On June 5th, the ASEAN Coal Industry Conference 2025, part of Indonesia Critical Minerals Conference & Expo 2025, hosted by SMM Information & Technology Co., Ltd. (SMM), supported by the Ministry of Foreign Affairs of Indonesia as a government supporter, and co-organized by the Association of Indonesian Nickel Miners (APNI), the Jakarta Futures Exchange, and Sxcoal, wrapped up in Jakarta, Indonesia!

This Coal Industry Conference brought together authoritative experts and corporate representatives from the global mining sector to engage in in-depth exchanges and forward-looking discussions on core topics such as the supporting role of mining services in Indonesia's coal industry, the strategic value of Indonesian metallurgical coal to the world's steel industry, "Value Symbiosis of China's Coking Coal and the Global Coal Supply Chain," a comparison of credit quality between coal producers in Asia and North America, the global market transmission mechanism of Indonesia's coal benchmark prices, changes and trends in global coal trade flows, the construction of a sustainable supply chain for coal in the cement industry amid energy transition, the geopolitical and decarbonization game faced by metallurgical coal, as well as the current state of the coal markets in China and India and the role of coal in Asia's energy transition. The conference aimed to provide practical and strategic guidance for the high-quality and sustainable development of the global coal industry in the context of energy transition through the collision of industry wisdom and the sharing of experiences.

Guest Speeches

June 4th

Keynote Speech: The Role of Mining Services in Supporting the Coal Mining Industry in Indonesia

Speaker: Bambang Tjahjono, Executive Director of ASPINDO (Indonesian Mining Services Association)

Why Use Contractors?

In Coal Mining:

1. The coal price index is relatively low compared to operating costs (cost-sensitive)

Coal mine owners find it difficult to flexibly respond to production fluctuations

It is difficult to invest in heavy equipment during (temporary) production increases

Production cuts affect equipment utilization rates and lead to idle labor

Unable to compare ideal costs with actual costs

2. Contractors are more flexible in adapting to production fluctuations

• In case of production cuts, equipment and labor can be reallocated to other sites

• If there are labor fluctuations due to production increases or decreases, work shifts can be adjusted from two shifts to three shifts

Overall, the total cost of using contractors is lower.

In Mineral Mining:

A few years ago, almost all mineral mining was carried out by mine owners themselves because the mineral price index was much higher than operating costs (not cost-sensitive).

• Due to safety concerns, mine owners worried that contractors would not be able to properly separate ore from scrap.

The current situation has changed the mindset of mine owners:

• Price indices have dropped significantly.

• Greater focus on cost issues.

• Using contractors offers cost advantages.

Prospects for Indonesia's Coal Industry

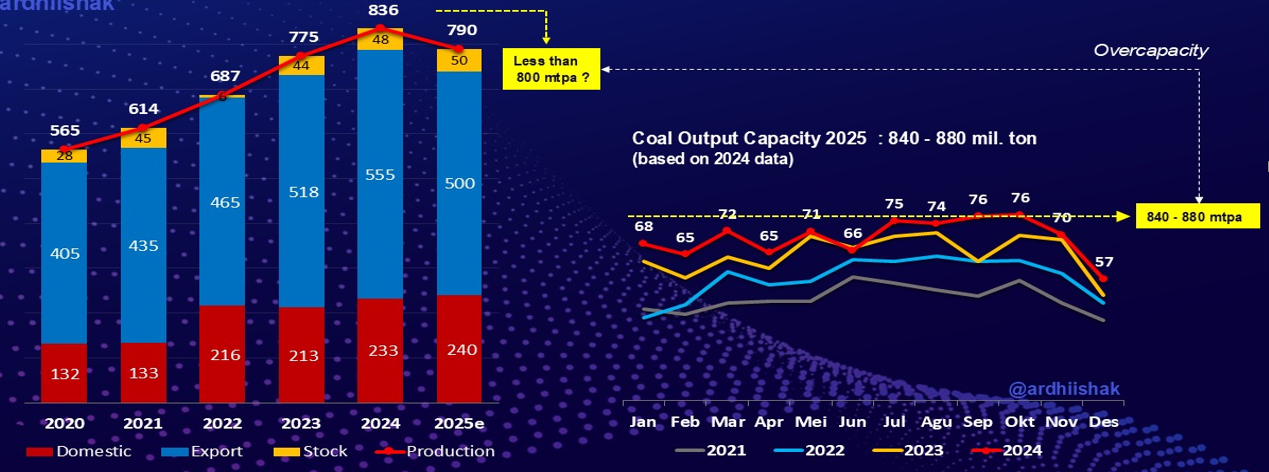

In 2025, Indonesia's coal production will be below 800 million mt, a decrease of approximately 5.6% compared to 2024. In 2025, exports will reach a maximum of 500 million mt, showing a significant decline YoY. Domestic demand will continue to grow, but at a limited rate.

