SMM August 19 News:

Recently, some overseas mining companies have successively released their Q2 reports. In the first half of the year, although heavy rains, floods, wildfires and other factors affected the output of some zinc mines, the newly commissioned capacities of zinc mines such as Oz and Kipushi were gradually released, and the outputs of mines like Antamina and Tara recovered. Overall, the output increment was quite significant. Let's take a look at the specific performance of each mining company.

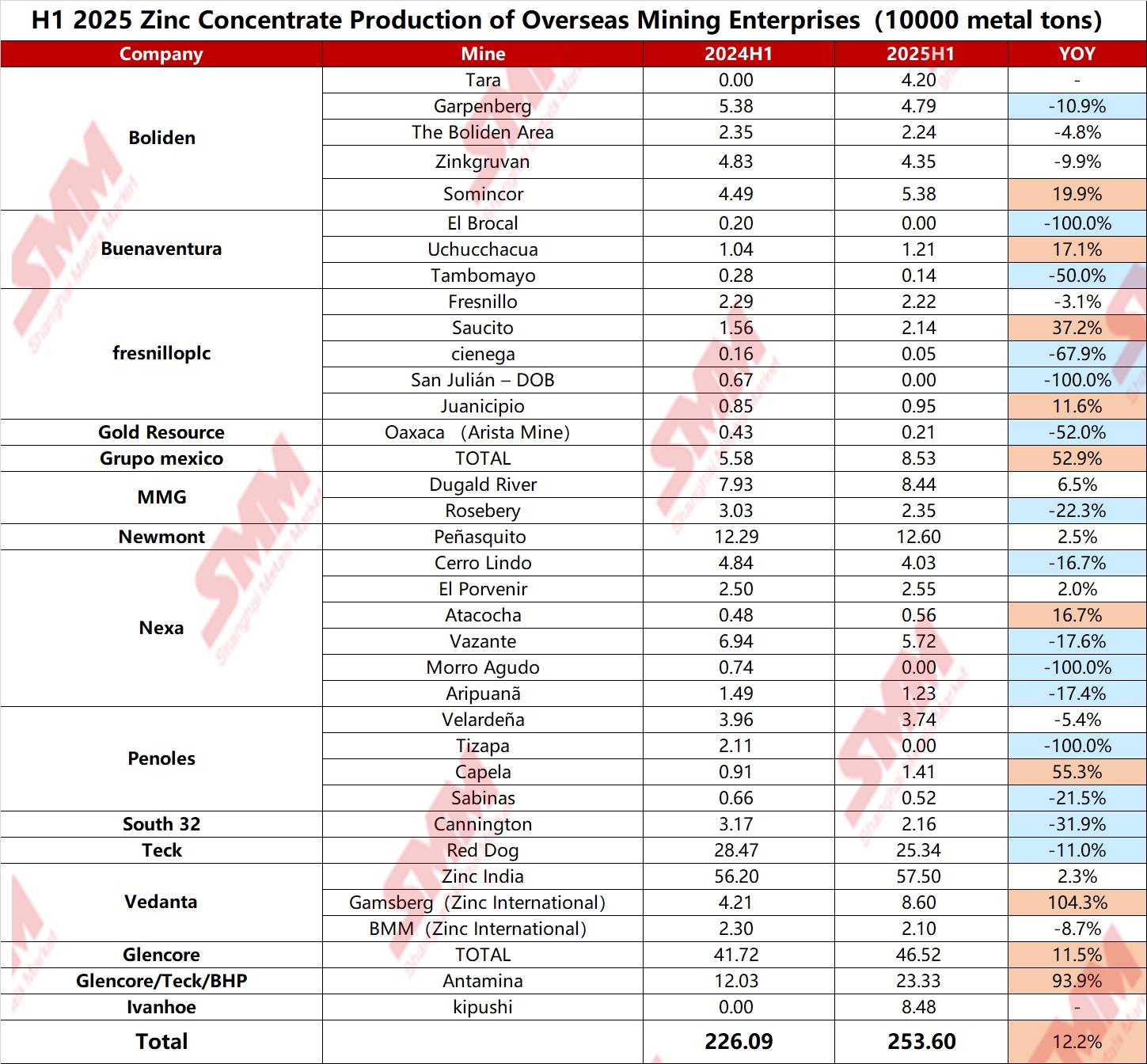

SMM conducted a statistics on the production situation of 15 major overseas mining companies (The zinc concentrate output of these 15 mining enterprises in 2024 accounts for nearly 40% of the global total zinc concentrate output). According to the data disclosed in the financial reports, the total zinc concentrate production of these 15 mining companies in H1 2025 was 2.536 million metal tons, an increase of 275,000 metal tons (12.2%) compared with 2.2609 million metal tons in H1 last year, showing a very significant year-on-year growth. The following figure shows the H1 production data of each mining company counted by SMM.

