In the first half of 2025 (H1), there were two main topics surrounding recycled copper raw materials in China. Firstly, as the "reverse invoicing" policy was fully implemented across various provinces, the previous procurement model of secondary copper rod enterprises would change. However, whether domestic suppliers of recycled copper raw materials would cooperate with secondary copper rod enterprises in implementing the "reverse invoicing" policy remained a major challenge. Secondly, the US imposed high import tariffs on various countries, including China. In response, China imposed an additional 10% tariff on all US goods imported into China, with recycled copper raw materials also included. The domestic supply model of recycled copper raw materials was still in a transitional period under the gradual implementation of the "reverse invoicing" policy, while the ongoing trade tensions between China and the US forced many traders of recycled copper raw materials to shift their procurement sources from the US to other countries. Domestic recycled copper raw materials faced both "internal and external challenges," with long-term insufficient market circulation failing to meet market demand, resulting in artificially high prices for recycled copper raw materials.

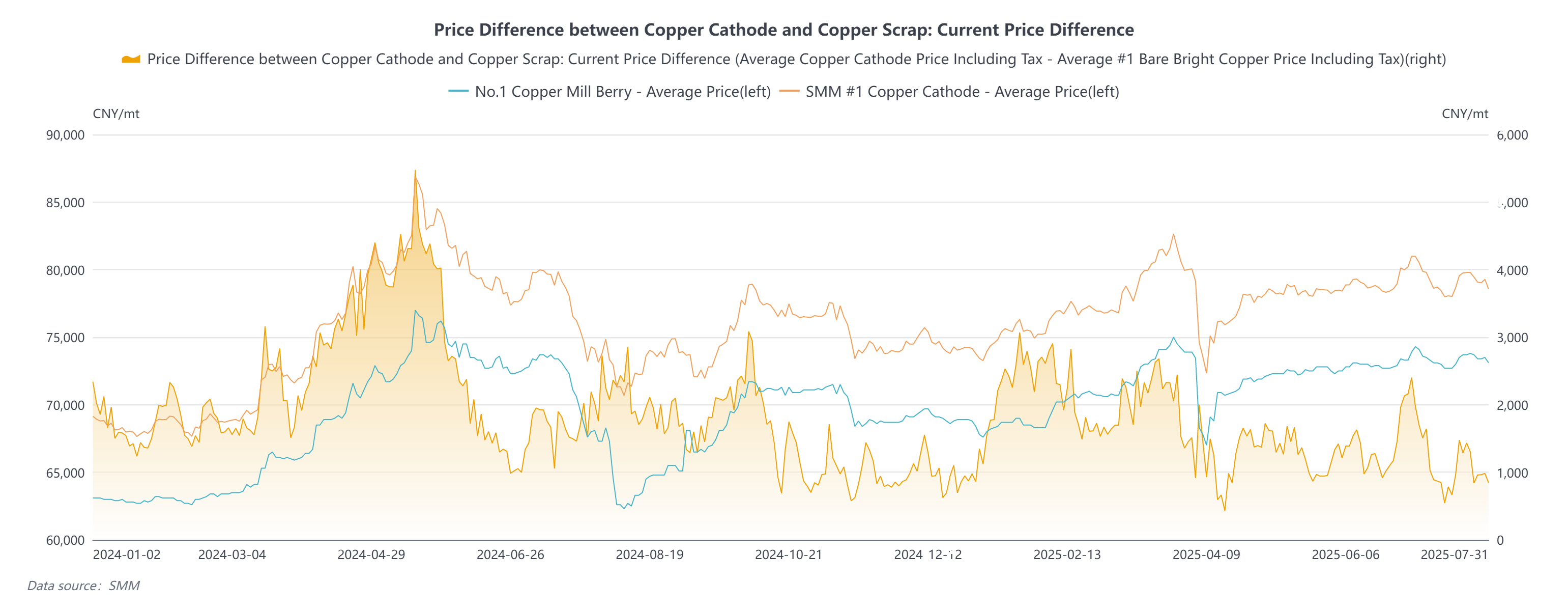

Firstly, let's look at the "internal challenges." Domestic copper prices showed an initial rise followed by a decline in H1, rebounding slightly before maintaining a fluctuating trend. Similarly, the price difference between primary metal and scrap hovered within the range of 2,000-3,000 yuan/mt in Q1. The steady increase in copper prices drove traders of recycled copper raw materials to actively sell, leading to a significant increase in market circulation of recycled copper raw materials compared to Q4 2024. The widening of the price difference between primary metal and scrap also indicated a relatively abundant supply of recycled copper raw materials.