Expected Responses to Declining Coal Demand

► For contractors:

1. Diversify business operations : Shift into the mineral sector, participating as contractors or mining parties.

2. Streamline equipment quantities : Ideally, all contractors should hold at least 25% of their equipment with a book value of zero (Note: This may refer to outdated equipment/equipment that has been fully depreciated).

3. Adjust work shifts : Change from a two-shift system to a three-shift system to avoid layoffs.

Keynote Speech: The Importance of Indonesian Metallurgical Coal Growth in Supporting the World Steel Industry

Speaker: Hendri Tamrin, Director of PT Adaro Minerals Indonesia Tbk

Keynote Speech: Value Symbiosis of China's Coking Coal and Global Coal Supply Chain

Speaker: Yin Yue, Director of the Energy and Chemical Department, Shanxi Coking Coal Group International Trading Co., Ltd.

Keynote Speech: Assessing Credit Quality: Contrasts Between Asian and North American Coal Producers

Speaker: Maisam Hasnain, Vice President and Senior Credit Officer, Moody's Ratings

Keynote Speech: Indonesia's Coal Benchmark Price (HBA) - How Is It Going to Impact the Global Market

Speaker: Ashok Mitra, Director and CEO of PT Kaltim Prima Coal

He elaborated from perspectives such as seaborne thermal coal, international coal price indices, coal futures prices, and coal price indices.

Coal Benchmark Price (HBA)

Below is a summary of the HBA formula:

1. According to Article 159, Paragraph 1 of Presidential Decree No. 96/2021, coal sales must reference the benchmark price.

2. The determination of HBA and HMA will be published on the 1st and 15th of each month, with the following formulas:

• HBA on the 1st = (0.7 * x1) + (0.3 * x2);

X1 = w4 from two months prior to the previous month

X2 = w2-w3 from the previous month

• HBA on the 15th = (0.7 * x1) + (0.3 * x2)

X1 = w2-w3 from the previous month

X2 = w4 from two months prior to the previous month

Example of Data Entry into the ePNBP System:

If the FOB price is lower than the HPB price, additional royalties must be paid on the difference between the HPB and FOB prices. Furthermore, additional taxes must be accrued/paid on the difference between the HPB and FOB prices.

Royalty Rates

• Starting from 2025, the royalty rate for domestic industries, excluding smelters, has been adjusted to 14%. This adjustment is in line with ESDM Ministry Regulation No. 58.K/HK.02/MEM.B/2022, issued on April 11, 2022 ("Regulation on Coal Selling Prices to Meet Domestic Industrial Raw Material/Fuel Needs"), which stipulates an HBA price of $90 for domestic industries, excluding smelters, and Presidential Decree (PP) No. 18/2025, which imposes a 14% royalty rate on coal sales subject to regulated prices (i.e., HBA $70 and HBA $90).

