According to SMM statistics, although the overall growth rate of the energy storage market in 2023 is not good as expected, the overall market growth rate is still relatively fast. In 2023, global ESS LFP cell production reached 190GWh, a YoY increase of 48% compared to 2022; global ESS LFP cell shipment volume reached 195GWh, a YoY increase of 49% compared to 2022.

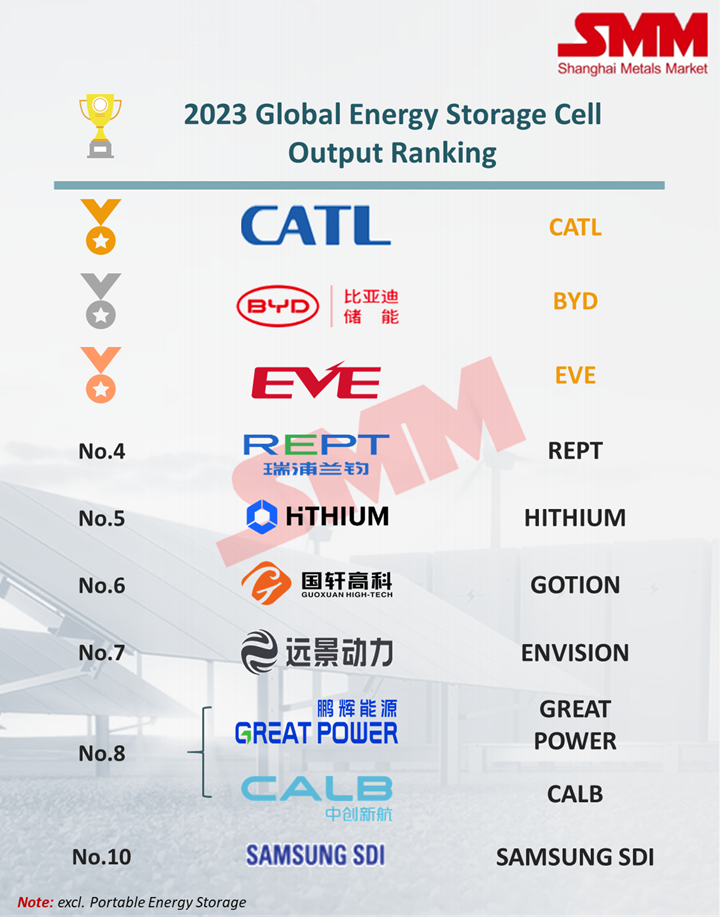

Overall, many new players entered the energy storage market in 2023, but the market competition pattern of the leading players has not changed significantly. From the perspective of market share, CR5's market share is as high as 75%, and market concentration is still increasing.

Among them, CATL is firmly in the lead, with total shipments exceeding 65GWh, ranking first in a row. BYD and EVE both shipped more than 20GWh to maintain their market share advantage as before.

REPT and Hithium won the 4th and 5th places. REPT still maintains a high market share in the energy storage field, while Hithium made rapid progress in 2023 and squeezed into the top five ranks.

In terms of market segments, the large scale ESS market shipped more than 155gwh. Overall, the market is still concentrated at the leading players, but in the process of switching cells from 280Ah into 314Ah, there may be a new wave of reshuffle.

The resential ESS market has been full of twists and turns in 2023 with the high growth expectations at the beginning of the year led to high inventories, and then rsperienced a rapid decline in market enthusiasm. However, the European energy crisis caused by the Red Sea War has a hidden trend of re-erupting. It is expected that the resential ESS market may improve in 2024.

![[Lithium Battery: New Ultra-Fast Charging Battery Industrialization Project To Be Launched In Zaozhuang, Shandong]](https://imgqn.smm.cn/usercenter/aXRJI20251217171728.jpg)

![[SMM Analysis] Analysis of Production and Sales of Selected Listed Lithium Battery Enterprises in China in 2025](https://imgqn.smm.cn/usercenter/WgbTp20251217171727.jpg)