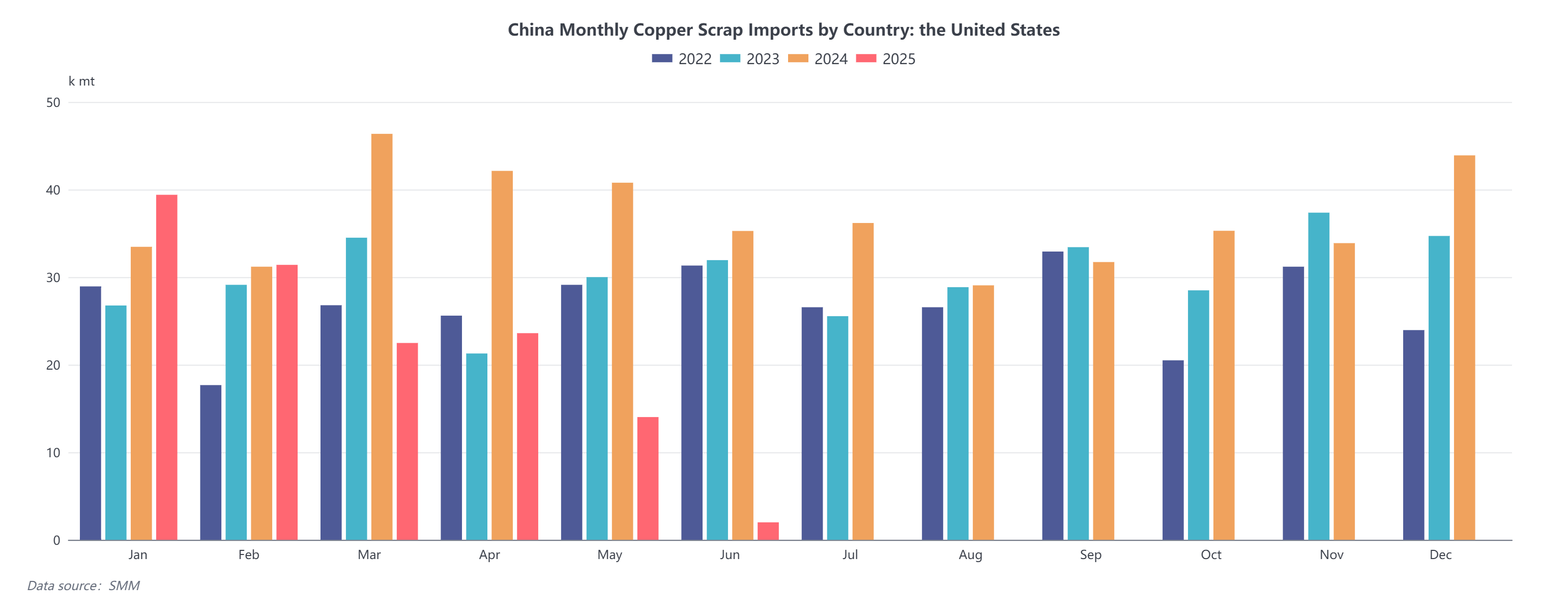

Finally, looking at the export data of secondary copper raw materials from the US, due to China's tariff countermeasures against the US, local traders of secondary copper raw materials in the US have had to gradually shift their focus from the Chinese market to Southeast Asian countries and the markets of Japan and South Korea. It is precisely the existence of Sino-US trade tariffs that has led to the mismatch in the export of secondary copper raw materials from the US. Chinese traders importing secondary copper raw materials, facing increased procurement costs due to import tariffs, can only turn their attention to Central Asia, the Middle East, and even Africa.

Looking ahead to H2, the supply situation of secondary copper raw materials in China is not optimistic. Due to the implementation pain period of domestic policies and the impact of the economic downturn, the market circulation volume of secondary copper raw materials is much lower than before. Overseas, the US and China are expected to conduct a second round of trade negotiations. Given that Trump has already implemented tariff hikes on imported goods from multiple countries, it seems almost certain that the US will continue to impose additional tariffs on Chinese imports. The mismatch in the supply of secondary copper raw materials from the US will persist. Under the circumstances where the supply landscape both domestically and overseas cannot be improved, the supply situation of secondary copper raw materials in China may remain tight in the medium and long-term.

