SMM, ngày 26 tháng 5 năm 2025:

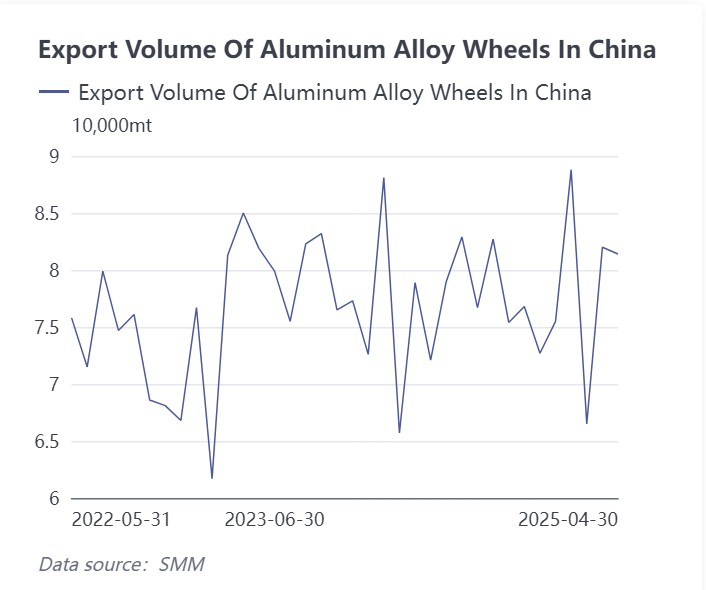

Theo số liệu hải quan, Trung Quốc đã xuất khẩu tổng cộng 81.400 tấn mâm bánh xe hợp kim nhôm trong tháng 4 năm 2025, tương đương so với 82.000 tấn của tháng 3, thể hiện sự ổn định chung và tăng 13% so với cùng kỳ năm ngoái. Hiệu suất xuất khẩu mâm bánh xe nhôm trong nước trong tháng 4 vẫn mạnh mẽ, với kết quả vượt kỳ vọng thu hút sự chú ý của thị trường. Kể từ khi Mỹ phát động cuộc chiến thuế quan vào đầu tháng 4, ngành công nghiệp mâm bánh xe nhôm, vốn đã trực tiếp xuất khẩu hơn 30% sản phẩm sang Mỹ trong những năm gần đây, được dự đoán sẽ là "ngành bị ảnh hưởng đầu tiên", và thị trường có triển vọng tương đối bi quan về xuất khẩu của ngành này. Tuy nhiên, số liệu xuất khẩu mâm bánh xe nhôm trong tháng 4 lại "bình lặng", hoặc thậm chí "yên ắng", vượt quá kỳ vọng của hầu hết các nhà đầu tư trên thị trường. Vậy, những bí mật nào đằng sau số liệu này đáng được chúng ta chú ý? Các doanh nghiệp lớn trong chuỗi ngành công nghiệp mâm bánh xe nhôm nhìn nhận số liệu này như thế nào? Sau khi tiến hành khảo sát thị trường mâm bánh xe nhôm, SMM đã tổng hợp những phản hồi sau đây:

Phản hồi từ Nhà sản xuất A mâm bánh xe nhôm: Tác động đến xuất khẩu có thể bị trì hoãn, và số liệu của hai tháng liên tiếp là tháng 5 và tháng 6 có thể phản ánh tốt hơn tình hình thực tế.

Phản hồi từ Nhà sản xuất B A356: 50% khách hàng của chúng tôi xuất khẩu sang Nhật Bản, và đơn hàng xuất khẩu của họ đang diễn ra tốt đẹp, trong khi nhu cầu trong nước trong phân khúc này tương đối yếu.

Phản hồi từ Nhà sản xuất C mâm bánh xe nhôm: Chúng tôi đã đàm phán với khách hàng nước ngoài từ tháng 4, nhưng do 70% sản lượng mâm bánh xe hợp kim nhôm toàn cầu được sản xuất tại Trung Quốc, nên khách hàng nước ngoài khó có thể tìm thấy sự thay thế đầy đủ. Do đó, tác động đến số liệu xuất khẩu trong tháng 4 có vẻ hạn chế. Đồng thời, do năng lực sản xuất trong nước của công ty chúng tôi có hạn, khối lượng xuất khẩu trực tiếp sang Mỹ chỉ chiếm một phần tương đối nhỏ trong hoạt động kinh doanh của nhà máy Trung Quốc, và không có sự vội vàng trong xuất khẩu. Chúng tôi có một nhà máy ở Mexico có thể giảm thiểu một số rủi ro thương mại quốc tế. Hiện tại, chúng tôi đã liên tục nhập khẩu nguyên liệu để sản xuất, với sản lượng sản xuất tăng nhẹ gần đây.

Phản hồi từ Doanh nghiệp Xuất khẩu D hạ nguồn: Có nhu cầu mua hàng trước thời điểm từ khách hàng trong mùa thấp điểm truyền thống từ tháng 6 đến tháng 8. Đồng thời, sự mất giá của đồng đô la Mỹ trong tháng 4, cùng với sự giảm giá của giá nhôm LME, đã tạo ra một cơ hội tạm thời để có lợi thế về giá xuất khẩu, trùng hợp với sự cạnh tranh gia tăng trên thị trường trong nước, buộc các doanh nghiệp phải tăng cường nỗ lực khám phá thị trường nước ngoài.

