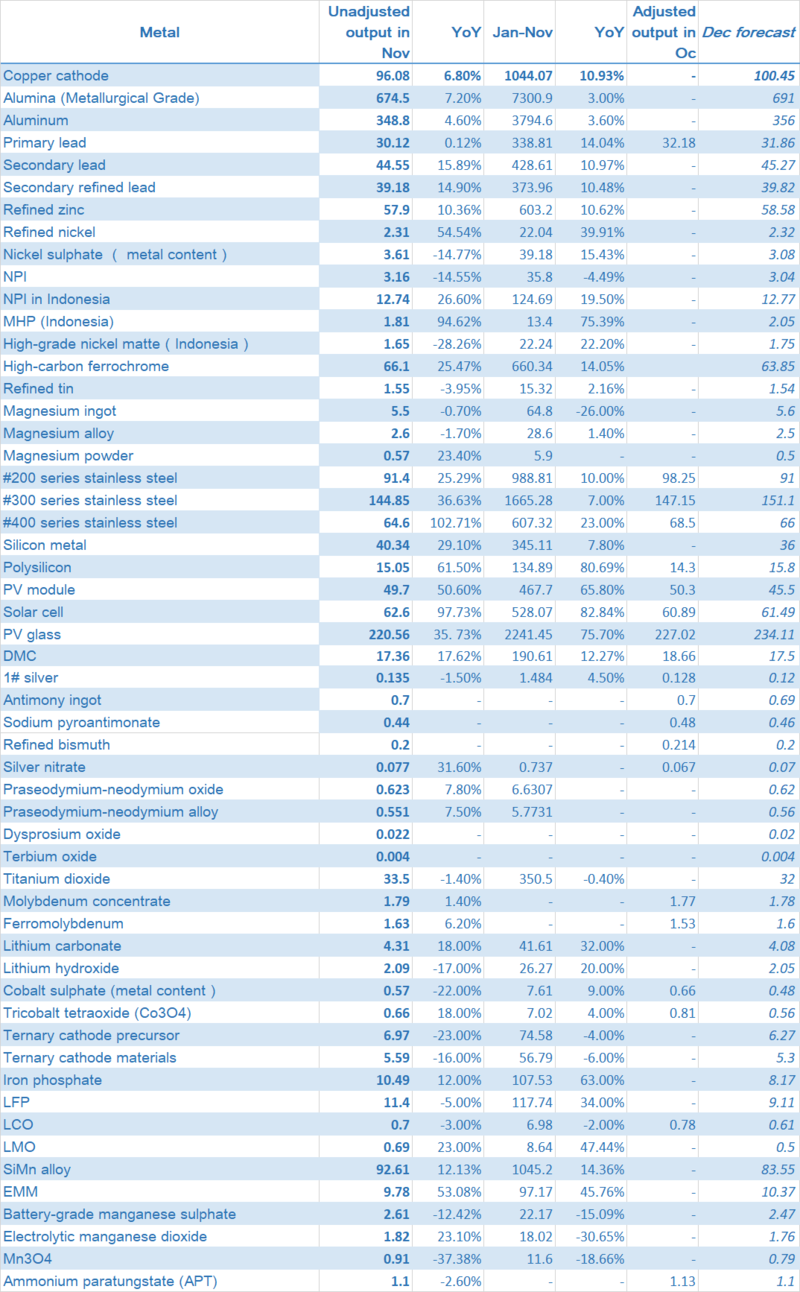

Copper cathode

China's copper cathode output in November was 960,800 mt, a decrease of 33,000 mt or 3.3% month-on-month, but a growth of 6.8% year-on-year, according to SMM data. The output was 40,400 mt lower than the expected 1 million mt. The output totalled 10.44 million mt from January to November, an increase of 1.03 million mt or 10.93% year-on-year.

Three smelters undertook planned maintenance in November, and one smelter reduced production due to equipment damage. A smelter began technological upgrading, and output at some smelters fell due to tight supply of blister copper. Those unfavourable factors resulted in sharp declines in the output in November. In addition, the output of newly-commissioned smelters was slower than expected, limiting new production, which was also one of the reasons why total production failed to increase. We believe that the average operating rate of copper cathode industry fell 3.41 percentage points month on month to 88.92% in November.

In December, according to SMM statistics, only one smelter has overhaul plan. In addition, the smelters that were overhauled in November will resume production. Many smelters reported that the supply of blister copper in December was better than that in November. Total production in December will increase compared with November. However, several newly-commissioned smelters were unable to produce copper cathode, and it is estimated that they will not be able to produce output until January, which will result in lower-than-expected output in December. Domestic copper cathode output is estimated at 1 million mt in December, up 43,700 mt or 4.55% month-on-month and 15.5% year-on-year, according to the current production schedules. The accumulated output from January to December is expected to stand at 11.45 million mt, an increase of 11.31% or 1.16 million mt year on year.

Aluminum

SMM reports China's November aluminum output at 3.488 million mt, up 4.6% YoY. Yunnan's shutdowns cut domestic daily output by 1,185 mt to 116,300. January-November total reached 37.946 million mt, up 3.6% YoY. November saw minor shifts in China's aluminum billet production. Yunnan's cuts mainly hit ingot output, key for the processing sector. SMM notes the molten aluminum’s share rose 3 points to 73.4% MoM. November's domestic aluminum cast ingot volume was around 928,000 mt, down 10% YoY, and January-November total was about 11.138 million mt, down 10.4% YoY.

Capacity Changes: November saw a drop in China's aluminum operating capacity, mainly from major cuts in Yunnan due to power shortages. The province saw an annualized cut of 1.17 million mt, reducing local operating capacity from 5.65 million mt to about 4.48 million mt. Currently, Yunnan's aluminum operating capacity has increased by about 440,000 mt YoY. In November, Inner Mongolia's Baiyinhua started new capacity, adding about 80,000 mt in operating capacity, with another 120,000 mt to be powered soon, aiming for full production by December's end. Other regions' aluminum capacities remained stable with no major changes.

SMM states that as of November, China's aluminum installed capacity is about 45.19 million mt, operating capacity is around 41.89 million mt, and industry operating rates have dropped 2.4% MoM to 92.7%.

