August 26, 2025 News:

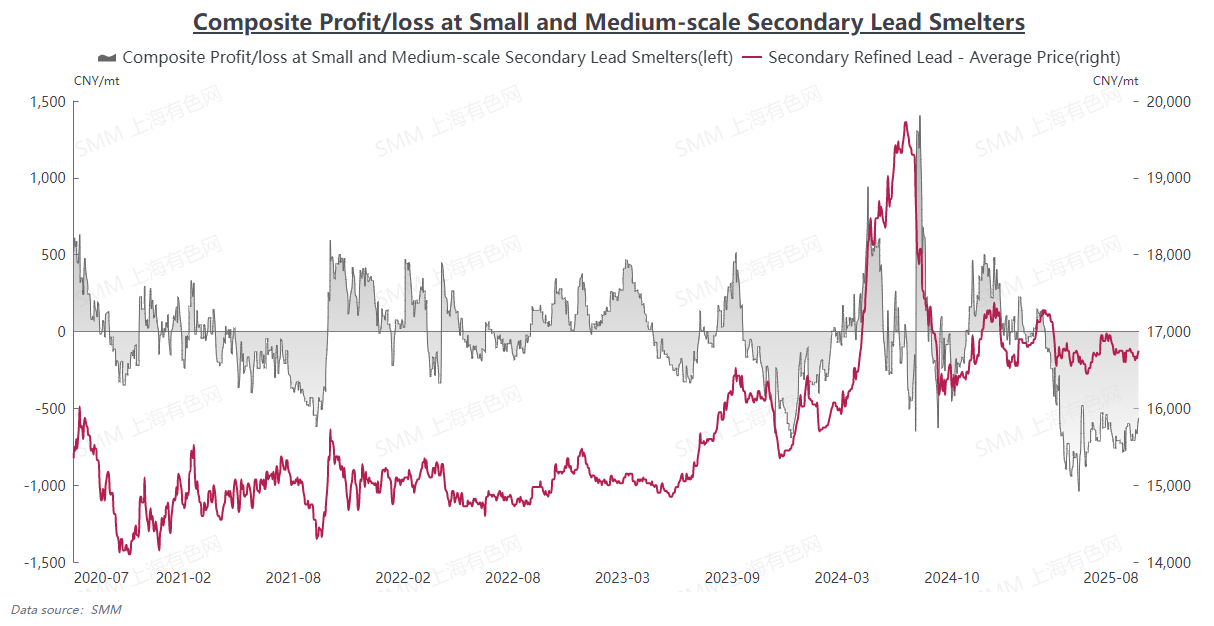

Since 2025, the losses in secondary refined lead smelting have been increasing, and the duration of these losses has been extending.

