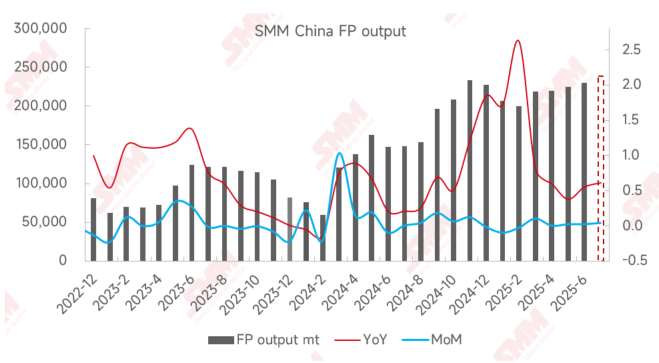

In June, the domestic iron phosphate market showed a steady yet increasing trend, with production increasing slightly by 2% MoM and significantly by 56% YoY. On the supply side, enterprises maintained a stable production pace. Although a few enterprises underwent maintenance, it did not significantly impact overall production, with limited monthly increases. On the demand side, some downstream LFP enterprises saw an increase in orders, directly boosting the sales growth of upstream iron phosphate enterprises. Additionally, as enterprises aimed to meet their mid-year sales targets and prepare for business negotiations in H2, market activity increased.

On the cost side, the prices of industrial-grade MAP and phosphoric acid remained stable in June. Although the price of ferrous sulphate increased, the overall cost fluctuation was relatively small. Due to a lack of cost support, iron phosphate prices continued to weaken, with some enterprises more actively reducing prices to ensure shipments.

In July, with the resumption of production by enterprises undergoing maintenance and the gradual release of capacity, iron phosphate production is expected to increase slightly. It is projected that production will increase by 4% MoM and 61% YoY in July.

While ensuring supply, enterprises will continue to monitor changes in costs and demand, adjusting their production and sales strategies to adapt to market dynamics.