Forecast: December may see slight new domestic capacity. Yunnan's current operating capacity is above its historical average, with uncertain power supply. Other regions should remain stable. Short-term, domestic aluminum capacity is expected to stay steady, but watch the southwest's power situation.

SMM predicts December's aluminum output at 3.56 million mt over 31 days, up 3.5% YoY, with 2023's total expected at 41.5 million mt, up 3.6% YoY.

Alumina

SMM shows November's China metallurgical-grade alumina production at 6.745 million mt over 30 days, daily average up by 4,100 mt to 224,800 mt. Production fell 1.4% from October but rose 7.2% YoY. End of November, installed capacity of alumina was at 100 million mt, operating capacity at 82.07 million mt, with operating rates at 82.1%. January-November total alumina output was 730.09 million mt, up 3.0% YoY.

Regional data shows Shanxi's November operating rates at 78.4%, up 3.4% YoY. This rise is due to a second production line restart in Shanxi's factories, adding 350,000 mt annual capacity, and some factories upping output for profit, boosting operating rates.

In the Henan region, the province-wide operating rates stood at 63.5% in November, down 2.2% MoM. This decline was primarily due to certain alumina refineries in the Sanmenxia area maintaining reduced production since October because of tight ore supply. According to SMM research, mines in the Sanmenxia area are still halted with no short-term expectations for resumption of production.

In Guizhou, alumina refineries faced ore supply and cost issues, keeping November operating rates at 82.4%. Hebei saw rates drop to 81.3%, down 7% MoM, mainly because a major enterprise underwent maintenance due to a steam shortage from equipment failure at its power plant, impacting 2.4 million mt annual capacity. Normal production is expected to resume soon.

Guangxi's operating rates fell from 86.9% to 85.4% due to maintenance at a local refinery affecting 300,000 mt annual capacity, but it resumed normal production by late November, causing only a slight monthly decline. Shandong's operating rates recovered from 88.8% to 93.5% in November, despite a major refinery's furnace maintenance impacting 1 million mt of annual capacity, scheduled from November 28 to December 10.

December forecast: Hebei is expected to regain some capacity post-maintenance. In Henan's Sanmenxia, mines aren't set to reopen soon, with ore shortages likely to keep some capacity constrained and operating rates low. A major Shandong alumina refinery undergoing maintenance aims to restart early December. In Guangxi, refineries that reduced output in November due to ore shortages aren't expected to full production capacity in the short term.

As year-end nears, northern regions may face pollution, possibly prompting more production limits. Thus, SMM predicts December's daily production at about 223,000 mt, with total operating capacity around 81.5 million mt, up 6.6% YoY.

Primary lead

In November 2023, the domestic output of refined lead was 301,200 mt, a drop of 6.42% month-on-month but up 0.12% year-on-year. The cumulative output from January to November 2023 increased by 14.04% year-on-year. Total production capacities of enterprises in the survey totalled 5.84 million mt in 2023.

According to survey, refined lead production dropped by over 20,000 mt in November, which was the largest monthly drop in refined lead in the past five months. The main reason for the decline in output is that some lead smelters in Henan, Yunnan, Hunan and other places began maintenance, and most of them are medium-to-large-scale producers of delivery brands, which caused large fluctuations in output. Yunnan implemented power rationing in November due to the low-water season. At the same time, the escalation of the war in Myanmar led to the temporary closure of some gateways in Yunnan. The reduction in border trade of lead concentrates led to tight supply. These also led to the decline in the output of refined lead companies.

The refined lead smelters that were overhauled in November plan to resume operations in December, which will bring about a month-on-month increase in refined lead output of over 10,000 mt. Medium and large smelters in Henan, Yunnan, Hunan, Jiangxi and other regions restored after maintenance, which will lead to increase in refined lead output. On the other hand, tight supply of lead concentrate and the continued weakening of lead prices have reduced the production enthusiasm of some lead smelters, resulting in the possibility of output reductions. The conflict in northern Myanmar has continued to escalate recently, and some gateways in Yunnan are still closed. There are limitations in border trade of lead concentrate, which has tightened regional supply. In addition, lead smelters in Qinghai plan to upgrade the equipment of the lead smelting system from December 25 to increase the production capacity of lead ingots. During the technical transformation period (the first half of 2024), production will be suspended for half a year. SMM will track the actual production changes.

Secondary lead

The output of secondary lead in November 2023 was 445,500 mt, a decrease of 6.43% from October and up 15.89% year on year; the cumulative output of secondary lead from January to November 2023 was 4.29 million mt, an increase of 10.97% year on year. In November 2023, the output of secondary refined lead was 391,800 mt, a decrease of 6.47% from October, and a growth of 14.9% year on year; from January to November 2023, the cumulative output of secondary refined lead was 3.74 million mt, an increase of 10.48% year on year.

According to survey, secondary lead production dropped by over 30,000 mt in November, which was the largest monthly decline in nearly nine months. There are four main reasons for the decline in production: First, the supply of battery scrap was tight and this limited output; second, losses at smelters from high costs and significant declines in lead prices were not motivated to produce; third, some medium and large smelters shut down for maintenance due to the price factor during the month, which affected about 10 days of output; fourth, the air quality in the heating season in the north was poor, and environmental protection controls caused some smelters to reduce production.

In December, market pessimism is still strong, and the price of battery scrap has a crucial impact on the trend of lead prices and the production of secondary lead smelters. Some smelters said that if the subsequent shipments arrivals of battery scrap can still meet production needs without price rising, they will maintain normal production in December; if the subsequent supply of battery scrap remains tight and lead prices remain weak, they may shut down for maintenance against severe losses. In addition, companies whose output fell due to maintenance in November are expected to return to normal in December. SMM expects the output of secondary refined lead to increase slightly by 6,000 mt in December. Raw material supply and prices may have an impact on actual production.

Refined zinc

In November 2023, China's refined zinc output was 579,000 mt, a decrease of 25,600 mt or 4.23% month on month, but a year on year increase of 10.62%, below our expectations. The output totalled around 6.03 million mt from January to November, up 10.62% year-on-year. Domestic zinc alloy output was 93,300 mt in November, 4,800 mt lower than in the previous month.

Smelters in Shaanxi, Hunan and Yunnan stopped production and overhauled, resulting in significant output reductions. In addition, the output of some smelters in Inner Mongolia, Shaanxi, Yunnan, Guangdong and other places also decreased. Smelters in Sichuan increased production and Smelters in Gansu ended maintenance, growing output.

