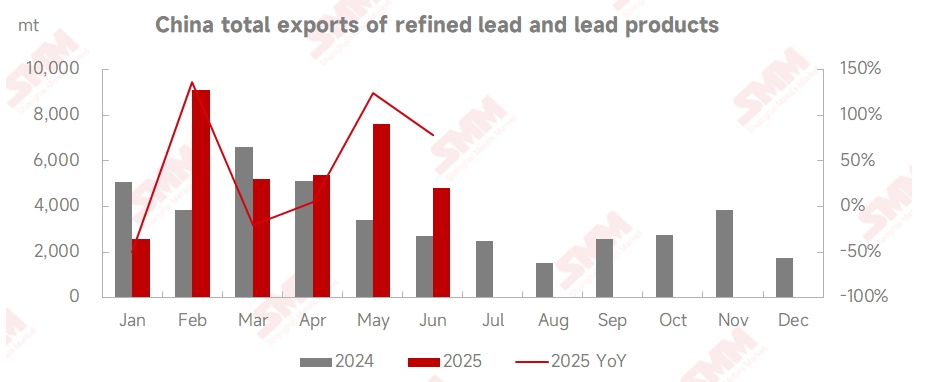

According to data from China Customs, in June 2025, China's refined lead exports stood at 3,183 mt, down 42.69% MoM and up 133.69% YoY. From January to June, the combined exports of refined lead and lead products reached 34,748 mt, with a cumulative YoY increase of 29.89%. On the import front, China's refined lead imports in June were 817 mt, while lead alloy imports were 10,657 mt. From January to June, the combined imports of refined lead and lead products were 75,013 mt, with a cumulative YoY increase of 152.1%.

According to the US Treasury's monthly budget statement, customs tariff revenue in May reached $23 billion, an increase of $17 billion compared to the same period last year, representing a growth rate of 270%. The May data was more than three times the monthly average in 2024. At the beginning of June, tariff risks continued to escalate, with non-ferrous metals generally weakening. Lead prices also remained in the doldrums, with the most-traded SHFE lead contract once approaching the 16,500 yuan/mt threshold. After mid-to-late June, maintenance activities increased among domestic lead smelters, coupled with environmental protection inspections, leading to delayed production resumptions among secondary lead enterprises. Primary lead inventories were gradually digested, causing lead prices to stop falling and rebound, breaking through the 17,000 yuan/mt threshold near month-end. The most-traded SHFE lead contract reached a high of 17,270 yuan/mt, setting a new three-month high.

Comparing LME lead and SHFE lead prices, after currency exchange rate calculations, the price spread between SHFE lead and LME lead remained large in June. This trend of "domestic market outperforms overseas market" continued in July.

China's lead ingot export situation is unfavorable, but the export of secondary crude lead from some tariff-privileged countries to China can be profitable. For example, crude lead from Japan, Malaysia, and Thailand entering the Chinese market has self pick-up quotations at a discount of around 200 yuan/mt against the SMM #1 lead average price. Sources rich in metals such as antimony and tin are quoted at parity or a small premium against the SMM #1 lead average price. As some domestic smelters are willing to accept non-taxed sources, after traders clear customs, the delivery-to-factory prices are reported to be around 15,750 yuan/mt (with variations in freight due to different transportation distances).

Lead prices continued to hold up well in July, with the interaction between tight raw material supply and expectations for a peak consumption season for lead. The overall center of gravity for LME lead and SHFE lead prices moved higher, with the most-traded SHFE lead contract reaching a high of 17,315 yuan/mt. As the US "reciprocal tariff" suspension period ended, the US government began issuing notifications of new tariff rates to countries that have not yet reached trade agreements starting from July 4, with tariff rates ranging from 10% to 70%, and plans to formally implement them starting from August 1. This upper tariff limit (70%) is significantly higher than the 50% announced in April. Now, as July approaches its end, the market is generally concerned that this move will exacerbate inflation risks in the US economy and may trigger a new round of asset sell-offs, with non-ferrous metals generally in negative territory. Meanwhile, there has been no significant improvement in domestic peak consumption season demand, with lead prices also reversing course and declining, and import conditions becoming less favorable.

Additionally, in July, there is an expectation for an increase in domestic lead ingot supply, especially with maintenance completions and production resumptions at secondary lead smelters, as well as the commissioning of new capacity. However, the current end-use consumption in the lead-acid battery market has not shown significant improvement, with dealers mainly focusing on digesting inventories. Orders for producers have seen limited improvement, and it is expected that the consumption increase will lag behind supply, which is also not conducive to lead ingot imports.

Overall, refined lead and lead product exports declined in June, with further declines expected in July. However, July imports are expected to remain relatively stable, with little change compared to June.

Data Source Statement:

All data other than publicly available information is processed by SMM based on publicly available information, market exchanges, and relying on SMM's internal database models. This data is for reference only and does not constitute a decision-making recommendation.