By mining company:

- Boliden: The total zinc mine production of Boliden in Q2 was 93,076 metal tons, including the zinc mine outputs of Somincor and Zinkgruvan which started to be counted from April 16. It increased by 61% month-on-month and 147% year-on-year. The report disclosed that the zinc concentrate production of The Boliden Area in Sweden in Q2 was 10,700 metal tons, that of Tara Mine in Q2 was 20,400 metal tons, and that of Garpenberg Mine in Sweden in Q2 was 23,300 metal tons.

- Buenaventura: The zinc mine production in Q2 2025 was 8,800 metal tons, increasing by 34% month-on-month and 22% year-on-year. The report disclosed that the resources of El Brocal Mine in Peru were exhausted in Q1 2024, and production was stopped from Q2 onwards; the zinc mine production of Uchucchacua Mine in Peru in Q2 was 6,900 metal tons, and that of Tambomayo Mine in Peru in Q2 2025 was 900 metal tons.

- MMG: The zinc concentrate production in Q2 2025 was 56,200 metal tons, increasing by 9% month-on-month and 12% year-on-year. By mine, due to a significant increase in grinding volume, the zinc concentrate production of Dugald River in Q2 was 43,600 metal tons, a year-on-year increase of 26%; due to the grade reduction caused by mining sequence and problems related to equipment reliability, the zinc concentrate production of Rosebery in Q2 was 12,600 metal tons, a year-on-year decrease of 20%. Its 2025 production guidelines are 170,000-185,000 metal tons and 45,000-55,000 metal tons respectively.

- Newmont: The zinc concentrate production in Q2 2025 was 67,000 metal tons, and the mine's 2025 production guideline is 236,000 metal tons.

- Nexa: The total zinc concentrate production in Q2 2025 was 73,500 metal tons, a month-on-month increase of 9%, mainly due to the improved performance of its operations in Peru. Compared with the second quarter of 2024, the output decreased by 12%, mainly due to the reduced output of Vazante and Aripuanã operations, but this was partially offset by the increased output of Atacocha and El Porvenir.

- Pan American Silver Corp: The total zinc concentrate production in Q2 2025 was 12,600 metal tons, a year-on-year increase of 25%. The mining company's 2025 zinc mine production guideline is 42,000-45,000 metal tons.

- TECK: The zinc concentrate production of Red Dog in Q2 2025 was 136,600 metal tons, a month-on-month increase of 17% and a year-on-year decrease of 2%, mainly due to the low ore grade, which was expected in the mine plan. The 2025 production guideline for the mine is 430,000-470,000 tons, 410,000-460,000 metal tons for 2026, and 365,000-400,000 metal tons for 2027.

- Vedanta: The total zinc concentrate production in Q2 2025 was 322,000 metal tons, a month-on-month decrease of 11% and a year-on-year increase of 7%. Among them, the total zinc concentrate production of Zinc India in India in Q2 2025 was 265,000 metal tons, a year-on-year increase of 1%; the zinc concentrate production of Zinc International in Q2 was 57,000 metal tons, a year-on-year increase of 50%. Driven by the improvement of mining capacity and higher throughput, the output of Gamsberg Mine increased significantly.

- Glencore: The self-produced zinc output in Q2 2025 was 251,600 metal tons, a year-on-year increase of 19%, mainly reflecting the increased zinc grade at Antamina and the increased output at McArthur River. Its 2025 self-produced zinc output guideline has been adjusted to 940,000-980,000 metal tons.

- Antamina: The zinc concentrate production in Q2 2025 was 142,000 metal tons, a year-on-year increase of 155%. Its 2025 zinc concentrate output guideline is 422,000-467,000 metal tons.

- Ivanhoe: The zinc concentrate production of Kipushi Mine in Q2 was 41,800 metal tons, and its 2025 production guideline target is 180,000-240,000 metal tons of zinc.