SMM predicts that domestic refined zinc production will increase by 6,800 mt month-on-month to 585,800 mt in December 2023, a year-on-year increase of 11.41%; the cumulative output from January to December 2023 will reach 6.617 million mt, a year-on-year increase of 10.69%; the release of new production capacity in Guangxi, and the production resumption from maintenance at smelters in Hunan, Yunnan will increase the total output. The output of smelters in Shaanxi will continue to decline. The overall output increase will not be obvious.

Refined Tin

SMM reports November's domestic refined tin output at 15,560 mt, up 0.24% MoM but down 3.95% YoY. January-November total reached 153,253 mt, up 2.16% YoY. Production was stable; minor output fluctuations in Yunnan were due to production plan adjustments and maintenance, while a Jiangxi smelter cut production due to high costs and tight scrap supply.

In November, an Inner Mongolia smelter slightly cut output following production plan adjustments. A Guangdong smelter also reduced its operating rates due to a scrap tin shortage. Most other smelters kept production stable during the month.

Heading into December, Yunnan smelters have stable plans, with refined tin output likely steady. A Jiangxi smelter that cut production in November expects to continue this trend. Another Jiangxi smelter plans a year-end halt for maintenance, potentially decreasing December's refined tin output. An Anhui smelter resuming post-maintenance is set to hit prior output levels in December. A Hubei smelter, paused since late October due to scrap shortages, will remain so until post-Spring Festival. Most others should keep production normal. December's domestic tin ingot production is projected at 15,445 mt, down 0.74% MoM but up 2.69% YoY.

Refined Nickel

November 2023 saw national refined nickel output in China at 23,000 mt, down 3.9% MoM but up 54.45% YoY, marking the year's first production drop. The decline since October is due to falling nickel prices, which squeezed profits for electrodeposited nickel producers using external raw materials, leading to losses by late October as prices fell to around 123,000 yuan/mt. This price is close to the production costs of some vertically integrated producers. Moreover, spot prices for nickel raw materials didn't fall as fast as nickel futures, causing some enterprises to cut production due to cost pressures.

December 2023's estimated national refined nickel output is 23,200 mt, slightly up from November. Nickel prices show recovery signs after recent lows. Raw material supply may rise, while downstream demand will remain weak.

China NPI

November 2023's national NPI production in China was 31,600 mt in nickel content and 765,700 mt in physical content, with volume in physical content down 2.87% MoM and volume in nickel content down 6.35% YoY, matching the anticipated reduction in domestic NPI output.

SMM research shows August's nickel ore price hike impacted domestic NPI plants, some holding costly ore reserves, thus increasing losses as NPI prices fell. Smelters now operate at 8-20% losses, leading some to cut production or shut down for maintenance.

December 2023's projected national NPI output is about 30,400 mt in nickel content, down 3.72% MoM. SMM notes NPI plants still have costly nickel ore stocks, keeping production costs high. With a gloomy stainless steel market and low demand, NPI prices are unsupported, and smelters' losses may continue. Thus, a December recovery in NPI production is unlikely.

Indonesia's NPI

Indonesia's NPI production in November 2023 reached 127,400 mt in nickel content, up 10.03% MoM and up 26.6% YoY. The cumulative production for the year amounted to 1,246,900 mt in nickel content, up 19.5% YoY. The rise in Indonesia's high-grade NPI production generally aligns with the forecasts by SMM. The issuance of temporary mining quotas by the Indonesian government has significantly alleviated market concerns over tight nickel ore supply. In the latter half of November, the premiums for medium and high-grade nickel ore have returned to their normal ranges.

High-grade NPI smelting costs in Indonesia have been reduced. Despite falling NPI prices in November, Indonesian smelters retain a cost advantage over Chinese counterparts, keeping most lines at full capacity. New lines starting in November also boosted high-grade NPI output. December's NPI production in Indonesia is expected to stay stable at around 127,700 mt in nickel content, up 0.24% MoM.

Nickel Sulphate

November 2023 saw national nickel sulphate production in China at 36,100 mt in metal content and 164,300 mt in physical content, down 6.39% MoM and 14.77% YoY. The market faced a bearish trend, with year-end inventory reductions and weak demand for nickel sulphate. Some nickel salt firms' slight inventory surplus in October led to reduced production in November, causing the production drop.

December's nickel sulphate market struggled due to reduced precursor company orders, lowering production schedules and demand. Nickel sulphate prices fell to historic lows, hurting manufacturers' profits. Additionally, some factories scheduled maintenance. These factors suggest a continued production drop, with an expected 14.65% MoM decrease from November.

Battery-grade Manganese Sulphate

China's high-purity manganese sulphate production in November 2023 was about 26,100 mt, down 0.76% MoM. Demand was weak, but supply didn't drop much, as some producers unexpectedly continued production, causing a slight inventory buildup. Meanwhile, integrated precursor companies increased manganese sulphate solution output. Thus, despite production adjustments by some firms, overall supply remained relatively stable.

SMM reports that December's ternary precursor production scheduling is set to drop further, reducing high-purity manganese sulphate procurement demand. Supply should theoretically decline too. Yet, some producers might prepare certain amounts of finished product stocks before a concentrated shutdown. Considering these factors, December's high-purity manganese sulphate production is expected to be around 24,700 mt, down 5.36% MoM.

Electrolytic Manganese Dioxide (EMD)

SMM data shows China's November 2023 EMD production at 18,200 mt, with 2,700 mt LMO type, 10,500 mt alkaline-manganese type, and 5,100 mt zinc-carbon types, up 18.60% MoM and 23.10% YoY. January-November production was 180,200 mt, down 30.65% YoY. The rise is due to EMD firms' post-maintenance resumption, increasing operation rates. Yet, the sluggish LMO market curbed procurement, causing slight inventory growth.

As we enter December, with New Year's Day and the Spring Festival approaching, some battery cell manufacturers have plans to stock up, which may result in a slight increase in the procurement of alkaline manganese and zinc-carbon types. However, the sluggish trend in the LMO market is expected to persist, leading to a decline in the production of LMO-type manganese dioxide. Therefore, it is estimated that the production of EMD for December will be around 17,600 mt.

