SMM April 9 News,

Overview: In Q1 2025, domestic crude stainless steel production decreased by 2.8% compared to Q4 2024, but increased by 10.6% YoY, with ample supply. Supported by costs, stainless steel prices rose.

During the Chinese New Year holiday in Q1 2025, crude stainless steel production remained at a high level from January to March, with March production reaching a record high of 3.58 million mt. Domestic demand diverged: new construction starts in the real estate sector declined YoY, dragging down stainless steel demand; retail sales growth of home appliances slowed, indicating insufficient demand momentum. However, expectations for policy stimulus, such as increased trade-in subsidies, may marginally improve domestic demand. Overseas markets were affected by the EU's carbon tariff hikes and anti-dumping duties in Asian markets, leading to a YoY decline in exports. The US tariff hike also impacted exports.

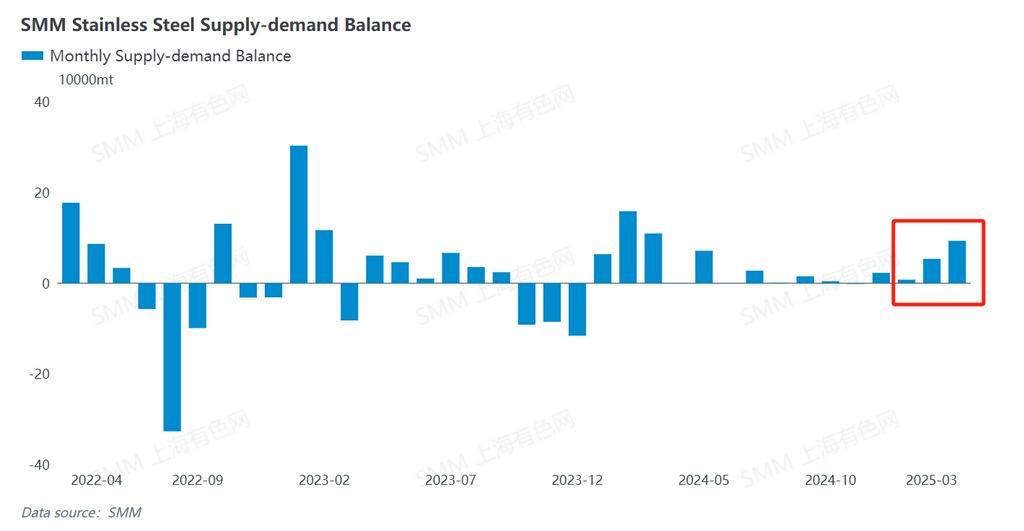

The supply-demand balance for stainless steel remained in surplus, with ample supply: Q1 2025 production increased by 10.6% YoY; demand, affected by the Chinese New Year holiday, still maintained a high growth rate, increasing by 10.8% YoY. In terms of supply-demand balance, a surplus of 155,000 mt was formed, a significant decrease from the 333,000 mt in Q1 2024.

