On 18th July, LME zinc opened at $2,737.5/mt, reached an intraday high of $2,826.5/mt and closed at $2,824.5/mt, up by $86.5/mt or 3.16%. As of Monday 21th July , LME zinc remained an upward trajectory and closed at $2,844.5/mt, maintaining strong price momentum. This marks a notable reversal from the bearish expectations for LME zinc widely held by analysts just a couple of weeks ago.

In mid-July 2025, LME zinc prices surged dramatically over the course of just a few trading sessions—specifically on 17th, 18th, and 21st July. Behind the stage, movement of price aligns closely with macroeconomic signals, warehouse dynamics, aggressive warrant cancellations and shifting market structures. Here's a breakdown of the key drivers and the logic behind what some in the market believe is the making of a squeeze.

Macro Background Set the Stage for the Rally in Base Metal

The broader macro environment in July 2025 created a stage for a base metals rally. The US dollar softened as inflation showed signs of easing, US economic figures of employment and PMI stays robust, and markets grew confident that the Fed would pause or even pivot from its tightening cycle, which is favourable for a a range of commodities, including zinc.

In parallel, China’s policy released positive signal of boosting steady growth. On 18th July, the Ministry of Industry and Information Technology (MIIT) announced new industrial support plans across sectors including steel, power, non-ferrous metals, emphasizing the promotion of advanced capacity and the phasing out of outdated capacity. Since the idea of 'anti-involution' was first released by the government during the meeting on 1st July, the message was quickly absorbed by the market and interpreted as a government intention to reduce blind capacity expansion, solve the issue of overcapacity and boost base metal demand. Although China's domestic support obviously has a greater impact on SHFE rather than LME and import arbitrage window for zinc ingot stays closed in China, the improved sentiment also lifted LME base metals broadly.

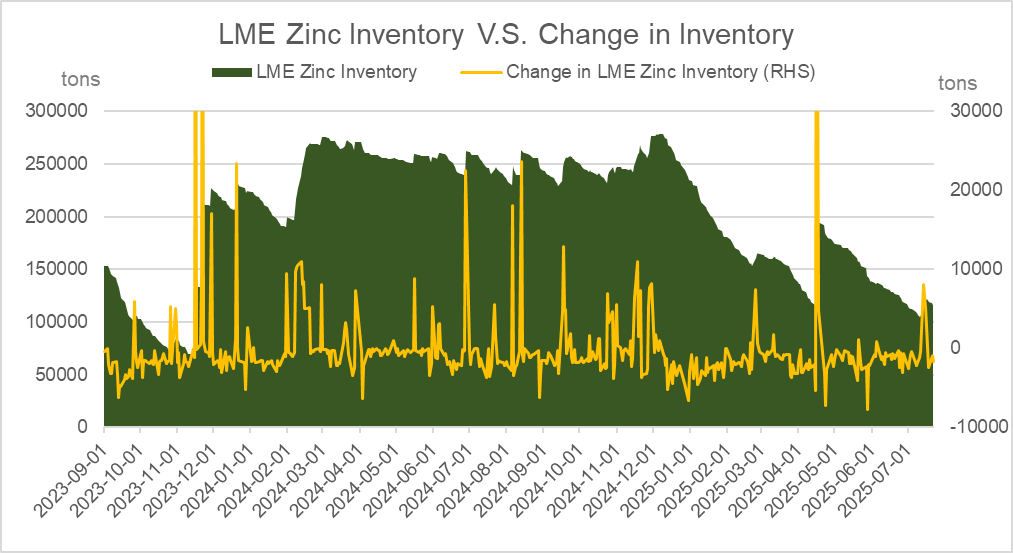

LME Zinc Inventory: Persistent Destocking and soaring calcellations

Another most important trigger for the boost in price, for zinc specifically, was the low level of LME zinc inventory. After the surge of LME zinc inventory happened in April, inventory continued to decline to around 105.25kt on 11th July. Much of the drawdown stemmed from sustained outflows from Asian warehouses, especially Singapore. According to customs data, Singapore exported 79.5kt of zinc in January–April 2025, with a 98% YoY increase.