Trimanganese Tetroxide (Mn3O4)

SMM data shows that in November 2023, China's production of Mn3O4 was 9,100 mt, which included 4,800 mt of electronic grade and 4,300 mt of battery grade, down 16.24% MoM and down 37.38% YoY. The cumulative production from January to November 2023 amounted to 116,000 mt, down 18.66% YoY. The production of battery-grade Mn3O4 saw a significant drop, primarily because the spot price of lithium carbonate entered a downward trend, leading to a substantial reduction in LMO orders and, consequently, a decrease in the procurement demand for battery-grade Mn3O4. On the other hand, the production of electronic-grade Mn3O4 remained stable, but the demand was hardly stimulated due to the downturn in the real estate market.

Market insights indicate a worsening LMO market downturn in December, likely causing a larger drop in LMO firms' production schedules. This will also reduce battery-grade Mn3O4 output, while electronic-grade Mn3O4 should remain stable. December's total Mn3O4 production is projected at about 7,900 mt.

High-Carbon Ferrochrome

SMM data reveals China's November 2023 high-carbon ferrochrome production fell slightly to 661,000 mt, down 3.71% MoM but up 25.48% YoY. Inner Mongolia produced 445,000 mt, up 1.14% MoM, while Sichuan production was 28,500 mt, down 35.96% MoM. Despite weaker steel market and price drops, stainless steel production cuts were limited, thus ferrochrome demand reduction was also limited. In the south, losses led to some ferrochrome plants halting production, which coupled with cost support, allowed ferrochrome retail prices to begin to recover. In the north, profitable retail prices kept production high. Thus, high northern operating rates meant overall ferrochrome supply decrease was limited.

December's high-carbon ferrochrome production in China is expected to hit 638,500 mt, down MoM. Yet, with stainless steel production starting to increase, ferrochrome demand is predicted to rebound. Despite lower ferrochrome bid prices from steel mills, lessened surplus expectations are easing ferrochrome producers' pessimism.

Sichuan's dry season has begun, causing a sharp rise in electricity costs and leading to shutdowns among ferrochrome producers there and in other southern areas early in the month. Yet, the north's increased capacity and stable output from large steel plants are keeping ferrochrome supply fluctuations minor.

Stainless Steel

SMM research shows China's November 2023 stainless steel output at 3.0085 million mt, down 4.16% MoM but up 3.91% YoY. The 200 series production was 914,000 mt, down 6.97% MoM; the 300 series was 1.4485 million mt, down 1.56% MoM; and the 400 series was 646,000 mt, down 4.16% MoM. Meanwhile, Indonesia's output was 405,000 mt, up 3.7% MoM and 35.29% YoY. The supply-demand imbalance for stainless steel eased a little in November thanks to October's production cuts. But supply surplus weighed down stainless steel price, which led to losses for mills, prompting year-end strategic maintenance and output reductions, especially in South China for the 200 and 300 series.

Indonesian stainless steel plants boosted production, leveraging lower raw material costs and restarting semi-finished product lines like billets. While China's November production fell, Indonesian stainless steel flowed into the Chinese market, thus the oversupply persisted.

A South China stainless steel mill plans to restart production early due to order backlogs. While the social stockpiles have seen some inventory reduction, levels are still high YoY. In terms of raw materials, November saw high-grade NPI prices stabilize after consecutive drops. Due to oversupply and more Indonesian production, NPI costs for stainless steel mills have fallen since October, easing mill losses. Thus, most mills will likely sustain production. However, some East and North China mills are cutting back, and a South China special steel mill facing significant losses may stop production in December, potentially impacting tens of thousands of mt of 400 -series stainless steel output.

In summary, production resumption after maintenance and high Indonesian output indicate sustained ample supply.

EMM

According to SMM data, China's EMM output was 97,800 mt in November, up 0.67% MoM and 53.08% YOY, bringing total output in the first eleven months of 2023 up to 971,100 mt, up 45.76% YoY. The main reason for slight output uptick in November was that the operating rate of manganese plants was still 70%. In addition, restart of major plants in Guangxi and Hunan offset the impact from some manganese plants’ production halts triggered by production pressure. On the demand side, total stainless crude steel in China decreased in November, and 200 series output ceased hiking and started falling. Despite this, EMM demand was modest due to winter storage demand at the end of November.

In December, an alliance meeting decided to keep operating rate of all manganese plants stable at 70%. Moreover, some plants will resume production or increase operating rate. Therefore, the overall EMM output may keep hiking to 103,700 mt in December, according to survey on scheduled production of manganese plants.

Silicon metal

China produced 403,400 mt of silicon metal in November, up 11,000 mt or 2.8% MoM and 29.1% YoY, according to SMM statistics. The total output was 3.4511 million mt in the first eleven months of 2023, up 7.8% YoY. The operating rate of silicon metal plants climbed to high level in north China, while that kept dipping in southwest China in December. Under this circumstance, silicon metal output in China will diminish in December after peaking in November.

Falling silicon metal output in November was mainly monitored in Yunnan and Sichuan, with a total output decreasing by around 27,000 mt. In Xinjiang, silicon metal output increased by more than 30,000 mt in November, mainly boosted by higher operating rate of large plants and new capacity of some small plants. With start-up of new capacity, silicon metal output inched up in Ningxia, while that in Inner Mongolia, Qinghai, Shaanxi, Chongqing and other places changed little.

Silicon metal output still mixed in December. In northern China such as Xinjiang and Ningxia, silicon metal output hiked amid rising operating rate. High costs and low silicon prices kept dragging down the operating rate of silicon metal plants in south China. Electricity prices generally increased to above 0.5 yuan/kWh in December in Sichuan and Yunnan. The electricity prices in some areas of Sichuan hit 0.63 yuan/kWh. The operating rate in Sichuan and Yunnan may drop to 22% and 39% respectively in December. On the whole, it is expected that silicon metal production in China may drop to around 360,000 mt in December.

Polysilicon

The actual polysilicon output in China was 150,500 mt in November, up 4.9% MoM. In late November, silicon wafer producers’ output hike fuelled more demand for polysilicon, especially N-type polysilicon. There was a shortage of shipments of high-quality materials. Therefore, polysilicon market firmed up. In November, there was rising capacity of several new investment bases of leading companies and start-up of new production lines such as Hoshine, Xinyi, and Qiya. Therefore, domestic polysilicon production is expected to increase to 158,000 mt in December.