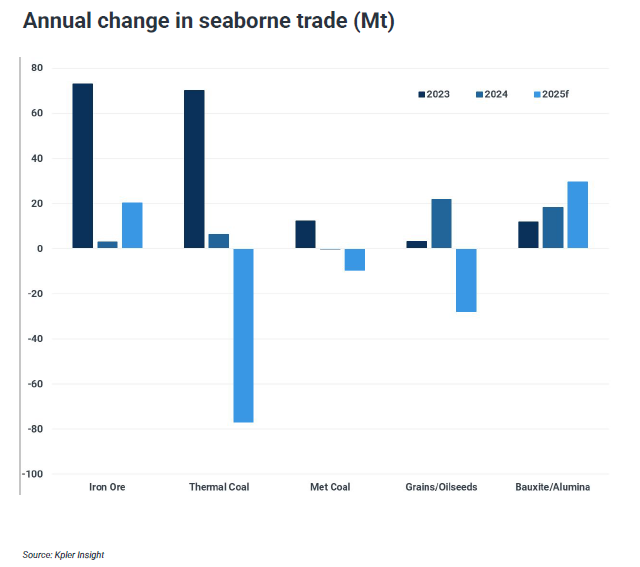

Keynote Speech: Global Coal Trade Flow Shifts: Current Trends and Future Outlook

Speaker: Dong Huanhuan, Senior Consultant at SMM

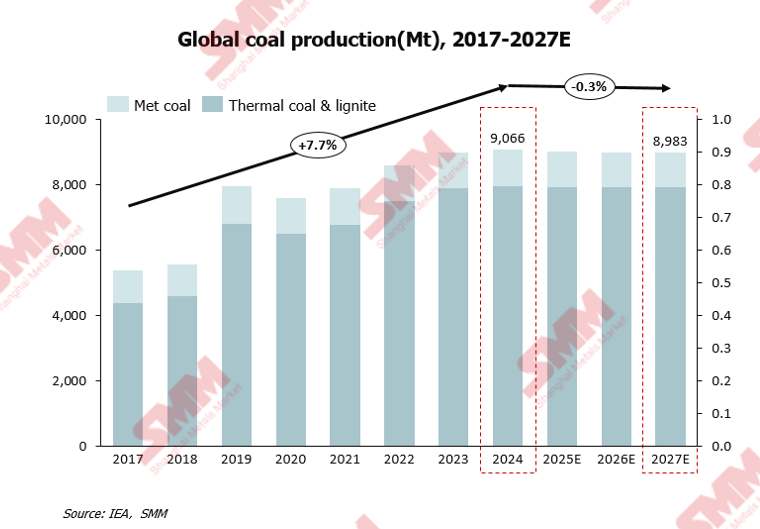

Global coal production is expected to decline after reaching a record high in 2024

In 2024, global coal production exceeded 9 billion mt for the first time, reaching a record high, but is expected to gradually decline in the coming years.

The main influencing factors are as follows:

The global energy transition is accelerating. The rapid development of renewable energy sources such as wind and solar is gradually replacing coal as the primary source of electricity.

With the establishment of the "dual carbon" goals, some countries globally, such as Germany and the UK, have gradually restricted or phased out coal mining and use.

The shift in the global economic development model and the increasing proportion of service and high-tech industries (which have relatively lower energy demands) have further suppressed the growth of coal demand.

Before 2024, global coal production had been on a growth trend, but it is expected to decline by 2027, except in India.

In 2025, China's total coal production is expected to maintain a slight growth trend, while India will continue to experience rapid growth in the coming years. The Indian Ministry of Coal has set a coal production target: an increase of over 40% from the 2025-26 fiscal year to the 2029-30 fiscal year. In the coming years, other major coal-producing countries will maintain a downward trend in production.

Keynote Speech: The Critical Role of Coal in the Cement Industry: Energy Transition and Supply Chain Sustainability

Speaker: Renard Cheng, Senior Purchaser at PT Indocement Tunggal Prakarsa Tbk

Keynote Speech: Global Coal Market and Price Trend and Outlook

Speaker: Kevin Lee, Senior Research Analyst at McCloskey

Panel Discussion: Metallurgical Coal at Crossroads: Navigating Geopolitics, Decarbonization and Steel Demand

Moderator: Ghee Peh, Energy Finance Expert at the Institute for Energy Economics and Financial Analysis (IEEFA)

Panelists: Bank Mandiri IndonesiaDendi Ramdani, Vice President of Industrial and Regional Research

FH Kristiono, Deputy Secretary General of APBI-ICMA

Andre Barahamin, Community Outreach Coordinator at IRMA

Keynote Speech: Optimizing Coal Logistics Transportation Efficiency: New Strategies for Integrating Technology and Sustainable Developmen