I. What are the root causes of the worsening losses in secondary lead smelting?

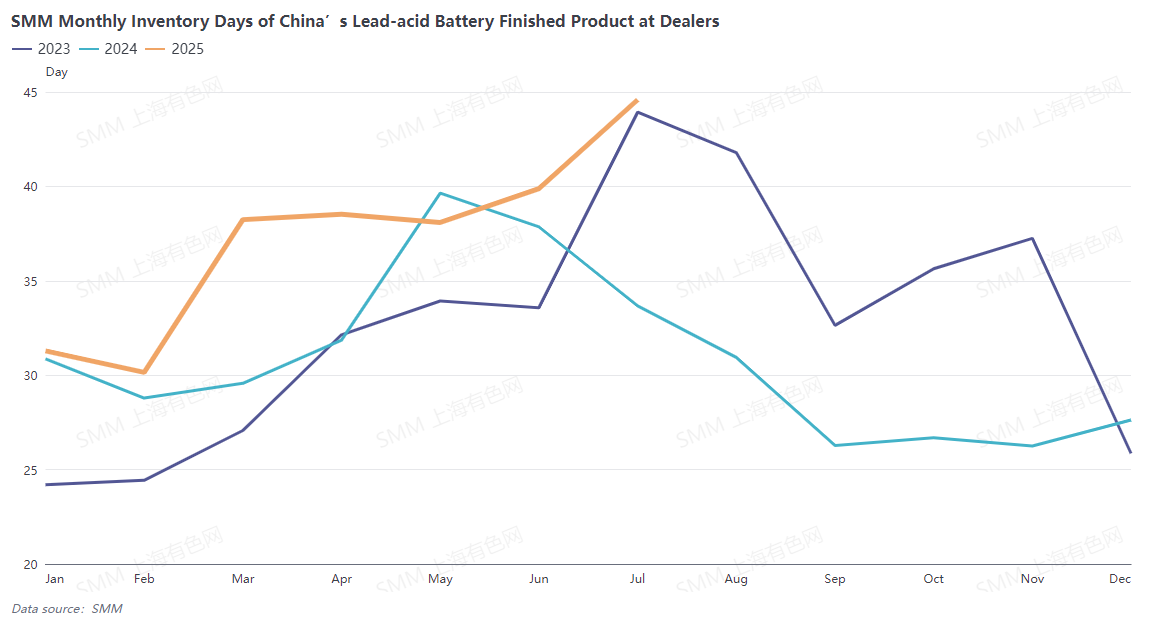

1. Fundamentally, overcapacity and high raw material costs due to tight supply are well-known issues. In addition, end-use consumption of lead has been declining year by year, and an "underperforming peak season" seems to have become the norm; especially with the Sino-US tariff events this year, export orders for Chinese lead-acid batteries have also performed poorly. Domestic lead-acid battery producers have high finished product inventories, and dealer inventories are similarly high. The market's absorption of batteries is far weaker than in previous years.

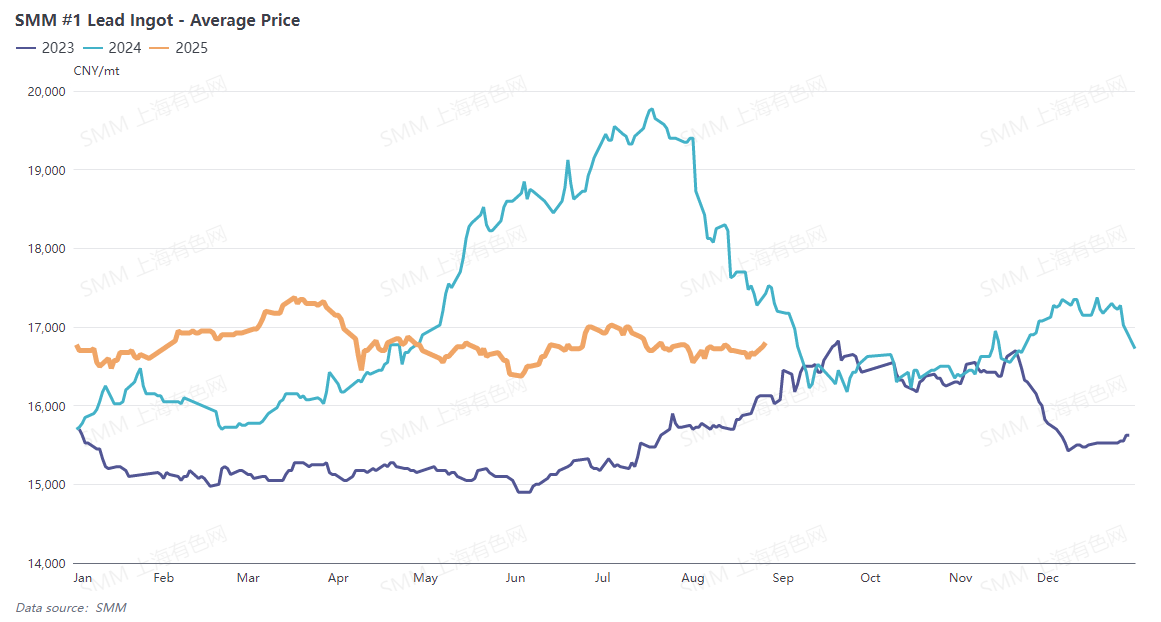

As a result, lead prices are weaker compared to last year. Under the circumstances of high raw material costs and stagnant refined lead prices, secondary refined lead smelters face significant loss pressures from both ends.

2. The withdrawal of local government preferential policies is akin to losing a "blood source" for most secondary lead smelters. When secondary lead smelting projects were initially established, they generally enjoyed the benefits of local investment attraction: tax incentives and financial subsidies varied by region. For example, a large smelter in north-west China mentioned that the local government provided five years of preferential policies, which expired after five years of operation. A medium-sized enterprise in east China mentioned that the local government's incentives were phased out gradually, with the tax rebate ratio decreasing by 25% annually until it reached zero. By 2024, some enterprises no longer enjoyed the preferential policies offered by local governments due to the long period since their establishment.

Meanwhile, to further advance the implementation of fair competition policies, fully implement the fair competition review system, and eliminate various market barriers, on June 13, 2024, the State Council issued the Fair Competition Review Regulations, effective from August 1, 2024. Article 10 of Chapter 2 of the Regulations states: "Policies and measures drafted by drafting units, without legal or administrative regulations as a basis or without approval from the State Council, shall not contain the following content affecting production and operating costs: (1) providing specific operators with tax incentives; (2) providing selective and differentiated financial rewards or subsidies to specific operators; (3) providing specific operators with preferential treatment in terms of factor acquisition, administrative and public service fees, government funds, and social insurance; (4) other content affecting production and operating costs."