PV module

According to SMM statistics, domestic PV module production in November was approximately 49.7GW, down 1% MoM. Global module stocks remained high. Moreover, second- and third-tier PV module makers were mostly in a loss. Under this circumstance, the operating rate of PV module inched down. At present, participants were in strong bearish sentiment. Scheduled PV module production will keep dipping to around 45GW in December.

Solar cell

The actual solar cell output in China in November was 62.6GW, up 97.73% YoY and 2.81% MoM. Of which, P-type cell output was 37.26GW, and N-type cell output was 25.34GW, with N-tpye accounting for 40.48% of the total solar cell output. Weighed down by a large drop in PERC cell demand in the past two months, PERC cell plants slashed production, and some even suspended production in December. Meanwhile, Topcon cell demand hiked, feeding into a steep scheduled output uptick. Solar cell demand fell short of supply, leading to a rapid build-up of inventory. Scheduled solar cell output diminished in December.

PV glass

According to SMM statistics, the monthly PV glass output in China was down 2.85% MoM at 2.2056 million mt in November. A big part of the dip in output was because of one day less in November than October. But newly commissioned furnaces in September-October ramped up production in November. It is expected that PV glass output will further increase due to more working days and rising production of newly commissioned furnaces.

DMC

SMM data showed that Chinese DMC output dipped 6.97% MoM to 173,600 mt in November. The operating rate of the industry was down 5.62 percentage points MoM to 75.22% in November. The reasons for the output slip in November was falling downstream orders and domestic DMC plants’ low operating rate amid more temporary maintenance.

SMM believed that DMC output in December will mainly fluctuate slightly within a small range. December will see restart of some production lines from maintenance and start-up of new capacity, while current demand will be sluggish. Under this circumstance, inventory pressure will increase. Meanwhile, stable costs will exert higher pressure on DMC plants who suffered losses. Therefore, DMC plants will lower operating rate, or even temporarily shut down units.

SiMn alloy

SMM data showed that SiMn alloy production in China in November totalled 926,100 mt, down 9.91% MoM but up 12.13% YoY, bringing total output in the first eleven months of 2023 up to about 10.452 million mt, up 14.36% YoY. In northern China, the operating rate of SiMn alloy plants remained high in Inner Mongolia. Some plants added new capacity, but their actual output was limited. In Ningxia, weak costs and large energy consumption fuelled production cuts. In southern China, falling price was the major factor denting SiMn alloy output. Overall, SiMn alloy output ceased increasing and started dipping in November.

In December, prolonged price weakness increased likelihood of production cuts or halts of some SiMn alloy plants. Annual SiMn alloy output hike was higher than crude steel output uptick, and more SiMn alloy plants were eager to sell off. Therefore, price softness will make it difficult to maintain the operating rate of SiMn alloy plants. SiMn alloy production may keep shrinking to about 835,500 mt in December.

Magnesium ingot

SMM data showed that China's magnesium ingot production in November was 55,388 mt, up 0.7% MoM but down 26% YoY, bringing total output in the first eleven months of 2023 up to about 648,000 mt, down 26% YoY.

In November, production reduction situation of magnesium plants in the main production areas improved, with restart of a few magnesium plants. Several large plants still carried out maintenance. At the same time, there were also plants that reduced production this month. The reasons for the reduction were: 1 Restart of some magnesium ingot plants in Fugu was hindered in the last week of November. 2 Magnesium ingot prices dropped to nearly the cost line, further squeezing profits of magnesium ingot plants, thereby blunting market confidence. Therefore, some plants lowered operating rate. Magnesium ingot output may hike to 56,000 mt in December with restart of some plants.

Magnesium alloy

According to SMM data, China's magnesium alloy production in November was 25,555 mt, down 1.7% MoM and 9% YoY, bringing total output in the first eleven months of 2023 up to about 286,000 mt, up 1.4% YoY.

In November, most major magnesium alloy manufacturers operated as usual according to their production plans, and there was no significant change in output. The reasons for the output slip were: 1. Overall demand weakness amid sluggish domestic economy led a magnesium alloy plant to suspend production. 2. Stricter environmental protection inspections stalled normal production plans of magnesium alloy plants. Judging from current orders received by domestic magnesium alloy companies, given that order receiving failed to improve significantly in December, magnesium alloy plants had no plan to resume production. SMM predicted that magnesium alloy production will keep dipping to 25,000 mt in December.

Magnesium powder

SMM data showed that China's magnesium powder production in November was 5,709 mt, up 23.5% MoM, bringing total output in the first eleven months of 2023 up to 59,000 mt.

In November, output of a magnesium powder maker increased suddenly, as the maker renovated its old production line in October and increased its capacity to 2,000 mt. In addition, a large rise in orders also explained for the output hike in November. The person in charge of a large magnesium powder enterprise said that poor profits of steel mills amid domestic economic downturn made downstream magnesium powder buyers prudent. There were still some magnesium plants’ production cuts caused by security inspection issues. The overall operation rate of magnesium powder remained low. SMM expected domestic magnesium powder production may decrease to 5,000 mt in December.

Pr-Nd oxide

China's Pr-Nd oxide output in November was 6,228 mt, down 1.5% MoM. The decrease was mainly contributed by Guangxi and Jiangxi.

According to SMM research, with sustained price erosions and few inquiries, some separation plants slightly lowered output, and Pr-Nd oxide output in Guangxi dropped by 25%. In Jiangxi, shutdown of some separation plants for maintenance in November fed into a 6% decrease in local Pr-Nd oxide production. Meanwhile, a few separation plants were rushing to meet deadlines towards the end of the year, and gently increased production in November. Among them, Pr-Nd oxide production in Guangdong hiked by 18.5%.

Pr-Nd alloy

China’s Pr-Nd alloy output in November was 5,511 mt, up 1.7% MoM. The increase was mainly contributed by Fujian, Inner Mongolia and Zhejiang, while the output in other regions changed little.

According to SMM, some alloy plants in Inner Mongolia and Zhejiang kept increasing their operating rate to meet year-end replenishing demand from China Northern Rare Earth (Group) High-Tech. In Fujian, alloy plants who produced dysprosium-iron alloy and terbium metal were at a loss, and demand was soft. Therefore, furnaces that were originally used to produce dysprosium-iron alloy and terbium metal were used to produce Pr-Nd alloy, making for a 16% gain in local Pr-Nd alloy output.

