SHANGHAI, Mar 24 (SMM) - This is a roundup of China's metals weekly inventory as of March 24.

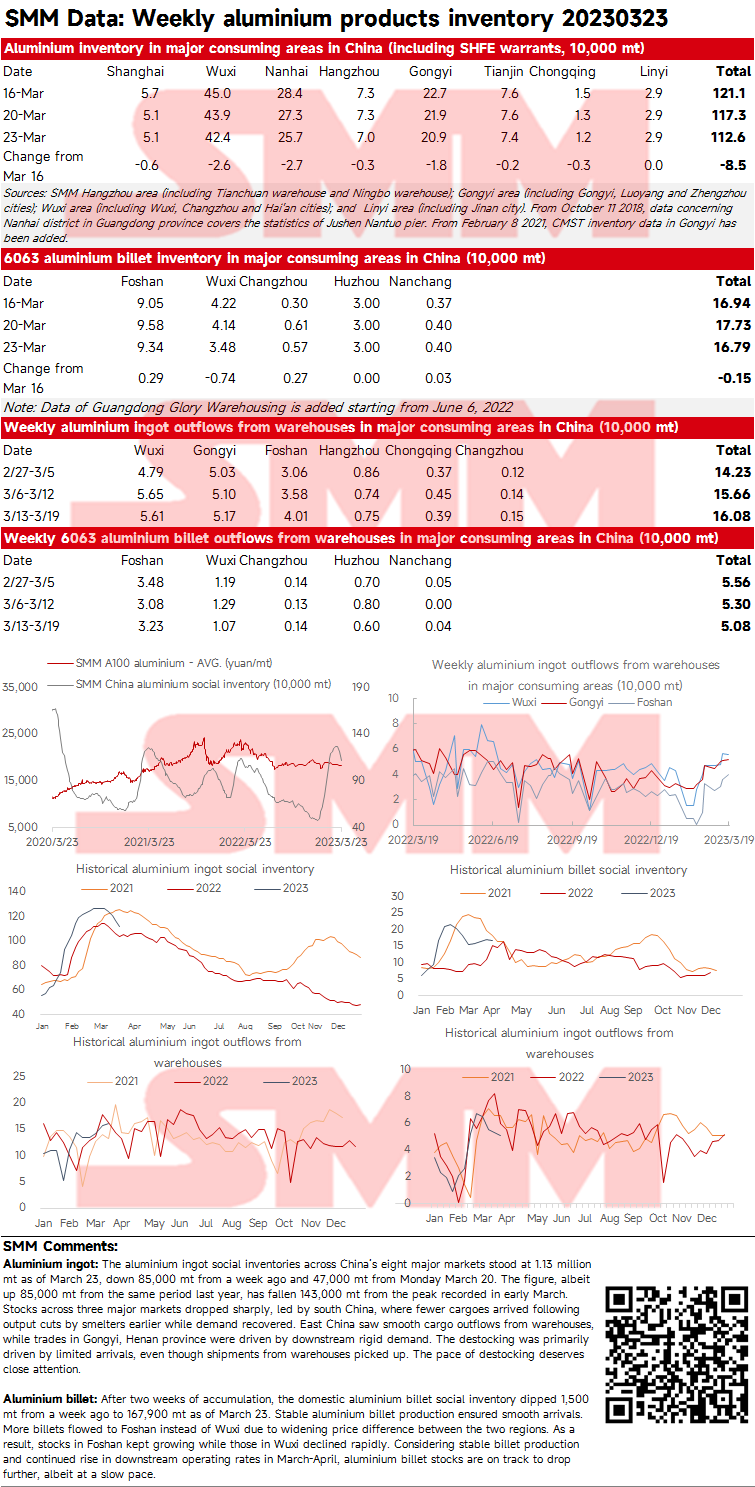

SMM Weekly Update of China Aluminium Ingot and Billet Social Inventories (Mar 23, 2023)

Aluminium ingot: The aluminium ingot social inventories across China’s eight major markets stood at 1.13 million mt as of March 23, down 85,000 mt from a week ago and 47,000 mt from Monday March 20. The figure, albeit up 85,000 mt from the same period last year, has fallen 143,000 mt from the peak recorded in early March. Stocks across three major markets dropped sharply, led by south China, where fewer cargoes arrived following output cuts by smelters earlier while demand recovered. East China saw smooth cargo outflows from warehouses, while trades in Gongyi, Henan province were driven by downstream rigid demand. The destocking was primarily driven by limited arrivals, even though shipments from warehouses picked up. The pace of destocking deserves close attention.