Speaker: Hanif, Senior Dry Bulk Shipping Analyst at Kpler

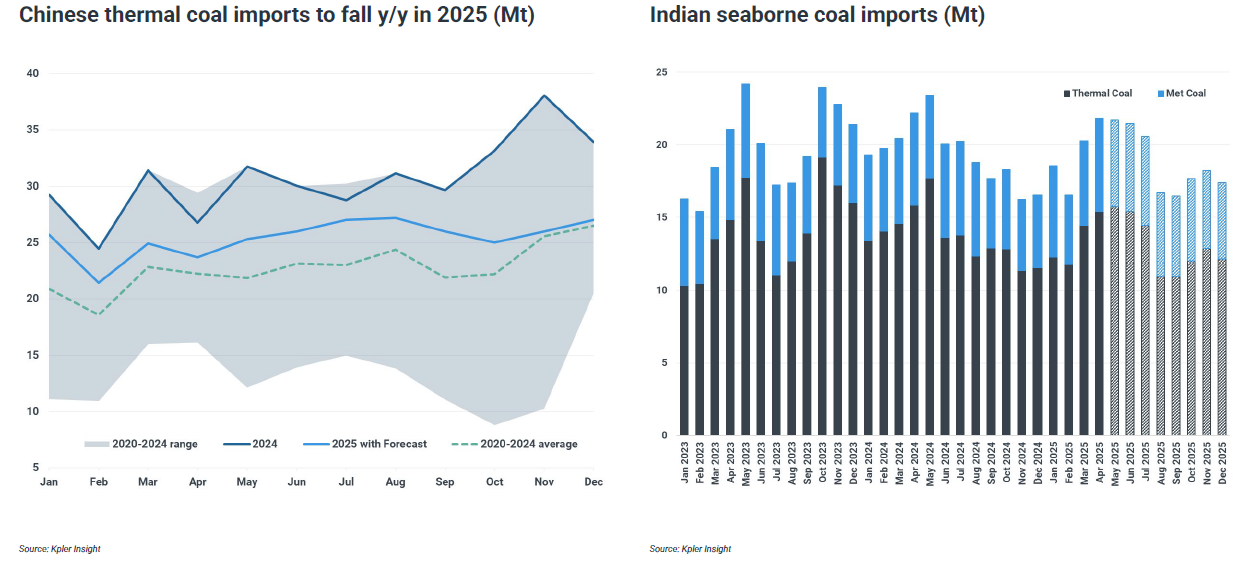

Rebalancing of the Pacific Coal Market and Its Impact on the Dry Bulk Shipping Industry

Demand for coal imports in major countries is expected to decline

Due to reduced demand for thermal coal and increased land-based metallurgical coal supply, seaborne coal imports are expected to decline in 2025.

Declining coal demand will drag down the shipping industry

Reduced coal demand will exert downward pressure on the demand for dry bulk fleets.

It provided an introduction on aspects such as the global dry bulk fleet's share and the contribution of dry bulk to shipping demand in 2024.

Ship earnings will struggle to find support.

Insufficient vessel utilization has exacerbated the supply surplus, and the bearish outlook for oil prices has reduced shipping costs.

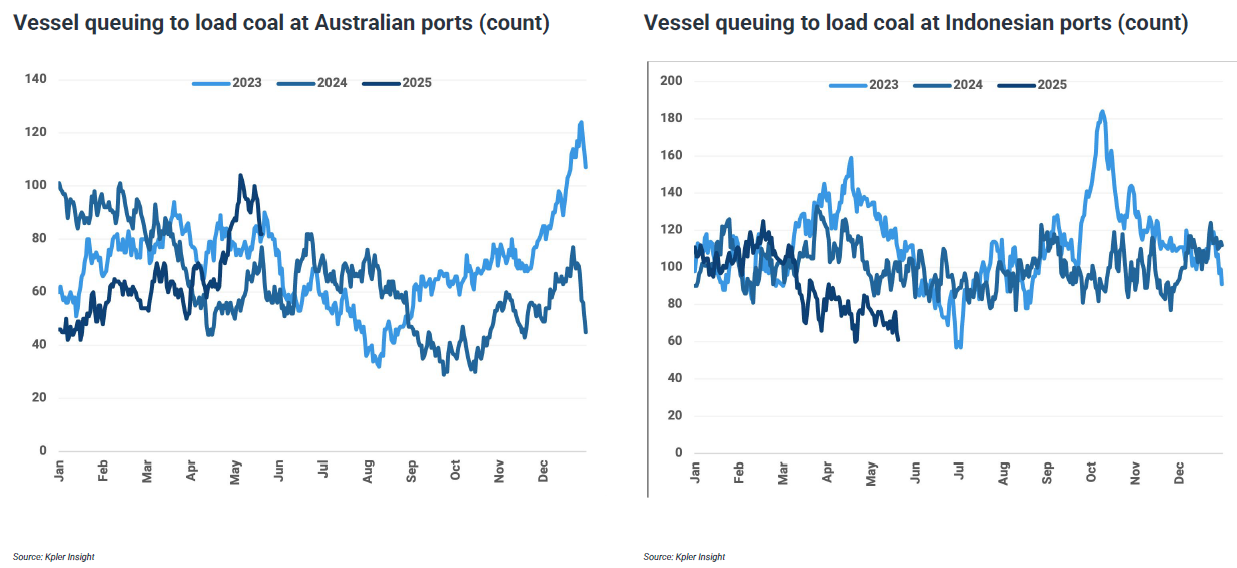

Port delays have decreased, but the reasons vary.