Dysprosium oxide

China’s dysprosium oxide production in November was 216 mt, down 0.8% MoM. The dip was mainly reflected in Jiangxi.

According to SMM, shutdown of some separation plants for maintenance lowered dysprosium oxide production by 18% in Jiangxi. However, news of Myanmar's customs closure resurfaced in November, some rare earth ore traders imported goods into China ahead of the closure. Therefore, with sufficient ion-absorption rare earth ore, output medium and heavy rare earth increased in some areas. Among them, dysprosium oxide output in Guangdong and Guangxi in November was up 20% MoM and 15% MoM.

Terbium oxide

China’s terbium oxide output in November was 41.5 mt, down 7% MoM. The dip was mainly reflected in Guangxi and Jiangxi.

According to SMM research, in November few actual transactions and year-end shutdown of separation plants for maintenance made a big dent in terbium oxide output of separation plants in Guangxi and Jiangxi by 9% and 27% respectively.

Molybdenum concentrate

SMM data showed that China's molybdenum concentrate output was 17,900 mt in November, up 1.4% MoM. In November, the operating rate of domestic molybdenum mines was stable amid stable demand, absent maintenance and little impact of environmental inspections. In addition, higher overseas raw material prices than domestic raw material prices most of the time shifted downstream buyers mainly towards domestic raw material. In addition, due to worries that weather conditions would probably stall stable mining of molybdenum concentrate in the future, most molybdenum mines in northern China currently operated at full capacity, in a bid to warrant future supply.

In December, downstream sectors kept production stable, and showed no obvious expectation of production reduction. Therefore, SMM predicted that domestic molybdenum concentrate output will remain stable in December.

Ferromolybdenum

According to SMM data, China’s ferromolybdenum output was up 6.2% MoM at 16,300 mt in November. The hike in output was because of rising demand from steel mills. According to SMM data, bids from steel mills for ferromolybdenum only exceeded 8,000 mt in October, while those in November reached more than 12,000 mt. The increase was mainly contributed to stable molybdenum-containing steel production. The fulfilment of demand postponed from October to November also partially explained for the increase.

In December, steel mills said that profits of molybdenum-containing steel still existed. Rigid demand from downstream sectors was passable. In addition, steel mills usually stockpiled raw materials in advance at the end of each year. Under this circumstance, SMM expected ferromolybdenum output may stabilise in December.

Silver

According SMM Statistics, China’s 1# silver output was 1,350.7,887 mt (including 924.7,887 mt of mineral silver), up 68.8,557 mt or 5.4% MoM but down 1.5% YoY. The reasons for the increase in output were: 1 Some makers resumed operation from maintenance. 2. Raw material suppliers’ enthusiasm for shipments increased. Underpinned by rising prices, smelters purchased more raw materials, thereby increasing output. 3. Silver content in associated ores hiked. At the same time, there were also companies that reduced production. The reasons for the reduction were: 1. The production need to keep pace with this year’s annual production plan. 2. The silver content in raw materials ore became less. 3. Enterprises suspended production for maintenance. Under this circumstance, the overall silver output in November trended up. Towards the end of the year, with the completion of annual production targets and high silver price, the pressure on downstream sectors to purchase raw material ores was also increasing, so SMM expected silver production to decrease in December.

The Fed's speech in December lowered market expectations of an interest rate cut. However, silver prices remained high for a period of time after rising at the end of November, and hovered around 6,000-6,200 yuan/kg for a week before hiking over 6,200 yuan/mt on December 4, exceeding market expectations. The rise in domestic silver prices was mainly caused by ample liquidity. The silver prices started dipping to 5,800 yuan/kg from 6,200 yuan/kg, and then rebounded, but will probably keep declining in the future.

Silver nitrate

Silver nitrate manufacturers with sales qualifications produced 764 mt of silver nitrate in November, up 15.2% MoM and 31.6% YoY. The output of the surveyed enterprises accounted for about 80% of the market. Therefore, China’s silver nitrate output is estimated to be about 968 mt. Among them, silver nitrate output in in Central China decreased by 7.7% MoM, while that in Northwest China, East China and south China increased by 18.8% MoM, 58.8% MoM and 9.5% MoM respectively. The reasons for the output hike were: 1. Silver price in November hit 5,697 yuan/kg (SMM1# silver price), and was not very high in early and mid-to-late November. Therefore, downstream buyers showed high acceptance of silver prices, and had robust demand. In the last week of November, silver prices rose to more than 6,000 yuan/kg, made downstream buyers prudent in placing orders, and they only picked up goods. 2. Due to changes in the price difference between domestic and imported silver, the price difference between silver TD and silver spot prices remained at 400-500 yuan/kg. Imported silver powder has a relative price advantage. Some companies increased demand and refilled imported silver power boasting a price advantage, but then turned to domestic silver powder given that available silver powder for sales decreased. 3. The technical routes of downstream enterprises changed. Demand from PERC cell routed gradually decreased, while that from Topcon cell and other routes slowly increased. Other routes consumed more silver than PERC route. 4. Downstream buyers started refilling a small amount of silver nitrate towards the end of this year, and will cut silver nitrate demand around the Spring Festival. SMM predicted that silver prices will be high in December, but there will still be some need to stock up. Therefore, SMM predicted that silver nitrate production will remain stable or slightly decrease in December.

Antimony ingot

According to SMM survey, China antimony ingot (including antimony ingot, converted crude antimony, cathode antimony, etc.) output in November 2023 was 6,948 mt, down 0.66% MoM. November saw a slew of production halts and some production cutbacks/hike. In detail, among the 33 survey respondents, 14 manufacturers stopped production, up 2 MoM; 16 cut production, down 1 MoM; and 3 kept production normal, down 1 MoM. SMM estimated that China antimony ingot production in December 2023 will be lower than that in November 2023 amid prolonged antimony ore tightness.

Some participants said that mines’ reluctance to sell, geopolitics and other factors will still tighten imported antimony ore supply in China. Under this circumstance, antimony ingot was concentrated in large manufacturers who possessed raw materials. Moreover, antimony ore prices were strong, boosting current antimony ingot costs to 78,000-79,000 yuan/mt. If antimony ingot manufacturers want to maintain reasonable profits, they must ensure that prices were higher than 80,000 yuan/mt at least.