As Q2 began, with Trump starting to impose hefty tariffs on Chinese exports to the US, it signaled the resumption of the China-US trade war after Trump 1.0. The market worried that the global trade war triggered by the US would have a significant impact on China's macro economy. Domestic copper prices fell accordingly, followed by domestic suppliers of recycled copper raw materials who had acquired a substantial amount of recycled copper raw materials when copper prices were high in the early stage. Now, with the significant retreat of copper prices, the inventory of raw materials held by suppliers of recycled copper raw materials suffered substantial losses. The vast majority of suppliers of recycled copper raw materials chose to hold back cargoes, causing the circulation volume of recycled copper raw materials in the market to plummet to a freezing point. The price difference between primary metal and scrap (including tax) even contracted to within 1,000 yuan/mt. Although China-US trade relations eased somewhat after the first round of negotiations, China still imposed a temporary 10% tariff on all US imports, while the US imposed a temporary 30% tariff on China. As long as the tariff issue remains unresolved, the market remains uncertain about the prospects for China's copper consumption, with limited rebounds in copper prices, followed by a prolonged period of consolidation with a fluctuating trend.

The copper price trend in Q2 of 2025 bears some resemblance to that in Q4 of previous years. When copper prices exhibit a fluctuating trend, the willingness to sell among suppliers of recycled copper raw materials tends to be low. According to exchanges with SMM, most traders of recycled copper raw materials in June-July this year generally maintained a low inventory level of recycled copper raw materials due to concerns about the volatility of copper prices. Additionally, traders generally adopted a "quick in, quick out" strategy, with the transaction price mostly being only 50-100 yuan/mt higher than the purchase price. After deducting daily expenses and other costs, the net profit from selling recycled copper raw materials for traders was minimal. (Regarding the coefficient performance of mainstream distribution areas for recycled copper raw materials in China, SMM conducted surveys on recycled copper raw material yards and traders, assigning scores based on current inventory levels, with a scale of 1-10. For example, a score of 5 indicates that the current inventory is at a normal level.)

Additionally, under low inventory conditions, recycled copper raw material traders tend to refuse to budge on prices when copper prices rise. When copper prices pull back, traders reduce prices by a minimal margin, sometimes even less than 50% of the daily copper price decline. The artificially high prices of recycled copper raw materials have caused significant difficulties for many secondary copper rod enterprises. Although Q2 marks the off-season for downstream consumption, with limited orders, the artificially high cost of recycled copper raw materials cannot be passed on to the downstream. Secondary copper rod enterprises have to bear the costs alone, and sales of secondary copper rods have been in a state of loss for a long time since May.