Reduced weather-related disruptions to shipping and lower demand have freed up more space at ports.

Time for scheduled maintenance.

Ships built from 2010-2012 are approaching special surveys, which may tighten capacity supply over the next three years.

It discussed the dry bulk fleet, including the existing and under-construction fleets, as well as the proportion of fleets requiring special surveys by year.

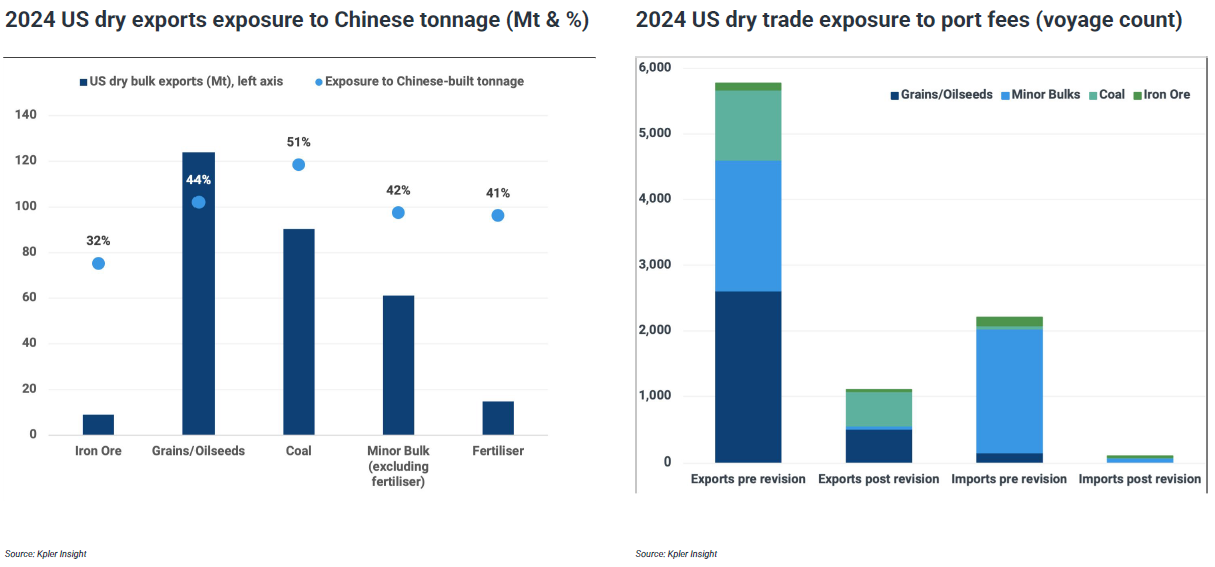

What the US port fees could have done but didn't.

If the initial rules are passed, nearly half of US coal and grain exports will face increased fees.

Key Points.

►Key Points and Outlook.

Declining coal demand affects shipping and earnings, while fleet aging and policy easing have improved market sentiment.

• Coal demand in China and India is in the doldrums. This has limited the growth of seaborne trade for the dry bulk fleet.

• With reduced coal demand, the utilization rates of Panamax and Supramax fleets are decreasing, leading to lower shipping demand.

• Ship earnings are facing downward pressure. Shipping costs have slightly decreased with falling oil prices.

• Port delays have decreased, and port space has increased, primarily due to reduced coal handling volumes.

• The dry bulk fleet will undergo special repairs from 2025-2027, which will begin to limit capacity supply.

Panel Discussion: The Future of Thermal Coal Demand: Asia's Energy Mix and the Rise of Renewable Energy.

Moderator: Djakarta Mining Club. Vice Chairman Ben Lawson.

Panelist: Manager and Founder of Strategic Point Partners. Charles J. Tumazos.

Chairman of Industry Relations and Industry Associations at Perhapi.Ardhi Ishak.

Director, Vasudev Pamnani, iEnergy Natural Resources Ltd.

Guest speeches

June 5

Keynote speech: Regional Coal Market Outlook: China

Presenter: Feng Dongbin, Deputy General Manager of Fenwei Digital Information Technology Co., Ltd.

