In previous summers, the fertilizer market entered the traditional consumption off-season, and industrial-grade MAP prices often came under pressure due to shrinking agricultural demand. However, this year differs from previous years as industrial-grade MAP prices did not experience a significant decline during the off-season but remained relatively high compared to the same period in previous years, showing an unusual trend of "stronger-than-usual off-season." Behind this price resilience lies the combined effect of demand structure changes triggered by the rise of the new energy industry, supported by raw material costs, and the reshaping of the supply-demand pattern.

As an important fertilizer raw material, industrial-grade MAP's traditional demand cycle is highly tied to the rhythm of agricultural production. Every year from June to August, as the fertilization period for summer-sown crops ends, the procurement volume of industrial-grade MAP in the agricultural sector drops significantly, and the market enters a seasonal adjustment phase. Over the past decade, the average price decline during the off-season has reached 8%-12%, with some years even experiencing a correction of over 15%. However, in recent years, this traditional cyclical pattern has been disrupted by the strong demand from the new energy industry.

The explosive growth of the LFP battery industry is reshaping the demand landscape for industrial-grade MAP. Industrial-grade MAP is a key raw material for iron phosphate, the precursor of LFP cathode material. With the expansion of the NEV and ESS battery markets, the procurement volume of industrial-grade MAP by related enterprises has continued to rise. During the agricultural demand off-season, the rigid procurement from the new energy sector effectively fills the demand gap, forming a new supply-demand balance of "agricultural retreat, new energy replacement" at the end of Q2 and the beginning of Q3.

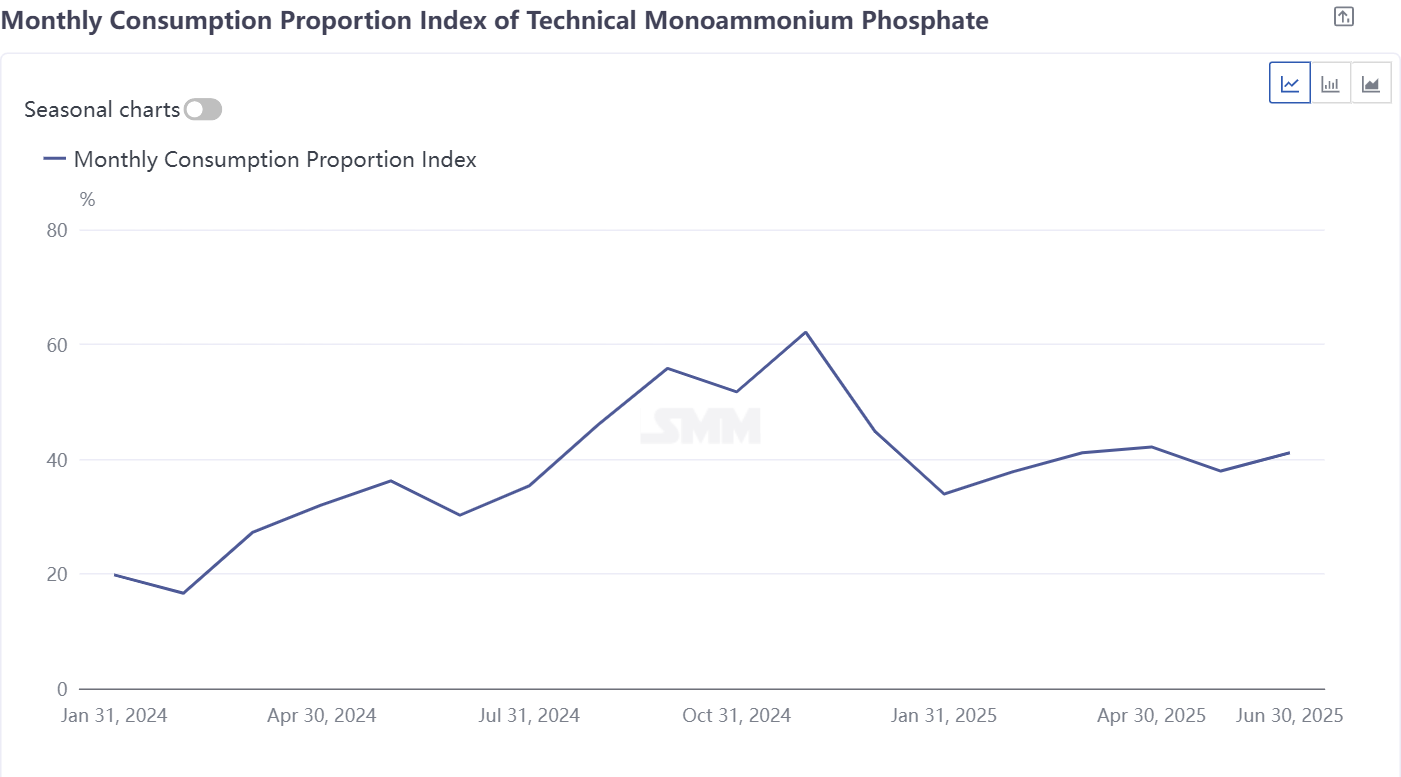

The monthly consumption proportion index of industrial-grade MAP reflects the monthly changes in the proportion of industrial-grade MAP in new energy demand, helping us better observe the demand situation of industrial-grade MAP in the iron phosphate and LFP industries.

The high-level operation of raw material costs has provided a solid floor for industrial-grade MAP prices. Phosphate ore, as an upstream resource in the new energy industry chain, has had its strategic value reassessed. Some mine enterprises have shifted to signing long-term contracts with battery material enterprises, further tightening the supply of phosphate ore for fertilizer use. Meanwhile, influenced by the geopolitical situation in the Middle East, international sulfur prices have fluctuated upwards, with domestic CIF prices rising by 28% compared to the beginning of the year, indirectly pushing up the production costs of industrial-grade MAP. The tight balance in the supply-demand pattern has strengthened market expectations for price resistance. Especially when industrial-grade MAP inventory is low, leading enterprises have successively introduced policies to refuse to budge on prices, with some even suspending quotations to observe the market, further exacerbating market bullish sentiment.

In the long run, the industrial-grade MAP market is undergoing a profound transformation from being "agriculture-dominated" to being "driven by both agriculture and new energy." The continuous expansion of the new energy industry will reshape its demand curve, while the enhanced strategic attributes of phosphorus resources may keep the industry in a state of tight balance for a long time. This structural change implies that the traditional cycle of peak and off-peak seasons may be disrupted, and the price center of industrial-grade MAP is expected to systematically rise with the support of new energy demand.