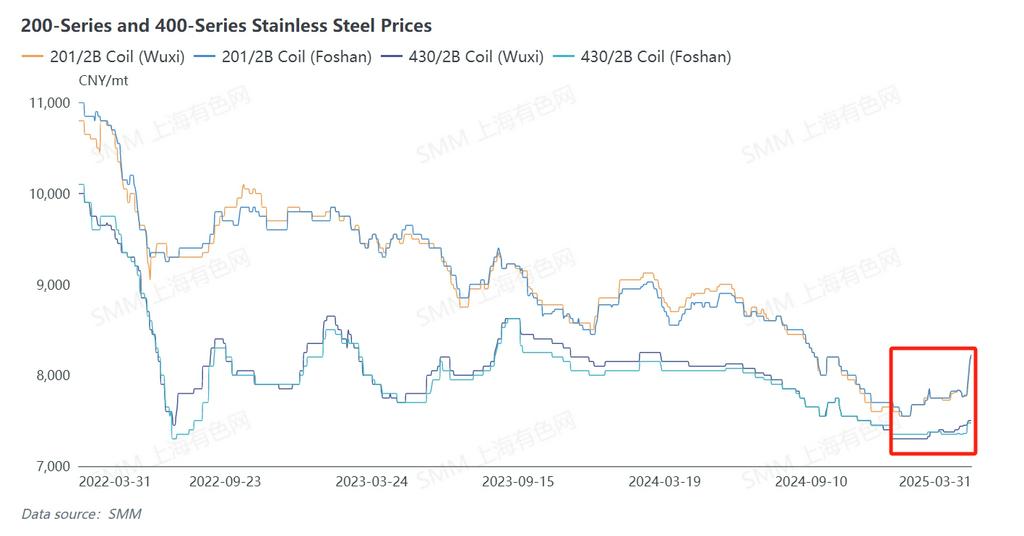

In Q1 2025, the stainless steel market exhibited a complex situation. Supported by costs, stainless steel prices hit bottom and then rebounded slightly, with overall fluctuations driven by raw material volatility. Changes in spot prices were transmitted to the futures market, with stainless steel futures closely following the upward trend of spot prices. On the demand side, performance in Q1 was relatively good, with downstream industries maintaining normal just-in-time procurement. However, prices of various stainless steel series in Q1 2025 were lower than those in the same period of Q1 2024, resulting in losses, though this phenomenon eased somewhat in March. The price recovery gradually narrowed the losses of stainless steel producers.

The most-traded stainless steel futures contract showed a fluctuating upward trend in Q1 2025, influenced by unstable macroeconomic expectations and raw material price volatility, with futures prices continuing to fluctuate while trending upward. Particularly in March, as market confidence in economic recovery strengthened, capital flowed into the futures market, pushing the price center gradually higher. After reaching a quarterly high in mid-to-late March, prices pulled back slightly and consolidated. Downstream demand in the spot market was mediocre, with cautious buyer sentiment limiting the upward momentum of futures prices.

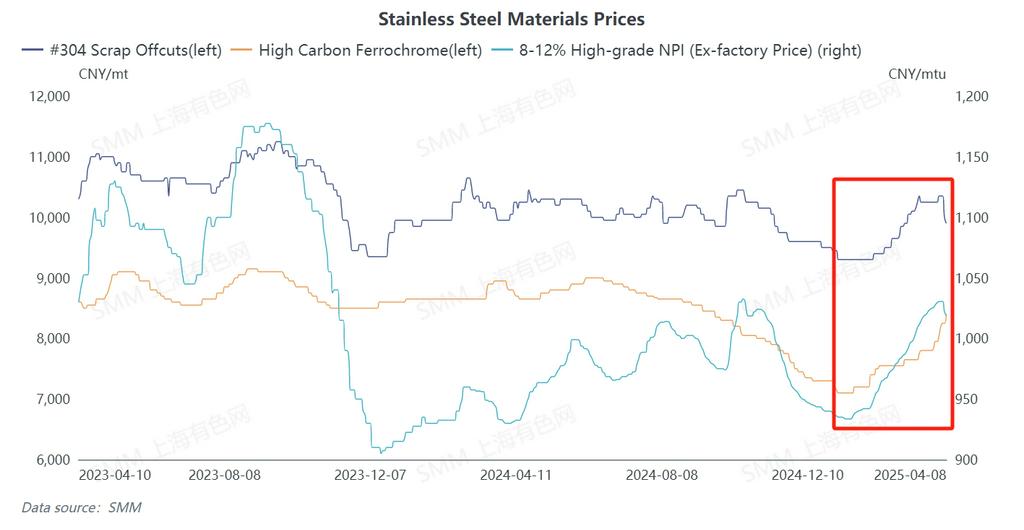

Stainless steel raw material prices trended upward in Q1 2025. Prices of raw materials such as nickel iron, ferrochrome, and stainless steel scrap rose, driving up the production costs of stainless steel.

On the nickel iron front, in Q1 2025, Indonesia's production growth slowed due to the rainy season and policy factors. Meanwhile, nickel ore from the Philippines failed to provide effective supplementation due to the rainy season, resulting in a tight overall supply of nickel iron. With stainless steel mills resuming production after the holiday, the demand for nickel iron procurement increased. Under the supply-demand imbalance, nickel iron prices rose. High-carbon ferrochrome prices remained relatively firm, staying at a high level. The main reason was the rapid and significant increase in the prices of key raw materials such as chrome ore, which strongly pushed up high-carbon ferrochrome prices. In terms of stainless steel scrap, overall prices strengthened in Q1 2025, with its economic efficiency somewhat weakened.