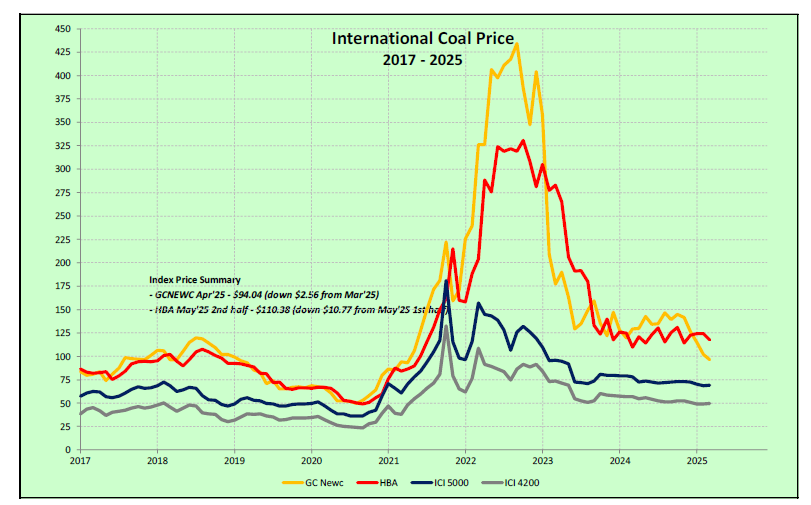

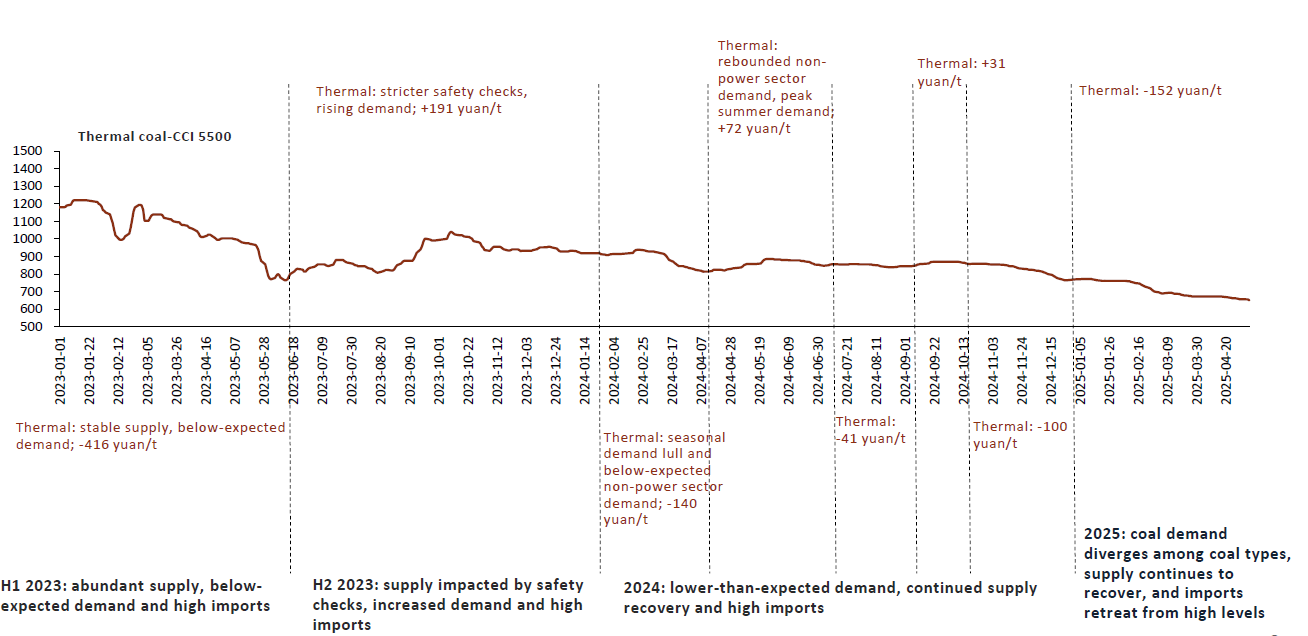

China's coal prices showed a downward trend in 2024, and this trend is expected to continue into 2025

Spot prices lower than futures contract prices

Thermal coal prices on May 23, 2025:

• CCI 5500 was 618 yuan/mt, 57 yuan/mt lower than the monthly futures contract price.

• CCI 5000 was 536 yuan/mt, 78 yuan/mt lower than the monthly futures contract price.

• CCI 4500 was 469 yuan/mt, 83 yuan/mt lower than the monthly futures contract price.

The capacity of operating coal mines expanded significantly, and a net increase is still expected by 2025.

• New capacity added in China in 2024: 85.9 million mt/year (thermal coal: 64.8 million mt/year, coking coal: 21.1 million mt/year).

