In August, the sodium-ion battery industry exhibited varying development trends across different segments of the industry chain. While some areas experienced production fluctuations, the market landscape continued to evolve, with companies actively preparing for H2 growth.

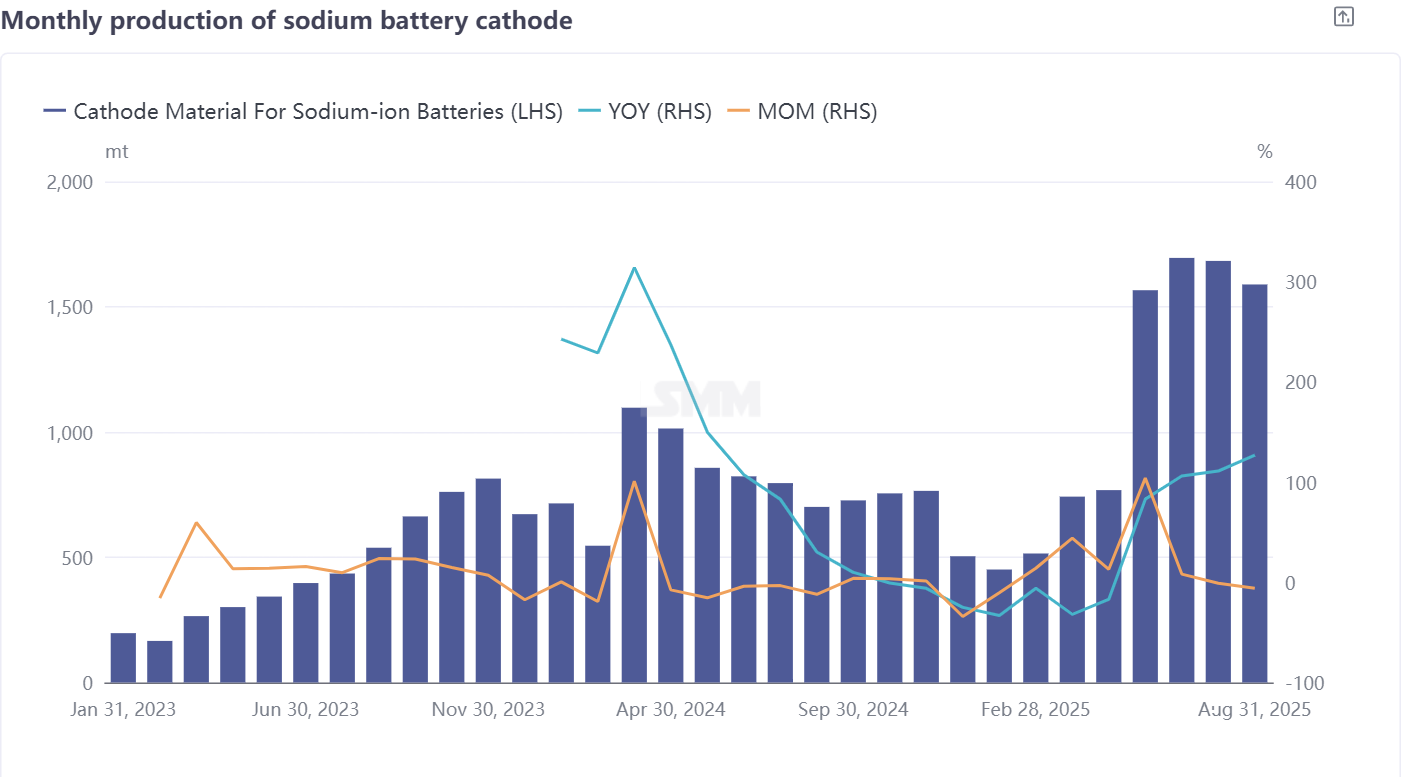

**Cathode Materials: Slight Production Decline, NFPP Dominance Remains Firm**

Sodium-ion battery cathode material production dipped 6% MoM in August but still surged 127% YoY, maintaining the overall growth momentum. In terms of product structure, polyanionic NFPP retained its dominant position with a 67% production share, though it edged down 2 percentage points MoM, while further penetrating the traditional layered oxide cathode market. In applications such as ESS and two-wheelers, NFPP's competitive advantages continued to squeeze the market space of layered oxide O3, leading to a notable YoY decline in O3 shipments.

Affected by weak demand, layered oxide cathode producers faced operational challenges. Some shifted their focus, while others maintained low-frequency production to meet minimal downstream orders. Compounding the difficulties, rising raw material prices (e.g., nickel sulphate) increased production costs for layered oxides, which already lacked price competitiveness against polyanionic materials. Some producers even resorted to loss-making sales to retain orders through price competition. Additionally, the market space for layered oxide P2 continued to shrink, potentially surviving only in niche scenarios. The NFPP production fluctuation was viewed as normal, likely due to downstream production plan adjustments. With intensive preparations for sodium-ion ESS projects in H2, NFPP demand is expected to see significant growth. Overall, September cathode production is projected to rise 10% MoM and 139% YoY.