After the Fair Competition Review Regulations were announced, there were speculations in the market that local policies might still offer smelters preferential treatment through other means. There were also reports suggesting that the implementation of the Fair Competition Review Regulations might be delayed by three years. Xinhua News Agency, Beijing, August 9, 2025 - The Decision of the Central Committee of the Communist Party of China on Further Deepening Comprehensive Reforms and Promoting Chinese-Style Modernization proposed: "Regulate local investment promotion laws and regulations, and strictly prohibit illegal and irregular policy preferences." This is a major deployment made by the central party leadership to promote the construction of a unified national market. It was made based on an accurate understanding of the phased characteristics of China's economic development and a deep grasp of market laws, from a holistic perspective.

In summary, regardless of market speculation, the overall trend has been set, with local incentives being completely phased out. Secondary lead smelters no longer have any fiscal "lifelines" to rely on.

II. Under such pressure of losses, why are secondary lead smelters still holding on? How long can they continue to do so?

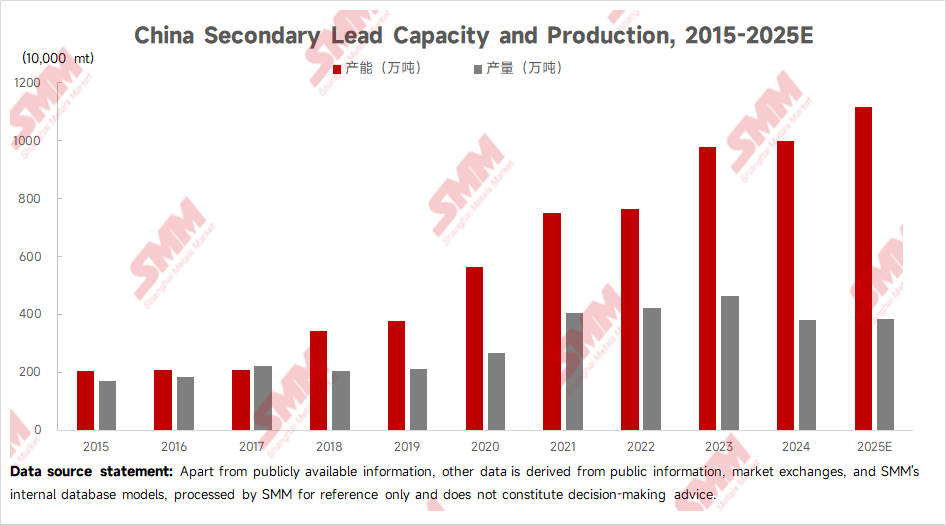

Although most secondary lead smelters are currently struggling, it would be unrealistic to say that no companies have gone bankrupt in recent years. Based on publicly available information, market exchanges, and SMM's internal database model, SMM found that between 2022 and 2025, the cancellation and suspension of new secondary lead projects reached 1.7 million mt, and the idle capacity of existing secondary lead smelters exceeded 1 million mt.

At the same time, the government is also consciously guiding the healthy development of the industry. On July 18, 2025, the State Council Information Office held a press conference to introduce the industrial and information technology development situation in H1 2025. Xie Shaofeng, Chief Engineer of the Ministry of Industry and Information Technology (MIIT), revealed at the meeting that MIIT will implement a new round of stable growth work plans for ten key industries, including steel, non-ferrous metals, petrochemicals, and building materials. These plans aim to adjust the structure, optimize supply, and eliminate outdated capacity. Specific work plans will be released soon. The press conference sent a clear signal, with the core message being "adjusting the structure, optimizing supply, and eliminating outdated capacity." For the secondary lead industry, the policy direction had already shifted from "expansion" to "optimization of existing capacity." The capacity for secondary lead smelting will bid farewell to past high-speed growth and enter a cycle of "gradually narrowing growth rates and slowly shrinking total volume."

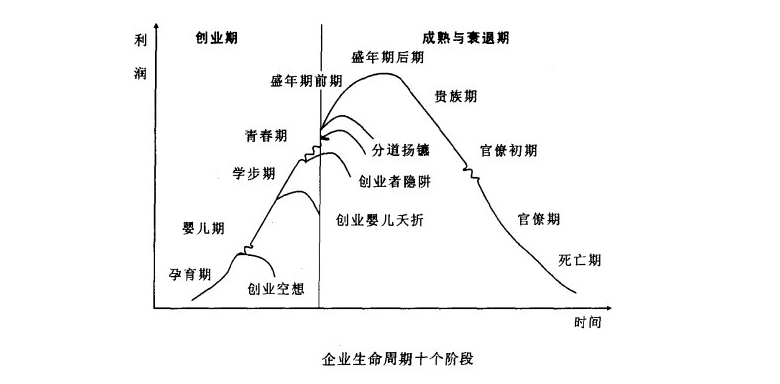

Ichak Adizes' corporate life cycle theory divides the business life cycle into ten stages: conception, infancy, toddlerhood, adolescence, prime, stability, aristocracy, early bureaucracy, bureaucracy, and death.