Fig.1 LME Inventory decreases quickly in recent months

Before the sharp rally in zinc price, LME inventories experienced unusual volatility. Inventories briefly increased above 120kt in mid-July, but then quickly declined, as of the article is written on 22th July, to around 116.6kt.

Around 14th July, a portion of zinc ingots was registered as LME warrants, causing an immediate uptick in LME inventory. Market believed that short side might have delivered physical metal to ease the squeeze pressure. However, this relief was rather short-lived. Soon after, a large volume of warrants was cancelled from LME warehouses. On 21st July, cancelled warrants surged to 59.9kt, marking a massive day-on-day increase of 178.93%. The cancellation ratio jumped from under 20% to approximately 50% of total LME zinc inventories, meaning half of the available zinc was locked for delivery, sharply reducing spot metal availability in the market, bullish sentiment quickly intensified thereafter.

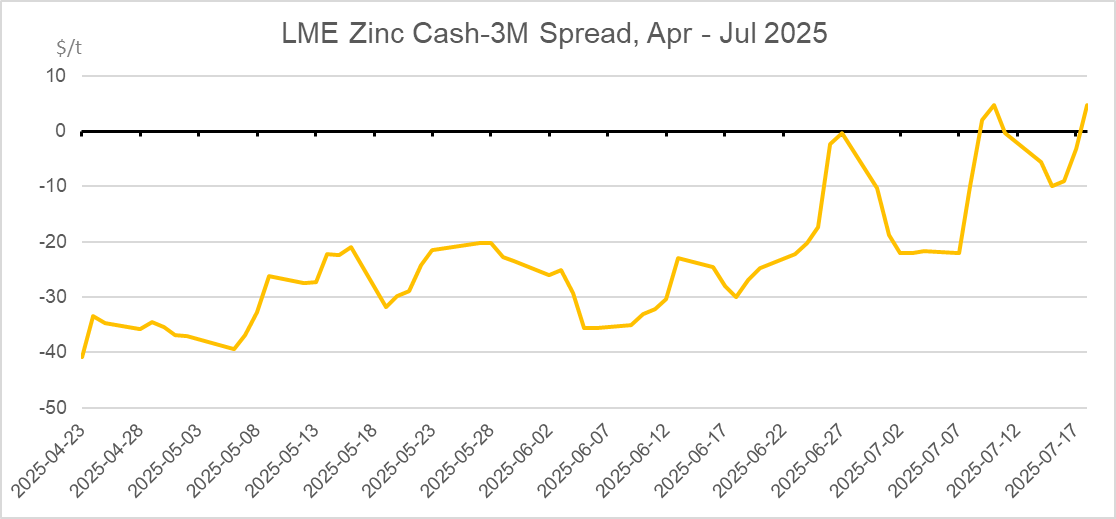

From Contango to Backwardation: Cash-3M Spread Sends a Signal

Another key signal was the shift in the LME zinc Cash-3M month time spread. Over the entire H1 2025, LME zinc sticks with a contango structure. However, with the continued destocking, structure started to flip.

Fig.2 LME zinc Cash-3M spread narrows down quickly while structure starts to flip

-

By 9th July, LME zinc Cash–3M spread narrowed from a few dollars of contango to a slight backwardation of $1.96/ton, marking the first time in six months that the term structure had flipped. This also indicated the initial signs of tightness in the spot market and served as a warning signal from the LME market that spot availability was tightening.

-

Following the emergence of backwardation on July 9th, LME inventories saw a slight rebound in mid-July, possibly due to some short sellers delivering physical zinc. As a result of this delivery, the spot premium quickly disappeared and the LME zinc Cash–3M spread reverted to a mild contango. The market expected no further squeeze to take place. However, this circumstance only lasted briefly.

-

Following the surge in cancelled warrants on 17th to 18th July, the volume of available zinc in the LME system dropped sharply, and the Cash–3M spread swiftly flipped back into backwardation. Around 18th July, the backwardation widened further. Falling inventories fueled expectations of a tightening spot supply.

The sudden shift of the Cash-3M spread towards backwardation, alongside the movement in inventory and warrant data, reinforced market's expectations of a deliberately tightened spot zinc supply and potential squeeze. These expectations, in turn, attracted speculative buying interest, which is eventually driving prices higher and creating a feedback loop.