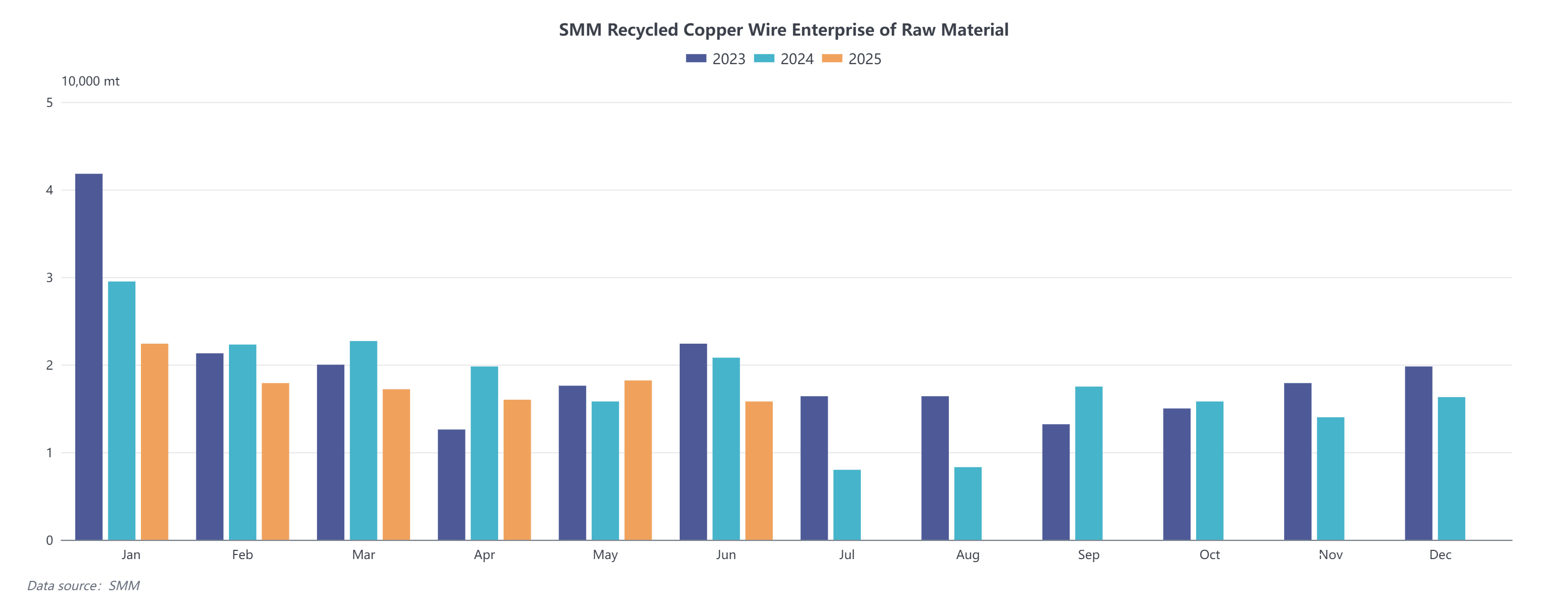

In addition to the impact of copper price fluctuations on the shipping sentiment of recycled copper raw material traders, the gradual implementation of "reverse invoicing" in various provinces this year has also led to a bottleneck in the procurement volume of raw materials for many secondary copper rod enterprises. According to monthly data from SMM, the monthly inventory of raw materials for secondary copper rod enterprises in April-May 2025 was lower than the same period in 2023 and 2024. In addition to the copper price factors mentioned above, the implementation of "reverse invoicing" has also posed difficulties for secondary copper rod enterprises in procurement.

The "reverse invoicing" policy explicitly stipulates that the invoicing limit for enterprises implementing "reverse invoicing" to the same natural person within 12 calendar months shall not exceed RMB 5 million. Currently, in China, most recycled copper raw materials are still recycled by family-run workshops and then handed over to secondary copper rod enterprises. If the sellers of recycled copper raw materials from family-run workshops do not cooperate with secondary copper rod enterprises in issuing "reverse invoicing" invoices, secondary copper rod enterprises can only turn to recycled copper raw material traders who can issue 13% VAT invoices for procurement. However, since the beginning of this year, factors such as copper prices and the poor performance of the domestic economic cycle have led to an extension of the scrap cycle for many scrap items, with a significant decline in the volume of scrap recovered by dismantling enterprises. The volume of recycled copper raw materials purchased by recycled copper raw material traders from formal dismantling enterprises also fell short of expectations. Therefore, the low monthly inventory of raw materials for secondary copper rod enterprises is mainly due to the unsatisfactory progress of "reverse invoicing" work, combined with the limited available sales volume of recycled copper raw material traders.

The shortage of domestic recycled copper raw material supply is difficult to change in the short term. In terms of imported recycled copper raw materials, it is also due to the tariff issues caused by the deterioration of Sino-US trade relations mentioned above.