Aluminium billet: After two weeks of accumulation, the domestic aluminium billet social inventory dipped 1,500 mt from a week ago to 167,900 mt as of March 23. Stable aluminium billet production ensured smooth arrivals. More billets flowed to Foshan instead of Wuxi due to widening price difference between the two regions. As a result, stocks in Foshan kept growing while those in Wuxi declined rapidly. Considering stable billet production and continued rise in downstream operating rates in March-April, aluminium billet stocks are on track to drop further, albeit at a slow pace.

Copper Inventory in Major Chinese Markets Fell This Week

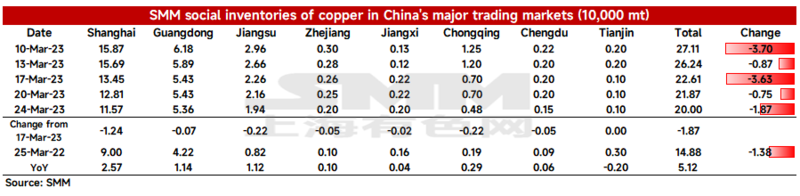

As of Friday March 24, SMM copper inventory across major Chinese markets stood at 200,100 mt, a sharp decline of 18,700 mt from Monday and 26,100 mt from last Friday. Total inventories added 3,400 mt from pre-CNY levels, rolling back all gains post-CNY holidays. This is the first inventory decline for four consecutive weeks since end-December 2022. Compared with Monday, copper inventories fell across all regions. Total domestic inventories added 51,200 mt from 148,800 mt in the same period last year. Inventories in Shanghai were 25,700 mt higher than the same period last year, those Guangdong were 11,400 mt higher, those in Jiangsu were 11,200 mt higher and those in Chongqing increased 2,900 mt.

In detail, the inventories in Shanghai dropped 12,400 mt from Monday to 115,700 mt, and those in Jiangsu fell 2,200 mt to 19,400 mt. While downstream stockpiling was lower than the week prior, shipments arrivals declined, reducing total inventories in east China. Inventory in Guangdong decreased by 700 mt from Monday to 53,600 mt. Arriving shipments in Guangdong increased and consumption weakened, resulting in lower daily average shipments from Guangdong. The inventory decline in Chongqing is attributable to local stronger consumption.

Sellers will be rush to liquidate stocks at the month-end, so the supply should increase next week. Downstream purchasing interest will fall. In aggregate, SMM expects supply to grow and demand to weaken next week, slowing the inventory decline compared to this week.