• Capacity eliminated in China in 2024: 17.8 million mt/year (thermal coal: 12.3 million mt/year, coking coal: 5.6 million mt/year).

• It is expected that China will add 100 million mt/year of capacity in 2025, including 77 million mt/year of thermal coal.

• It is expected that China will eliminate 24 million mt/year of capacity in 2025, including 18 million mt/year of thermal coal.

Coal production in 2025 will grow mildly, but demand will constrain the growth rate.

► Raw coal production:

• Increased production in Xinjiang and Inner Mongolia offset production cuts in Shanxi. China's raw coal production improved MoM, reaching 4.78 billion mt in 2024, up 1.5% YoY.

• Shanxi's production has returned to normal in 2025. China's raw coal production is expected to increase by 0.7% YoY, reaching 4.813 billion mt in 2025.

• Raw coal production in January-April 2025 increased by 6.6% YoY.

• The recovery of Shanxi's supply is expected to drive an overall increase in production.

• Declining coal demand will constrain production growth.

• Production in 2025 is expected to increase by 0.7% YoY.

Production will grow mildly in 2025, but growth will be constrained by demand.

Keynote Speech: Regional Coal Market Outlook: India

Presenter: Vasudev Pamnani, Director of I-Energy Natural Resources.

01 Background of India's Coal Industry.

India's coal mining history dates back over 250 years, originating in the eastern region.

• India has 378.21 billion mt of coal reserves, making it one of the world's largest coal reserve holders.

• In 2024, India ranked second globally in coal consumption (1.3 billion mt), production (1.04 billion mt), and imports (268 million mt).

• This momentum largely continued in the first four months of early 2025, with coal consumption reaching 492 million mt.

• Domestic coal production during the same period reached 403 million mt, a 3% increase compared to the same period last year.

• In contrast, import trends weakened, dropping to 88 million mt from January to April 2025, a 5% decrease from 93 million mt in the same period last year.

• The main challenges facing India's imports are the increase in domestic production and supply, high inventories at power plants, mines, and ports, as well as the adverse impacts of weak global demand and global trade tensions.

• The international market is also under pressure, with coal demand cooling in early 2025 due to macroeconomic instability.

• Despite coal prices falling to multi-year lows, demand remained sluggish during India's summer peak electricity usage period.

• The market remains fragile, but this is not the end of India's coal era.

• Coal remains the backbone of India's power sector and will continue to be an important component of the country's energy framework in 2025.

02 India's Coal Demand

Total Coal Demand in India (million mt)

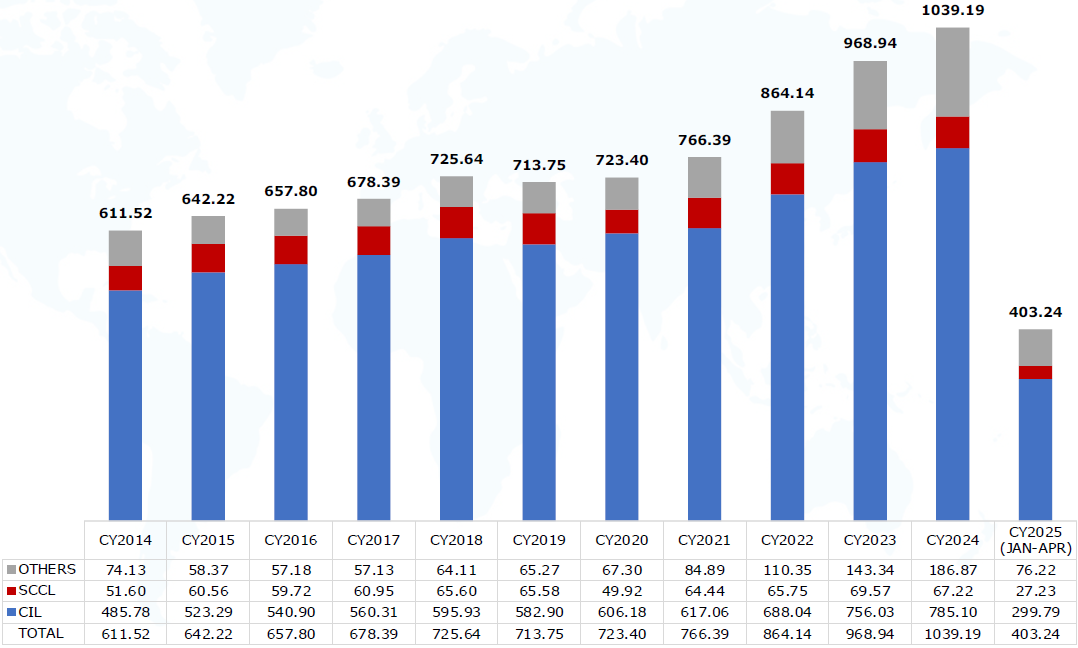

03 Domestic Coal Production in India

Coal Production in India (million mt)

In addition, the speaker also elaborated on perspectives such as coal dispatched from India to industries, drivers of coal demand in India, and "Black Diamond: Coal Supports India's Power System."