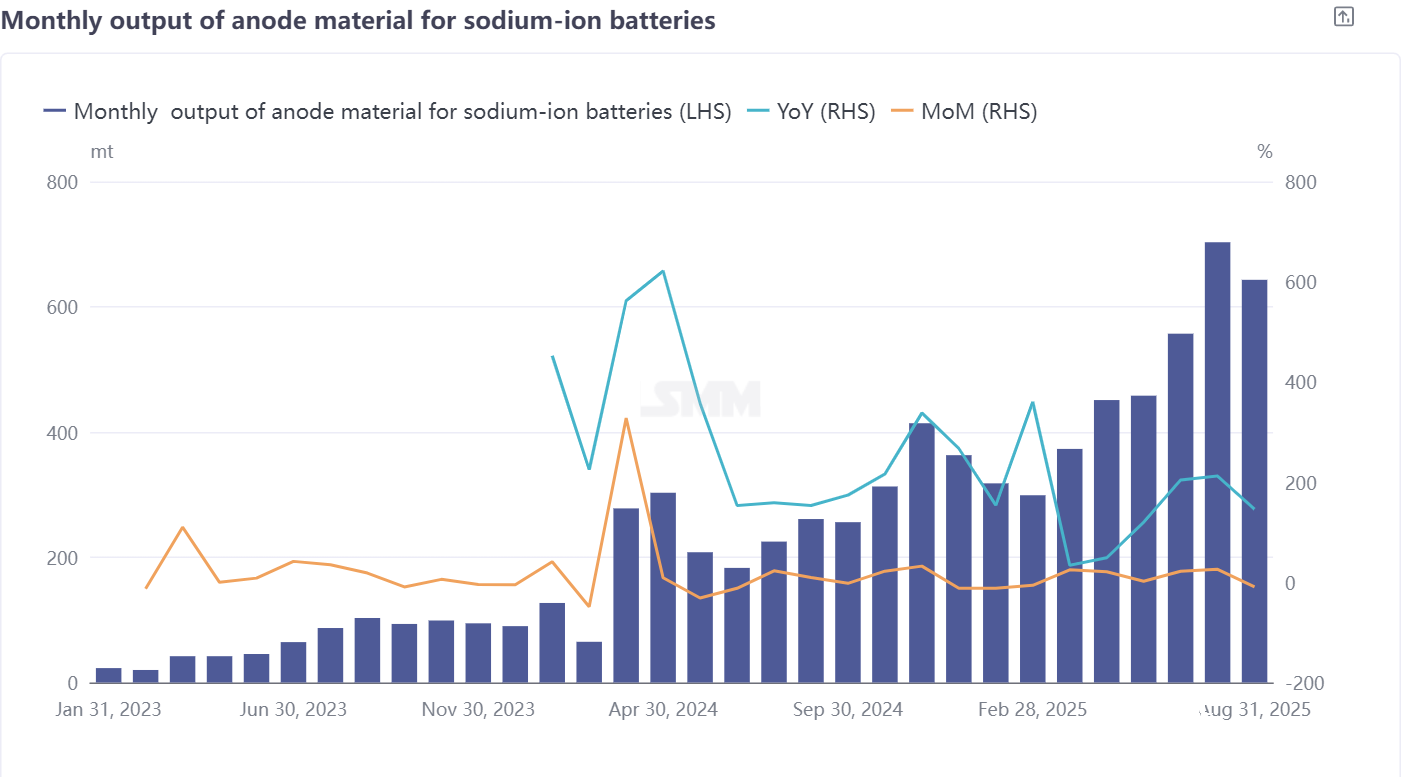

**Hard Carbon Anode Materials: Premium Capacity Shortage Spurs Alternative Solutions**

Sodium-ion battery hard carbon anode production fell 9% MoM in August but jumped 146% YoY. The sector currently faces multiple challenges: intermittent orders hinder stable production, while cathode output growth outpaces hard carbon anode capacity expansion, partially constraining battery cell production progress. On the raw material side, imported coconut shell carbon prices from overseas continued to fluctuate at highs, with import prices surging in recent months, imposing significant cost pressure on domestic hard carbon enterprises. As China has yet to develop mature hard carbon production technologies and mass production lines comparable to coconut shell carbon, companies have begun exploring alternative biomass resources and moving toward cost reduction. Looking ahead to September, as enterprises gradually address capacity and raw material challenges, hard carbon anode material production is expected to increase 13% MoM and 183% YoY.

