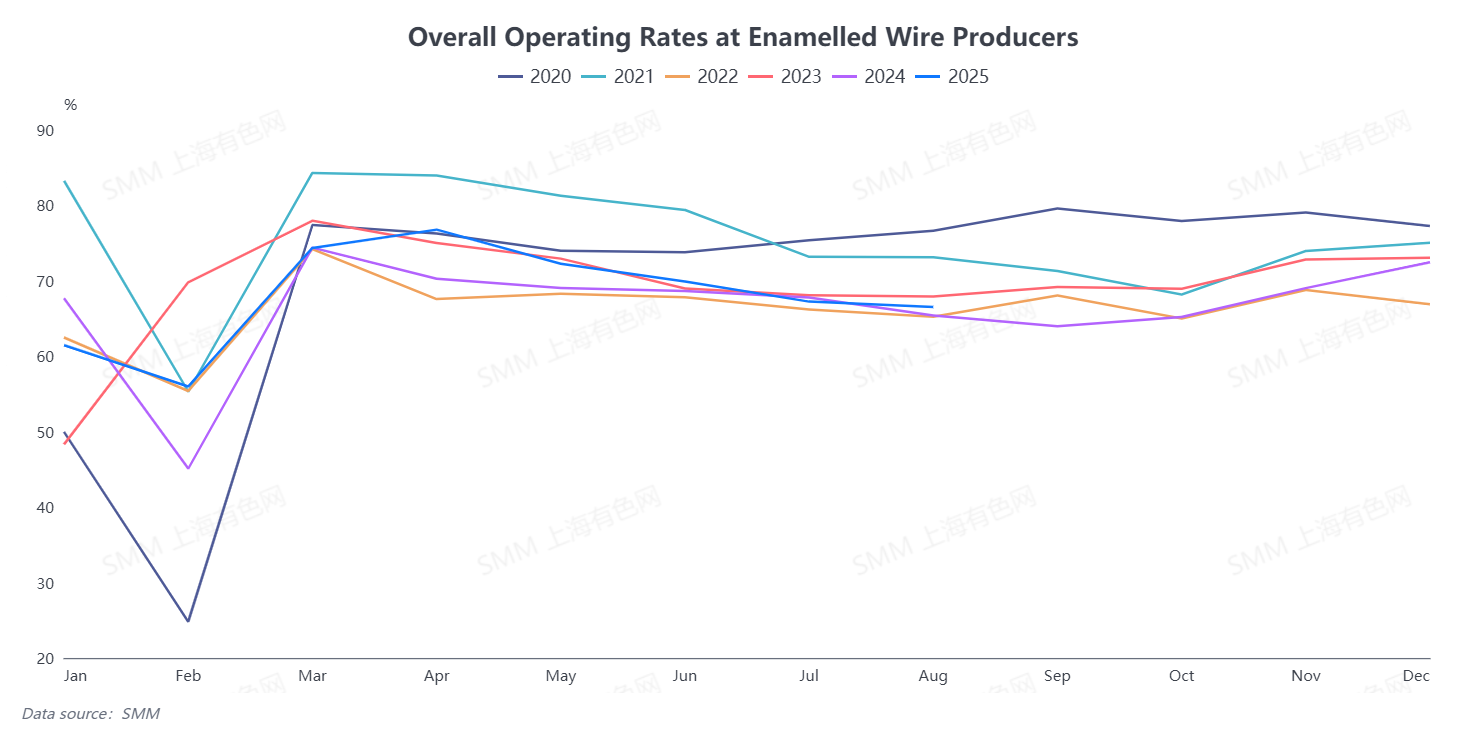

According to SMM, the comprehensive operating rate of the enamelled wire industry in August was 66.55%, down 0.7 percentage points MoM and 1.13 percentage points YoY. By enterprise size, the operating rates were 64.39% for large enterprises, 70.89% for medium-sized enterprises, and 68.94% for small enterprises.

In August, the operating rate of the enamelled wire industry declined as expected, aligning with market projections. The month remained a traditional off-season for the sector, with insufficient downstream orders being the primary constraint on enamelled wire demand and the key factor behind the subdued operating rate. Notably, round enamelled wire was more significantly impacted by the off-season effect, as persistently weak demand in the home appliance market and sluggish order performance became the main drag on the overall operating rate. Meanwhile, rising copper prices further suppressed demand, compounded by a slowdown in demand growth from the two-wheeler segment due to policy disruptions from new national standards in late August. These multiple pressures collectively exacerbated the industry's low operating rate. From a demand structure perspective, round and flat enamelled wires exhibited divergent trends: flat enamelled wire maintained steady demand supported by stable orders from the new energy and transformer sectors, while round enamelled wire remained under pressure due to weak home appliance demand. This divergence further highlighted the structural characteristics of industry demand in August.

On the inventory front, enamelled wire manufacturers continue to face sales-side pressure, with month-end finished product inventories remaining elevated. Data shows that the finished product inventory/output ratio for enamelled wire producers stood at 39.1% in August, up 0.31 percentage points MoM, reflecting a slight increase in industry inventory pressure.

SMM expects the comprehensive operating rate of the enamelled wire industry to rebound to 68.78% in September, up 2.23 percentage points MoM and 4.81 percentage points YoY, offering some positive expectations for the sector. However, given the current market environment, concerns persist regarding September’s outlook: on one hand, persistently high copper prices and the absence of clear recovery signals from the home appliance sector—a major downstream market for enamelled wire—raise uncertainties about the strength of the overall rebound. On the other hand, some firms note that the upcoming National Day holiday at the end of September may influence downstream stockpiling sentiment depending on copper price movements, making September’s copper price trends and downstream purchase willingness key factors to monitor.

![The Most-Traded BC Copper Contract Closed Down 1.47%, a Stronger US Dollar Index Put Copper Prices Under Pressure [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/Fxolk20251217171712.jpg)