Nhiều doanh nghiệp liên quan nói chung báo cáo rằng sản xuất đã diễn ra bình thường gần đây, với khả năng phục hồi của người tiêu dùng vẫn duy trì, và không có sự thay đổi đáng kể trong nhịp độ sản xuất ngắn hạn.

Nghiên cứu thị trường nhôm của SMM chỉ ra những thay đổi sau đây trong phân bố các quốc gia mục tiêu xuất khẩu mâm bánh xe nhôm của Trung Quốc trong tháng 4, đáng được thị trường chú ý:

1. Bị ảnh hưởng bởi việc tăng thuế, xuất khẩu mâm bánh xe nhôm trực tiếp sang Mỹ trong tháng 4 đã giảm 5.200 tấn, giảm 18,3% so với tháng trước, nhưng tăng nhẹ 1,8% so với cùng kỳ năm ngoái. Đồng thời, tỷ lệ xuất khẩu sang Mỹ giảm xuống dưới ngưỡng 30%, đây là một trường hợp hiếm gặp.

2. Tháng 4, lượng xuất khẩu sang Mexico lần đầu tiên trong năm nay vượt 10.000 tấn, tăng 22,7% so với tháng trước và tăng đáng kể 44% so với cùng kỳ năm ngoái, thể hiện những đặc điểm đáng chú ý của thương mại tái xuất khẩu.

3. Lượng xuất khẩu sang Morocco lần đầu tiên lọt vào top 10, chỉ xếp sau 5 nước hàng đầu là Mỹ, Nhật Bản, Mexico, Hàn Quốc và Thái Lan. Nguyên nhân đằng sau điều này đáng được chú ý. SMM dự đoán rằng điều này có thể liên quan đến việc một số doanh nghiệp sản xuất bánh xe nhôm trong nước thành lập nhà máy ở Morocco.

Theo góc độ phân tích của SMM, sau khi Mỹ tăng thuế vào tháng 4/2025, lượng xuất khẩu mâm bánh xe hợp kim nhôm của Trung Quốc đã thể hiện khả năng phục hồi mạnh mẽ, với tác động tiêu cực ít nghiêm trọng hơn dự kiến. Dữ liệu hải quan cho thấy lượng xuất khẩu vẫn ổn định trong tháng 4, chủ yếu là do lợi thế chuỗi cung ứng cứng nhắc xuất phát từ việc 70% công suất toàn cầu tập trung ở Trung Quốc, cùng với việc các doanh nghiệp hàng đầu chủ động thành lập công suất sản xuất ở nước ngoài tại Mexico, Thái Lan, Morocco và các địa điểm khác. Điều này không chỉ đáp ứng các đơn hàng mới ở nước ngoài mà còn giảm sự phụ thuộc vào xuất khẩu trực tiếp sang Mỹ (với tỷ lệ hiện tại giảm đáng kể). Do đó, không có sự tăng vọt xuất khẩu thường thấy trong các xung đột thương mại truyền thống trong ngắn hạn. Những thành công ban đầu đã đạt được trong điều chỉnh cơ cấu của ngành, nhưng cần tiếp tục theo dõi tiến độ tăng công suất ở nước ngoài và khả năng chuyển giá cao hơn sang các thị trường tiêu thụ cuối cùng.

Tuy nhiên, cần lưu ý rằng sự hạn chế kép của đà tăng trưởng kinh tế toàn cầu suy yếu và chủ nghĩa bảo hộ thương mại gia tăng đã khiến các nhà mua ở nước ngoài thường áp dụng chiến lược duy trì tồn kho thành phẩm ở mức thấp, khiến khó có thể thấy nhu cầu bổ sung hàng tồn kho quy mô lớn trong ngắn hạn. Đáng chú ý là các thị trường xuất khẩu lớn sắp bước vào chu kỳ điều chỉnh chính sách thuế quan. Cùng với tuyên bố chung được đưa ra trong cuộc đàm phán kinh tế và thương mại Trung - Mỹ tại Geneva vào ngày 12 tháng 5 năm 2025, trong đó mức thuế quan giữa hai bên đã giảm đáng kể, Mỹ đã hủy bỏ tổng cộng 91% thuế quan áp dụng và tạm ngừng thực hiện 24% thuế quan đối ứng trong giai đoạn 90 ngày ban đầu. SMM sẽ tiếp tục theo dõi thời điểm và cường độ thực hiện điều chỉnh chính sách thuế quan ở các nước xuất khẩu lớn. SMM dự đoán rằng xuất khẩu bánh xe nhôm của Trung Quốc có thể giảm tổng thể trong hai tháng tới, với xuất khẩu bánh xe nhôm bước vào giai đoạn điều chỉnh trong nửa cuối năm. Giai đoạn khó khăn của ngành có thể kéo dài cho đến khi hệ thống thuế quan mới rõ ràng hơn.

![Gió ngược vĩ mô đè nặng lên giá nhôm, xu hướng hạ nhiệt cung cầu alumina tiếp diễn [SMM Aluminum Futures Brief]](https://imgqn.smm.cn/usercenter/kxYyQ20251217171651.jpg)