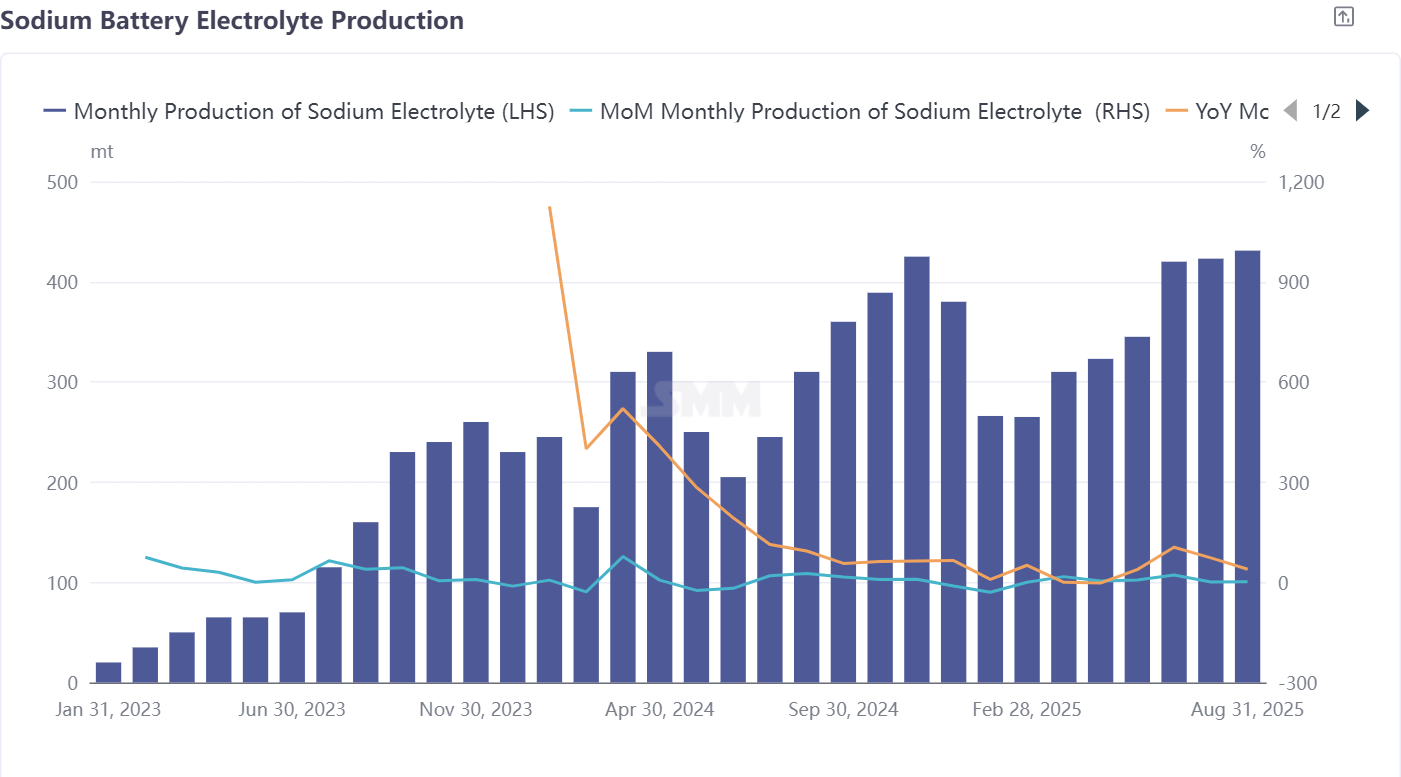

Electrolyte: Leveraging idle lithium battery capacity for production, mass production progress awaits acceleration

Sodium-ion battery electrolyte production rose 2% MoM and 39% YoY in August. Currently, the vast majority of sodium-ion battery electrolytes are produced by lithium battery electrolyte manufacturers utilizing idle capacity. Although overall capacity is sufficient, orders exhibit significant monthly fluctuations due to downstream demand.

With the expansion of sodium-ion battery electrolyte mass production, key raw material prices such as electrolytes and additives are expected to decline further, reducing production costs. Meanwhile, increased production by downstream battery cell manufacturers will also positively contribute to stable electrolyte production. Sodium-ion battery electrolyte output is projected to grow 1% MoM and 21% YoY in September, as the industry steadily progresses toward stable mass production.