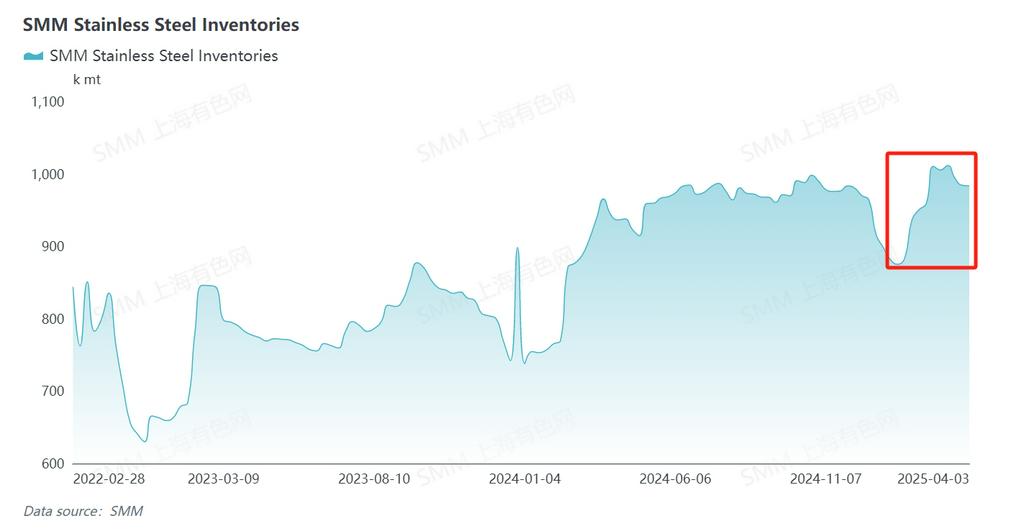

In terms of stainless steel inventory, both social inventory and in-plant inventory experienced changes.

Stainless steel social inventory: In Q1 2025, the social inventory of stainless steel first decreased and then increased. In the early stage, downstream demand was released after the Chinese New Year holiday, consuming inventory. In the later stage, the resumption of production by steel mills led to an increase in production, with new resources flooding the market. However, demand failed to keep pace, making it difficult to digest the new supply, resulting in inventory accumulation.

Stainless steel in-plant inventory: The in-plant inventory of stainless steel fluctuated overall in Q1. The inventory level of the 200-series fluctuated in Q1, with the inventory-to-sales ratio changing from the early stage to the end of Q1, reflecting continuous adjustments in its production and sales rhythm. As the main category, the 300-series saw fluctuations in both inventory and inventory-to-sales ratio in Q1. Taking production data as an example, the crude steel production of the 300-series increased by 15.6% YoY to 1.956 million mt, with the increase in production affecting in-plant inventory. The in-plant inventory of the 400-series gradually rose, with a significant increase at the end of March, and the inventory-to-sales ratio also changed accordingly by the end of Q1.

The performance of both social inventory and in-plant inventory collectively reflected a supply-strong-demand-weak pattern in the stainless steel market in Q1 2025.

In Q2 2025, the ongoing tariff issue significantly impacted the stainless steel market. Market sentiment was dominated by negative emotions among stainless steel producers and downstream enterprises. This sentiment was reflected in the price trend, with stainless steel prices initially fluctuating downward. As the market gradually digested the impact of tariffs, prices were expected to stabilize and then fluctuate within a certain range.

On the export front, the export of stainless steel products, aluminum products, and downstream products was hindered. The US imposed a 25% tariff on imported steel and aluminum products starting from March 12, 2025, covering products such as cold-rolled stainless steel sheets. The tariff was gradually increased from 25% to 45%, and with the addition of anti-dumping and countervailing duties, the actual tax rate for some products exceeded 100%. Meanwhile, the US also imposed tariffs of 32-46% on transshipment countries, cutting off some transshipment channels. Although the direct export of stainless steel from China to the US was limited, the stainless steel products sector was significantly impacted. For example, domestic stainless steel kitchenware exports to the US accounted for about 20% of the export channels, and export enterprises faced challenges such as profit compression and order loss.

However, the main demand for stainless steel is domestic. If domestic demand increases, it will effectively improve the bearish sentiment in the market caused by the tariff issue. On one hand, the growth in domestic demand can absorb some of the surplus capacity, alleviating supply pressure. On the other hand, it can also enhance market confidence and stabilize price expectations.

For any inquiries regarding stainless steel, please contact Yang Chaoxing at 021-20707860 or 13585549799 (same number for WeChat).

> Click to view the SMM Stainless Steel Database

![[SMM Nickel Midday Commentary] On March 26, influenced by expectations surrounding the policy of “Indonesia's proposed levy of a nickel export tax,” nickel prices rose significantly](https://imgqn.smm.cn/usercenter/CjEnN20251217171733.jpg)