As for antimony trioxide, some participants said that due to cost constraints, if current antimony trioxide price is too low, companies with their own mines and raw materials will restrict the sale of antimony trioxide. In early November, some antimony trioxide manufacturers were reluctant to sell antimony oxide with a grade of 99.8% at the price of below 71,500-72,000 yuan/mt, given that insufficient raw materials led to non-fulfillment of orders signed before, and they were even more unwilling to sell in retail market. However, participants currently had strong confidence in market outlook. On the one hand, they believed that the loan repayment period for the industrial chain almost ended around mid-December, and the loan repayment procedures were completed. Loans for next year were also approved, and a large amount of funds will flow into antimony market, offering a big boost to antimony prices. On the other hand, as long-term contract orders signed in 2023 were completed, imported antimony product prices began to stabilize or even rise, setting a good foundation for 2024. At present, given that waning impact of imported antimony product prices on domestic antimony market, domestic antimony companies gradually had more opportunities in 2023, and antimony product prices will be worth looking forward to.

Sodium antimonate

According to SMM's survey statistics, China's sodium antimonate output in November was down 8.34% MoM at 4,398 mt, but still stood high. Owing to maintenance of some makers, output declined for the first time after maintaining double-digit growth for several consecutive months.

Among the 11 survey respondents, there was shutdown of 2 manufacturer, normal production of 3 producers, rising production of 3 producers and a large drop in production of 3 producers. Shutdown of units for maintenance made a big dent in production of some producers. Some producers cut production as antimony price slip put end-users on wait-and-see mood. In a word, production resumption will probably be monitored in December. PV makers are likely to resume replenishing purchases in December. Robust demand from PV sector will be felt. Therefore, SMM predicted that sodium antimonate output in China will remain stable, or rebound in December.

Refined bismuth

According to SMM's survey, China's refined bismuth production in November was 1,996.77 mt, down 6.83% MoM. Among the 24 survey respondents, 7 manufacturers stopped production, unchanged from last month. Judging from changes on production of manufacturers, some manufacturers' output continued to decrease in November, with 4 of them seeing a significant drop in output. This also caused the overall antimony ingot production in November to decrease compared with the previous month. SMM predicted that refined bismuth output in China may remain stable in December, and may also diminish amid tight raw material supply.

Customs data showed that China's export volume of wrought bismuth, bismuth products, unwrought bismuth and scrap was 263.05 mt in October, lower than 301.5 mt in September.

Titanium dioxide

According to SMM data, China's titanium dioxide output was 330,000 mt in November, down 1.4% MoM but up 7.7% YoY, bringing total output in the first eleven months of 2023 up to 3.505 million mt, down 0.4% YoY.

Some titanium dioxide companies started carrying out scheduled maintenance in a slack season to ease pressure from rapid inventory uptick, lowering titanium dioxide production. With price reduction announced by leading companies, negotiated prices of titanium dioxide moved downwards. Therefore, titanium dioxide prices were stable-to-soft, increasing market price competition. In December, rising inventory of some producers may lead to the next round of titanium dioxide price slip, further squeezing profits of titanium dioxide producers. Meanwhile, new capacity will increase. Under this circumstance, the market competition will be increasingly fierce. Therefore, some titanium dioxide producers may suspend production. SMM estimated that titanium dioxide production will be 320,000 mt in December.

APT

SMM data showed that Chinese APT output was down 2.6% MoM at 11,000 mt in November. Tungsten concentrate market saw tight output, low-priced inventory cutbacks, and holders’ strong willingness to keep prices firm. Therefore, APT smelting costs increased, and its growth rate was faster than demand growth. Under this circumstance, APT prices had difficulty of hiking, leaving APT smelters with more losses. In addition to necessary long-term contract delivery, production and consumption of bulk cargoes shrank significantly. Therefore, APT production started declining to a certain extent.

In December, APT market will still witness rising tungsten concentrate prices and shrinking demand. Therefore, APT smelters will only maintain basic production. It is expected that APT output will keep inching down in December.

Lithium Carbonate

November saw domestic lithium carbonate production at 43,100 mt, up 6.6% MoM and 17.58% YoY. From January to November, production reached 416,100 mt, up 31.94% YoY. This rise is due to increased output produced from lepidolite and spodumene after a production dip and maintenance in September and October, with recovery at month-end. New enterprise ramp-ups also helped. However, production from salt lakes and recycled scrap fell due to seasonal factors and cost inversion issues, respectively, challenging production sustainability.

Heading into December, some smaller Jiangxi lithium salt producers, reliant on purchased lithium ore, have paused production for maintenance amid losses and less subcontracting work. A few may restart within the month. Major smelters using spodumene and lepidolite are running steadily, with no short-term maintenance planned.

Salt lake lithium operations face minor seasonal declines, and recycling companies’ production keeps falling due to cost inversion effects. December's domestic lithium carbonate output is expected at 40,800 mt, down 5.37% MoM but up 17.13% YoY. The annual total is projected at 456,900 mt, up 30.47% YoY.

Lithium Hydroxide

In November 2023, China's lithium hydroxide production reached 20,970 mt, down 4% MoM and 16% YoY. In November, the overall market for lithium hydroxide continued to be characterized by weak supply and demand.

Despite new production lines and increased total capacity, lithium hydroxide remains in oversupply. Price inversion with lithium carbonate has led to losses and slow production and sales for causticizing smelters. High inventories and slow de-stocking persist, prompting some producers to reduce operating rates, slash production, and clear lithium hydroxide and raw material stocks for year-end cash flows.

Demand for lithium hydroxide remains weak, with a bleak market outlook, as downstream battery cell makers cut orders for high-nickel products, lengthening the inventory cycle for cathode materials. Since mid-November, purchasing has dropped sharply, with manufacturers focusing on fulfilling long-term contracts and spot buying nearly ceasing, showing little sign of near-term recovery.

SMM forecasts that given the current lithium hydroxide production has reached a phase of low output, the market will continue to see a downward trend in both volume and price. However, the decline is expected to narrow. The projected production for December is anticipated to be 20,540 mt, down 2% MoM and 19% YoY.