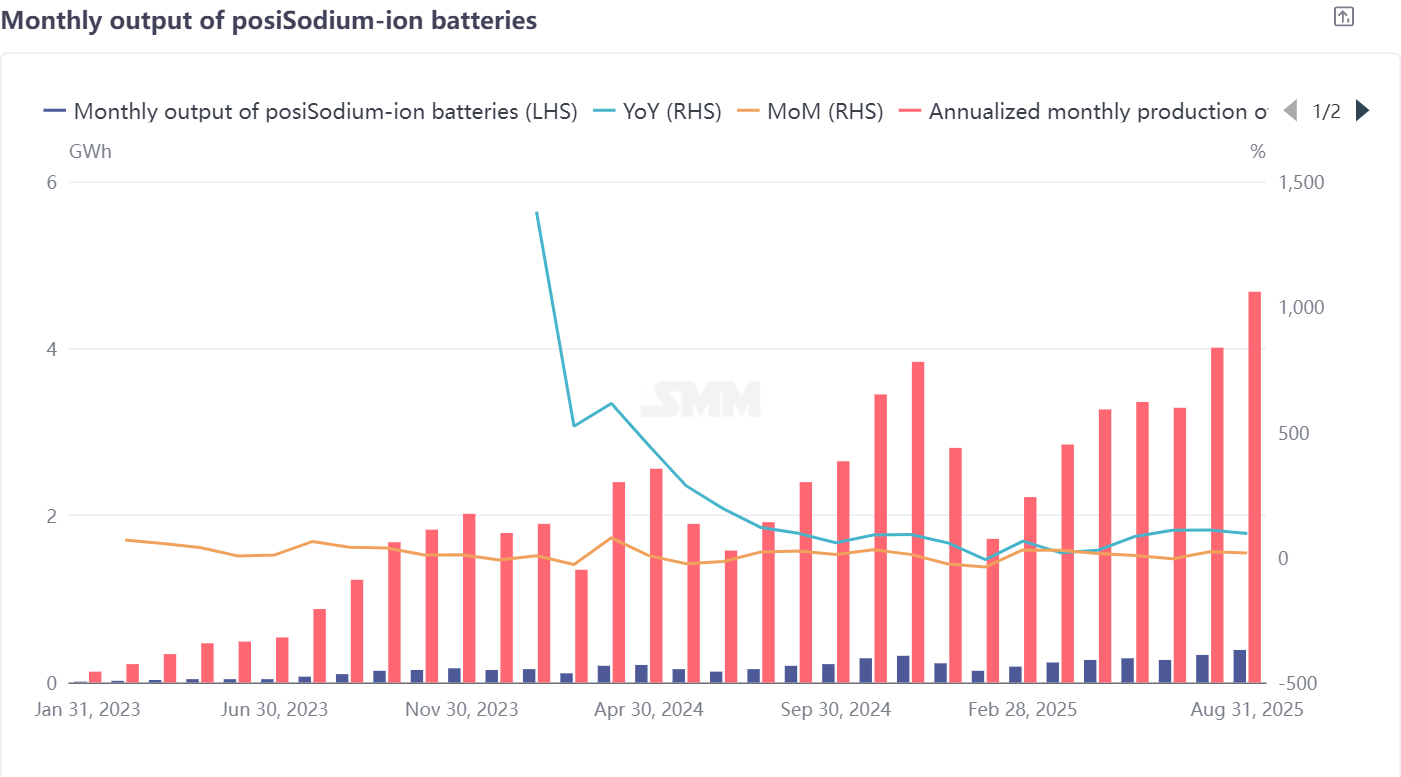

Battery Cells and End-Users: Actively expanding application scenarios, stabilizing shipments remains a core challenge

Sodium-ion battery cell production delivered strong performance in August, increasing 17% MoM and 95% YoY. Both traditional lead-acid and lithium battery enterprises actively expanding their sodium-ion product portfolios, as well as startup sodium-ion cell manufacturers, are fully committed to broadening downstream application scenarios to reduce unit costs through higher shipment volumes.

ESS project tenders for sodium-ion batteries are set to commence in H2, prompting battery cell manufacturers to begin preparations. Currently, industry competition focuses more on quality improvement and differentiated strategies, with optimistic shipment performance in niche segments. However, ensuring stable monthly shipments has become an urgent core challenge for sodium-ion cell enterprises. Production is forecast to rise 4% MoM and 83% YoY in September. Overall, the sodium-ion battery industry progressed amid fluctuations in August. While various segments of the industry chain faced distinct challenges, the gradual expansion of application scenarios such as ESS in H2 is expected to bring new development opportunities to the sector.

![[SMM Analysis] Ternary Cathode Payables May See Modest Increase in Q2](https://imgqn.smm.cn/usercenter/nVnLo20251217171728.jpg)

![[SMM Analysis] Weak Trading Sentiment but Strong Cost Support, Ternary Cathode Precursor Prices Edged Up](https://imgqn.smm.cn/usercenter/wZUBk20251217171729.jpg)