Outlook for the Market

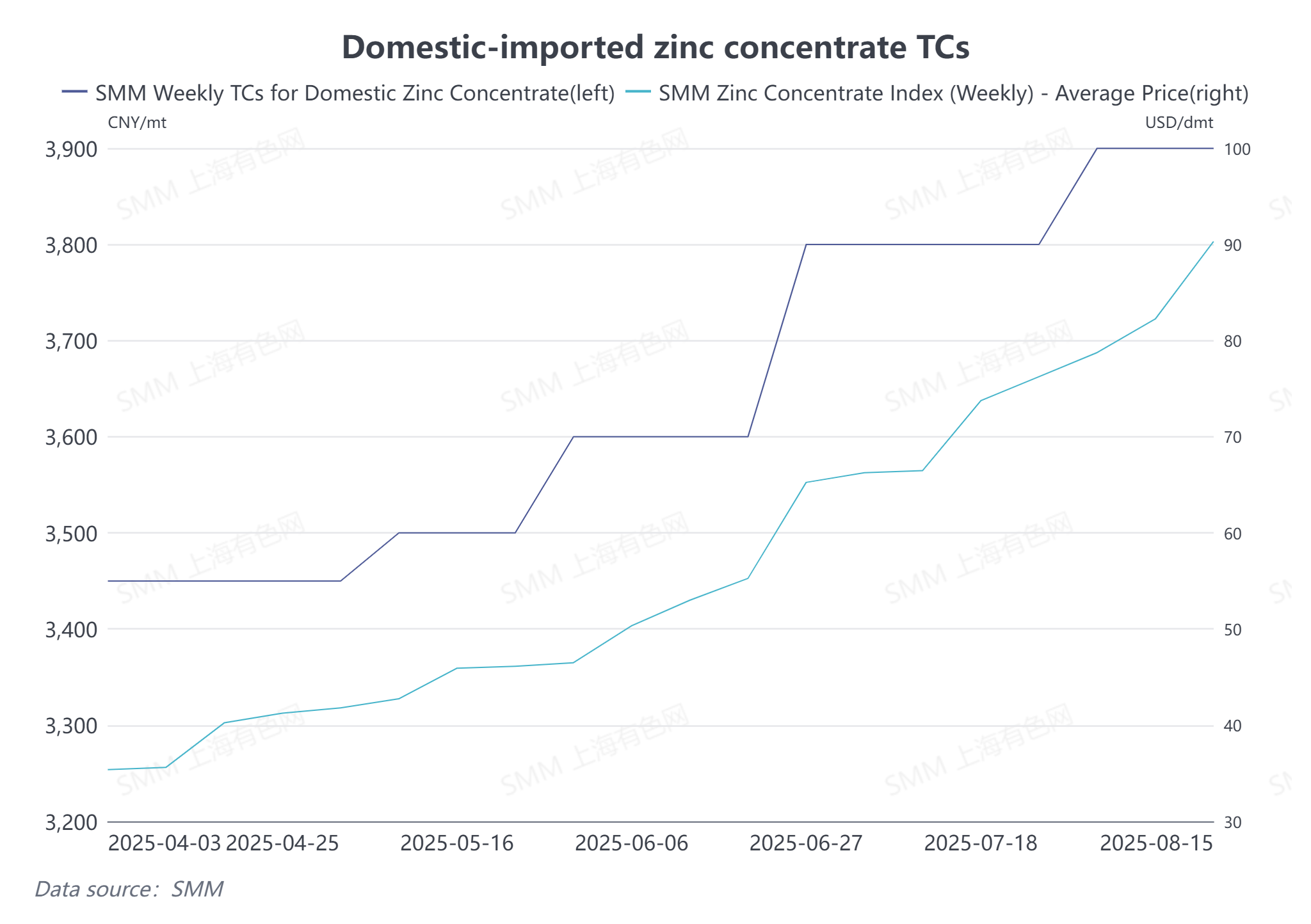

In the first half of the year, the Kipushi zinc mine operated smoothly, Antamina, Tara and other zinc mines resumed production as planned, and the Oz zinc mine also significantly increased its production, which began to flow into the domestic market in large quantities in May. With the continuous release or recovery of these capacities, it is expected that the zinc mine production in the second half of the year will continue to increase compared with the first half. Affected by this, China's cumulative imports of zinc mines from January to June this year increased significantly by 47.7% year-on-year, with a significant increase in import volume. Looking forward to the second half of the year, China's zinc mine imports are expected to remain at a high year-on-year level, continuously supplementing the domestic market supply. At present, the domestic zinc mine treatment charge (TC) has risen to more than 3,900 yuan/metal ton, and the import zinc mine treatment charge has exceeded 90 US dollars/dry ton. However, as the winter storage period in the fourth quarter approaches, the room for further increase in treatment charges is expected to be limited.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)