Overall, the volatility in the LME Cash–3M spread during the recent times served as a key indicator of market sentiment and supply-demand dynamics. Behind the fluctuations, it correlates closely with the rapid inventory drawdowns and concentrated speculative positioning.

Capital Flows: Rising Position Concentration

During the recent zinc price rally, signs of concentrated long positioning drew significant market attention. In the second half of July, LME position reports showed that the proportion of long positions in nearby contracts rose markedly. Market data indicated that a small number of participants were accumulating long positions in front-month contracts while controlling a significant proportion of the cancelled warrants.

Such surges in position concentration are often seen as early warning signs of a short squeeze, which echoed with the behavior we've seen before some previous squeezes. One example would be in October 2024, when one major trader reportedly held over 40% of recent-month zinc open interest and stockpiled 50–80% of LME zinc warrants, this later drove LME zinc structure from contango to a steep backwardation.

This time in July, the rally in zinc price holds a series of similarities if we compare it with the past episodes. Unusually high level of concentration in long positions, sudden spike in the amount of cancelled warrants, along with the persistently low LME zinc inventory levels, all of these factors together indicate that it's likely that dominant players may have again strategically tightened the availability of deliverable zinc on the exchange to create a squeeze, pressuring on the short positions, forcing them to close out their positions, which is further accelerating the boost on LME zinc price.

It is worth noting that, following the nickel market crisis in 2022, the LME has been imposing certain restrictions to proactively improve their supervision over overly-concentrated positions. Previously in June 2025, a major trading house was compelled by the exchange to lend out a portion of its June aluminum holdings, which amounted to roughly 30%–39% of the open interest and far exceeded on‑warrant inventory to mitigate extreme positions amid growing concerns over an emerging squeeze. However, within the bounds of compliance, large funds can still influence short-term supply and demand by stockpiling in off-market warehouses or acquiring exchange warrants.

Going forward, market participants should closely monitor the LME’s regular reports on positions and warrants, e.g. COTR, to track capital flows and shifts in position concentration.

What Comes Next with Market Driver Unclear

Behind the recent surge in zinc prices, major international trading houses, have been widely rumored within the industry to be key driving forces. Market speculation suggests that large institutions may have leveraged their control over physical inventories and capital flows to aggressively build long positions in near-term contracts while simultaneously cancelling a significant volume of warrants, strategically creating a squeeze within the market.

Major trading houses may have multiple motivations for driving up zinc prices. On one hand, if they had previously accumulated long positions or stockpiled enough physical metal at lower prices, a sharp rally allows them to offload at higher levels for significant profit between two prices. On the other hand, a price surge can directly reshape profit distribution along the industrial chain. For vertically integrated trading houses in particular who owns both mining and smelting operations, their mines benefit from higher-value ores while smelters get higher profit margin from ingots sold at elevated price. While zinc smelters in ex-China region are generally suffering from low TC, limited profit margin and maintaining a relatively low level of production, enough physical metal and high zinc price would both be good news.

Surely, at the same time, the possibility of other market participants contributing to the recent rally cannot be ruled out. According to the latest COTR published by LME for 18th July, the percentage of long positions that the category 'Investment firms and credit institutions' is holding accounts for 57.41% of total open interest, up by 0.82% WoW. Certain hedge funds, investment banks and institutional investors may also have identified the squeeze dynamics in the zinc market and captured the opportunity to increase their long position to conduct arbitrage over calendar spread. However, based on the current knowledge, the ability to move large volumes of physical zinc metals remains concentrated in the hands of major players. Smaller players and funds typically lack the capital and operational infrastructure to generate such significant warrant movements on their own.

Looking ahead, a key risk would be that if the leading long side, whoever it is, begin to unwind their positions, a sharp reversal may follow. Previously cancelled warrants may return to the LME system and therefore trigger rapid price corrections. As such, investors should pay close attention not only to the underlying supply-demand fundamentals, but also to shifts in positioning and the behavior of large market participants, whose behaviour may drive the direction of market dynamics above the tight physical market.

Author: Yueang He, Zinc & Lead Analyst of SMM UK

Contact: yueanghe@smm.cn | +44 (0)7522 173725

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)