According to its cyclical characteristics, about 60% of companies follow the typical sequence: growth phase (3 years) → peak phase (3 years) → stable phase (3 years) → decline phase (3 years). From the development history of the secondary lead industry, 2025 is already in the decline phase, and as long as companies can weather this period, they have the potential to enter a new life cycle.

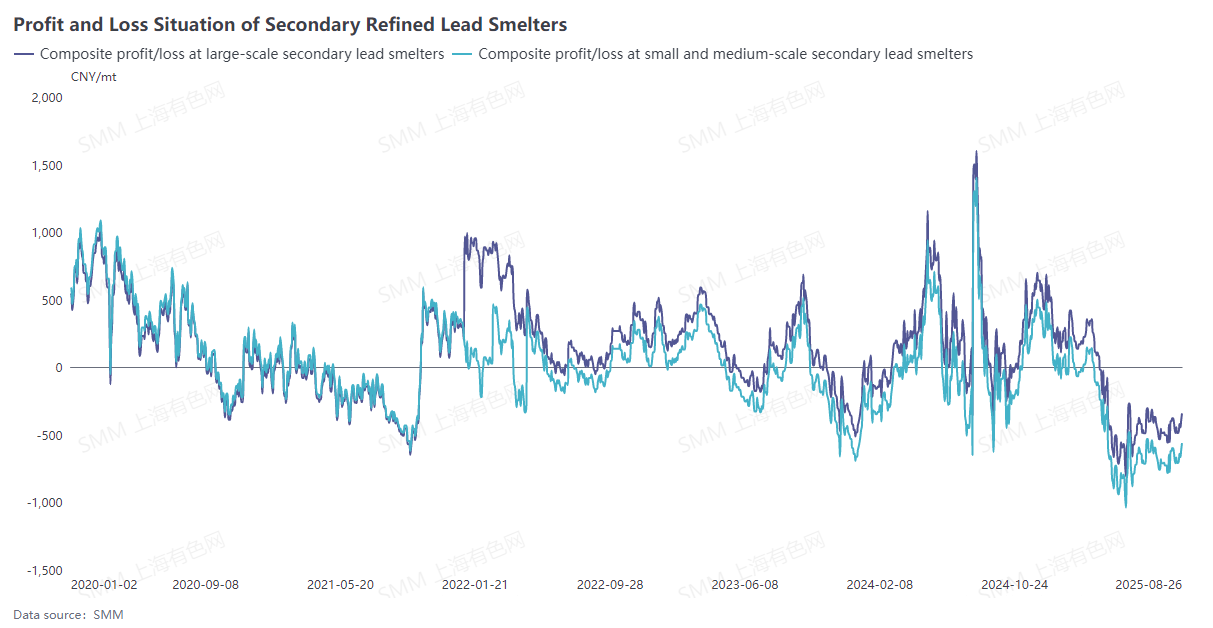

From the profit trend chart of secondary lead smelting, the excess profits accumulated during the previous boom cycle provide the necessary financial buffer for companies to navigate the current industry trough.

However, the depth and duration of the industry trough are difficult to predict, and the retained profits from earlier periods will eventually be depleted by continuous losses, with the safety cushion not being enough to hedge against systemic risks. Additionally, there are fewer than 10 state-owned secondary lead smelters in China, and no more than 20 private enterprises backed by battery producers; during the decline phase, the resilience of most secondary lead smelters is extremely weak.

In summary, the secondary lead industry is mired in a triple trough of tightening policies, capacity exit, and profit depletion. The reason companies continue to "bleed" while struggling on is largely due to the hope of surviving until the next boom after capacity optimization. However, limited profit buffers and fragile capital structures indicate that differentiation in the latter part of this "survival of the fittest" game will become increasingly pronounced.

![LME Lead Bottomed Out, While SHFE Lead Retreated After Rapid Rise and Consolidated [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/EhsCj20251217171721.jpeg)

![Tight Warehouse Supply in Jiangsu, Zhejiang, and Shanghai, Stronger Support From Firm Spot Price Offers [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/yqTpQ20251217171721.jpeg)