Keynote Speech Topic: The Cost of Geopolitical Security - A study of methanol Plant in Indonesia

Speaker: Ghee Peh, Energy Finance Expert at the Institute for Energy Economics and Financial Analysis (IEEFA)

Coal and Energy Security: What's the Cost?

• On April 2, 2025, US President Trump announced tariffs on all ASEAN countries: 32% for Indonesia, 46% for Vietnam, 36% for Thailand, and 24% for Malaysia.

• As globalization trends weaken, domestic energy security in Indonesia has become crucial. For Indonesia, whether to consider downstream coal products such as dimethyl ether (DME) as an option for energy security is a question worth exploring.

The DME project is costly, with a total investment of US$3.1 billion.

Indonesian President Prabowo Subianto has instructed an energy task force to restart coal gasification projects for dimethyl ether (DME) in four regions of Sumatra and Kalimantan. The plan aims to reduce imports of liquefied petroleum gas (LPG) by processing low-calorific coal.

According to estimates by the Institute for Energy Economics and Financial Analysis (IEEFA), a 1.4 million mt DME plant in Sumatra would cost US$2.6 billion, plus an opportunity cost loss of US$520 million over a decade, totaling US$3.1 billion.

Economic Feasibility in Question

The capital expenditure and opportunity cost of Indonesia's DME plants would account for 70% of the total annual cost of LPG imports (US$4.3 billion), yet would only produce energy equivalent to 1 million mt of LPG. The cost per unit of energy for consumers would be 42% higher than that of LPG.

A 1.4 million mt DME plant could offset 15% of Indonesia's LPG imports, but its economic feasibility is uncertain. For example, the Shanxi Lanhua Group in China halted its DME project in 2023 due to unprofitability, which serves as evidence.

Cost Comparison

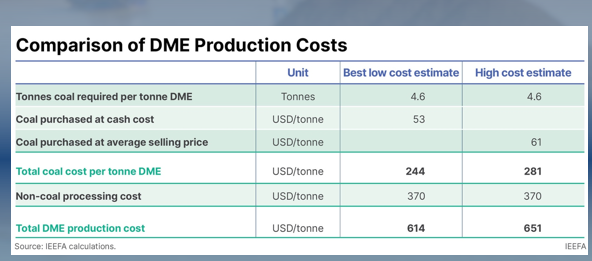

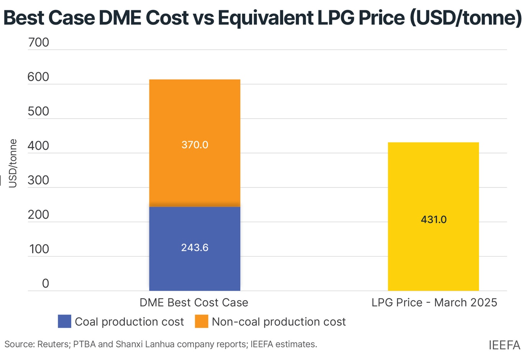

The cost of producing one ton of DME using 4.6 mt of coal can be calculated based on spot costs or average selling prices:

If calculated based on average selling prices, the cost of producing one ton of DME is US$281. If calculated based on cash costs, the coal cost per ton of DME is US$244, which is US$37 lower than the selling price calculation method.

Considering both coal and non-coal costs, the estimated production cost of DME isUS$614-651 per mt. Taking into account the lower energy content of DME, when converted to an equivalent LPG price, it isUS$431 per mt.

Panel Discussion: The Role of Coal in the Energy Transition Process of Asian Countries

Moderator: Laode M Syarif, Dr. from Faculty of Law, Hasanuddin University

Panelists: Subhashish Datta, Chief Financial Officer of Kaltim Prima Coal

Lloyd Hain, Chairman of Research at AME Mineral Economics Pty Ltd, a subsidiary of AME Group

Putra Adhiguna, Managing Director of Energy Shift Institute

Jeffrey Mulyono, Director of DVK Resources Pte Ltd Singapore

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)