Cobalt Sulphate

China's November cobalt sulphate output fell to 5,700 mt in metal content, down 13% MoM and 22% YoY, due to falling prices, decreased demand, and rising inventories, creating a market oversupply. Firms with external raw material sourcing face cost inversion from high-cost stock, leading to production cuts.

December's cobalt sulphate production is expected to decline further due to pessimistic market forecasts and reduced output by downstream precursor firms, exacerbating weak demand amid oversupply. The estimated December production is 4,822 mt in metal content, down 15% MoM and 30% YoY.

Tricobalt Tetraoxide (Co3O4)

China's November Co3O4 production hit 6,637 mt, down 18% MoM but up 18% YoY. The drop was due to early demand fulfillment, resulting in fewer orders and slower long-term contract deliveries. With rising spot inventories, prices fell. Despite lower cobalt salt prices, raw material costs remained stable. Smelters, under cost inversion and demand reduction pressures, cut production schedules.

December's consumer market is projected to be weak, with limited new orders and slow spot sales. Anticipating continued softness in the spot market, production is likely to keep falling. Estimated output is around 5,551 mt in December, down 16% MoM but up 11% YoY.

Ternary Cathode Precursor

China's November production of ternary cathode precursor was about 69,665 mt, down 5% MoM and 23% YoY. The January-November total reached 745,801 mt, down 4% YoY.

As year-end nears, listed ternary precursor producers are cutting inventory, aligning production with sales. To meet annual targets, some offered discounts to win consumer market orders. Overseas, November demand weakened, with expectations for lower precursor export volumes.

Domestic demand is stable yet varied among cathode factories. Some see rising end-projects boosting precursor orders, while others face falling demand due to stockpiling. Series 6's share is dropping as battery plants cut late November orders, sharply reducing mid-nickel precursor production for subcontracted firms.

Heading into December, ternary precursor firms are expected to tighten inventory control due to weakening demand, with likely major cuts in production plans. Overseas demand, already reduced earlier, should stay stable. Domestically, a notable drop in mid- and low-nickel precursor production is expected. China's December ternary cathode precursor output is estimated at 62,684 mt, down 10% MoM and 18% YoY.

Ternary Cathode Materials

China's November 2023 ternary cathode materials production was 55,867 mt, steady from October but down 16% YoY. January-November 2023 saw a total of 567,933 mt, down 6% YoY.

In the digital and power batteries markets, year-end order weakening leads to fierce price competition among top ternary material companies, squeezing out smaller producers. In the power battery market, there was stable demand from major domestic and some tier-two battery makers, with mid-nickel projects growing slightly despite a dip in high-nickel output. Some firms face low operating rates due to a sharp drop in overseas battery demand. Low-nickel and high-nickel materials’ shares are falling, while mid-nickel's share grows.

Entering December, demand in digital and power batteries continues to fall as some small domestic battery factories shut down, with only exports slightly stable. NEV orders are also declining. High-nickel production may slightly increase or stabilize for ternary cathode firms, especially those linked to leading and tier-two battery manufacturers targeting year-end boosts, mainly for overseas markets. However, mid- and low-nickel material production is significantly reduced, shifting the recent demand trend. China's December ternary cathode material production is estimated at 52,981 mt, down 5% MoM but stable YoY.

Iron Phosphate

China's November iron phosphate production was 104,900 mt, down 9% MoM but up 12% YoY, with January-November total up 63% YoY. The production drop is due to weaker downstream demand, with Q4 2023 seeing LFP businesses reducing inventory, cutting raw material purchases, and thus lowering iron phosphate demand.

Iron phosphate firms are cutting operating rates to match sales and prevent stock buildup. November's production costs stayed similar to October, but cost inversion dampens production enthusiasm. December's off-season expectations of inventory cuts in downstream sectors mean a persistent demand drop for iron phosphate. The industry is entering a "hibernation mode," with widespread production cuts and halts, leading to a continued output decline. December 2023's iron phosphate production in China is expected to fall by 22% MoM, with a slight YoY increase of less than 1%, estimated at 81,700 mt.

LFP

In November, China's LFP production was 114,000 mt, down 10% MoM and 5% YoY, with January-November total up 34% YoY. Q4 2023 saw lithium carbonate prices fall, prompting battery cell manufacturers to reduce inventories, which lowered LFP demand. The primary raw material's price drop in November also reduced LFP manufacturing costs. LFP producers continued aligning output with sales, minimizing finished goods inventory, significantly cutting total market supply.

As the year ends, NEV and energy storage sectors are clearing finished goods inventory, only making necessary purchases, thus limiting LFP material demand. From December to Q1 2024, the market is expected to enter its traditional off-season with a bearish outlook, reducing LFP demand. Many LFP producers are cutting back or stopping production, which will significantly lower output. December 2023's LFP production in China is expected to drop to 91,050 mt, down 20% MoM and 10% YoY, marking the first time since May 2023 that monthly LFP production will fall below 100,000 mt.

LCO

In November, China's LCO production was 6,980 mt, down 3% MoM and 11% YoY. Supply shrank noticeably in November from October. The LCO market hit its off-season in November; despite some early to mid-month sporadic new orders, activity slowed considerably later, easing LCO prices. Raw material costs, including cobalt and lithium carbonate, significantly fell, lowering production costs.

The LCO market is driven by long-term contracts, with few spot deals. Downstream cell makers are skeptical about near-term digital product demand, potentially delaying orders and slowing pickups. The e-cigarette market remains cool, while battery swapping demand stays stable. Entering December's off-season, downstream firms weigh raw material costs, reducing orders with little hope for a short-term rebound. December's LCO production is forecasted at 6,081 mt, down 13% MoM, up 6% YoY.

LMO

China's November 2023 LMO production was 6,897 mt, down 19% MoM and 23% YoY. Lithium carbonate's spot price kept falling, dragging down LMO prices. Battery cell manufacturers tend to buy more when prices rise than fall, leading to only moderate LMO demand and a strong push for price cuts. This resulted in most LMO businesses seeing a significant drop in November order volumes.

Heading into December, lithium carbonate's spot price is expected to keep falling, and cell manufacturers' production desire remains low, focusing on reducing inventory. This could tighten LMO purchasing further. With significant losses, LMO firms are cutting production, some planning pauses in December. LMO output is projected at about 4,959 mt for December, down 28% MoM and 27% YoY.