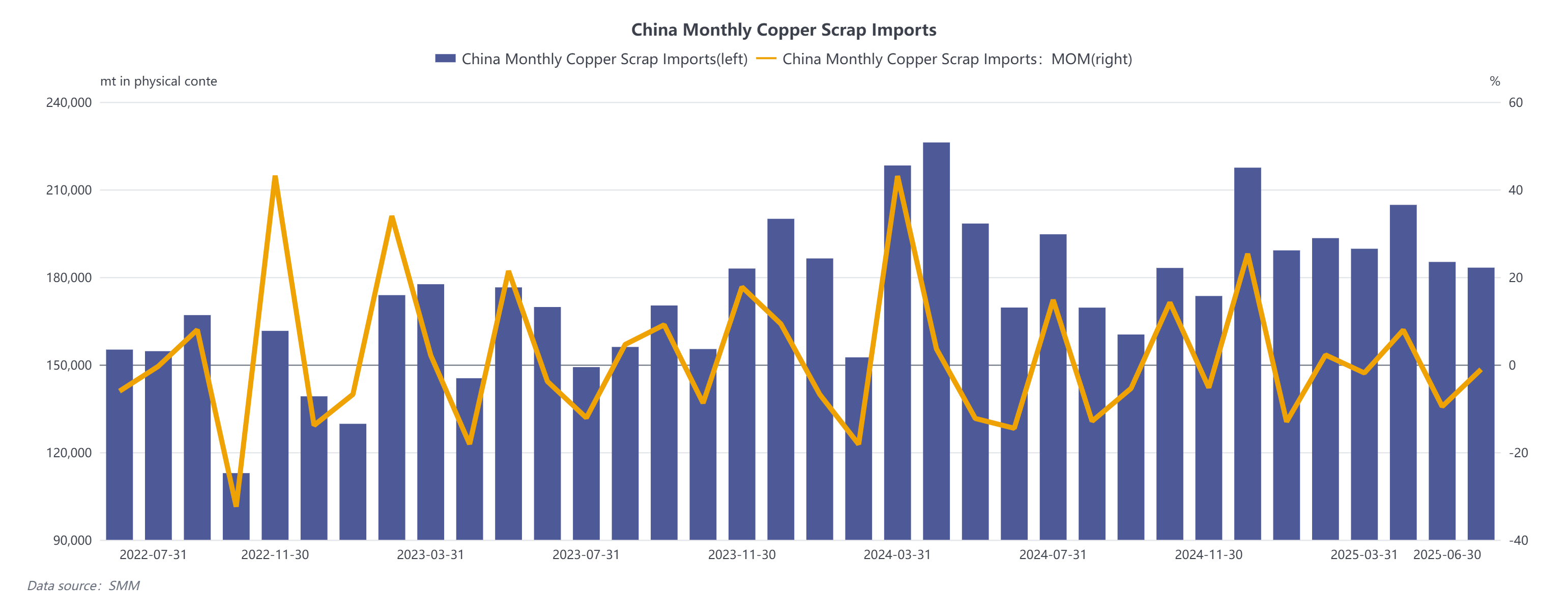

Firstly, according to the import data of recycled copper raw materials compiled by SMM, as of June 2025, the total imports of recycled copper raw materials in China for the first six months were 1.1454 million mt, a decrease of 0.5% compared to 1.1512 million mt in the same period last year.

China's imports of recycled copper raw materials declined YoY from March to May, while although there was a slight YoY decline in June, the YoY data increased by 8.06% against the trend. As early as April, the State Customs Administration issued documents stating that for recycled copper raw materials from the US shipped from April 10th and declared before 24:00 on May 13th (both time periods must be met), China's customs would only impose a 13% import VAT and would not impose an additional 10% import tariff. Therefore, in terms of time periods, the normal time from shipment to arrival at Chinese ports for US recycled copper raw materials is 30-45 calendar days. Thus, many import traders requested US traders to export recycled copper raw materials to China as soon as possible before June. The import data of recycled copper raw materials in April reached the peak in H1, and then declined normally in May. However, the June data only declined slightly by 1% MoM from May, which inevitably makes the market wonder whether Chinese import traders have quickly expanded overseas markets and achieved significant results in a short time after abandoning the US market.

According to the data on China's imports of recycled copper raw materials by country in 2024, the total annual imports of recycled copper raw materials from the US reached 439,200 mt, followed by Japan with 271,800 mt, Malaysia with 192,300 mt, and Thailand with 172,000 mt. In contrast, the US exported 959,300 mt of recycled copper raw materials in 2024. In other words, nearly 45.78% of the recycled copper raw materials exported by the US were directly sold to China, with the rest being dismantled, remelted, and recast in Southeast Asian countries before being shipped back to China. If both direct and indirect imports are combined, the proportion of recycled copper raw materials imported from the US may exceed 50%.

Finally, looking at the export data of secondary copper raw materials from the US, due to China's tariff countermeasures against the US, local traders of secondary copper raw materials in the US have had to gradually shift their focus from the Chinese market to Southeast Asian countries and the markets of Japan and South Korea. It is precisely the existence of Sino-US trade tariffs that has led to the mismatch in the export of secondary copper raw materials from the US. Chinese traders importing secondary copper raw materials, facing increased procurement costs due to import tariffs, can only turn their attention to Central Asia, the Middle East, and even Africa.

Looking ahead to H2, the supply situation of secondary copper raw materials in China is not optimistic. Due to the implementation pain period of domestic policies and the impact of the economic downturn, the market circulation volume of secondary copper raw materials is much lower than before. Overseas, the US and China are expected to conduct a second round of trade negotiations. Given that Trump has already implemented tariff hikes on imported goods from multiple countries, it seems almost certain that the US will continue to impose additional tariffs on Chinese imports. The mismatch in the supply of secondary copper raw materials from the US will persist. Under the circumstances where the supply landscape both domestically and overseas cannot be improved, the supply situation of secondary copper raw materials in China may remain tight in the medium and long-term.

![The Price Spread Between High-Quality Copper and Standard-Quality Copper Continued to Narrow, While SHFE Copper Spot Discounts Gradually Stabilized [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)

![Inventory Continued to Decline, Suppliers Held Prices Firm Accordingly, and Spot Trades Were Better Than Yesterday [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/KtfdC20251217171713.jpeg)