Copper Inventories in China Bonded Zone Decreased This Week

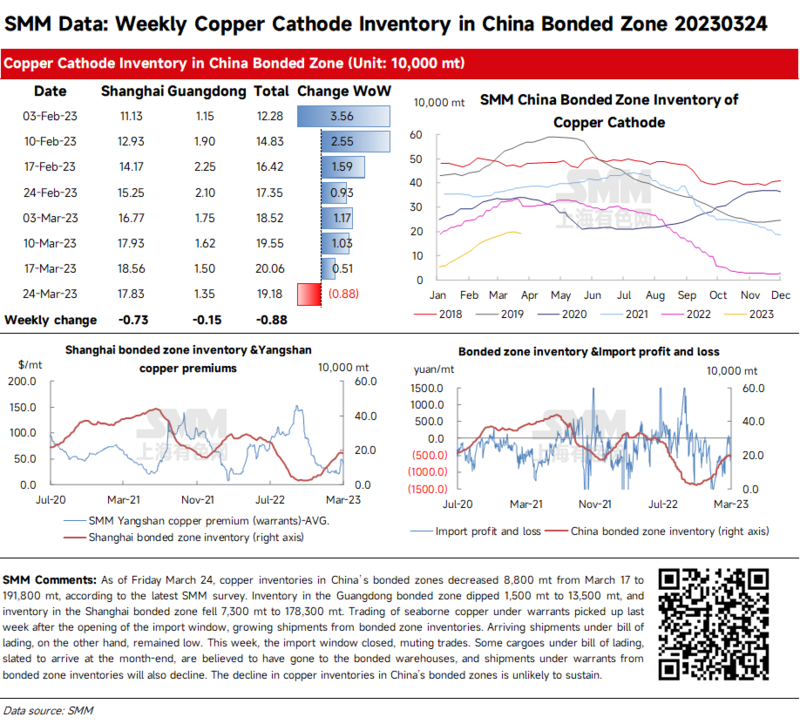

As of Friday March 24, copper inventories in China’s bonded zones decreased 8,800 mt from March 17 to 191,800 mt, according to the latest SMM survey. Inventory in the Guangdong bonded zone dipped 1,500 mt to 13,500 mt, and inventory in the Shanghai bonded zone fell 7,300 mt to 178,300 mt. Trading of seaborne copper under warrants picked up last week after the opening of the import window, growing shipments from bonded zone inventories. Arriving shipments under bill of lading, on the other hand, remained low. This week, the import window closed, muting trades. Some cargoes under bill of lading, slated to arrive at the month-end, are believed to have gone to the bonded warehouses, and shipments under warrants from bonded zone inventories will also decline. The decline in copper inventories in China’s bonded zones is unlikely to sustain.

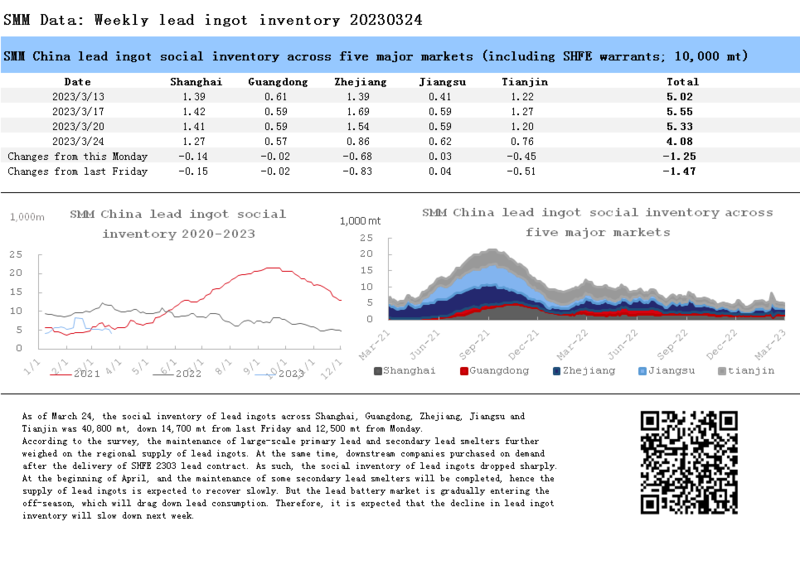

Decline in Lead Ingot Inventory will Slow Down amid Increasing Supply and Weakening Demand

As of March 24, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 40,800 mt, down 14,700 mt from last Friday and 12,500 mt from Monday.

According to the survey, the maintenance of large-scale primary lead and secondary lead smelters further weighed on the regional supply of lead ingots. At the same time, downstream companies purchased on demand after the delivery of SHFE 2303 lead contract. As such, the social inventory of lead ingots dropped sharply. At the beginning of April, and the maintenance of some secondary lead smelters will be completed, hence the supply of lead ingots is expected to recover slowly. But the lead battery market is gradually entering the off-season, which will drag down lead consumption. Therefore, it is expected that the decline in lead ingot inventory will slow down next week.

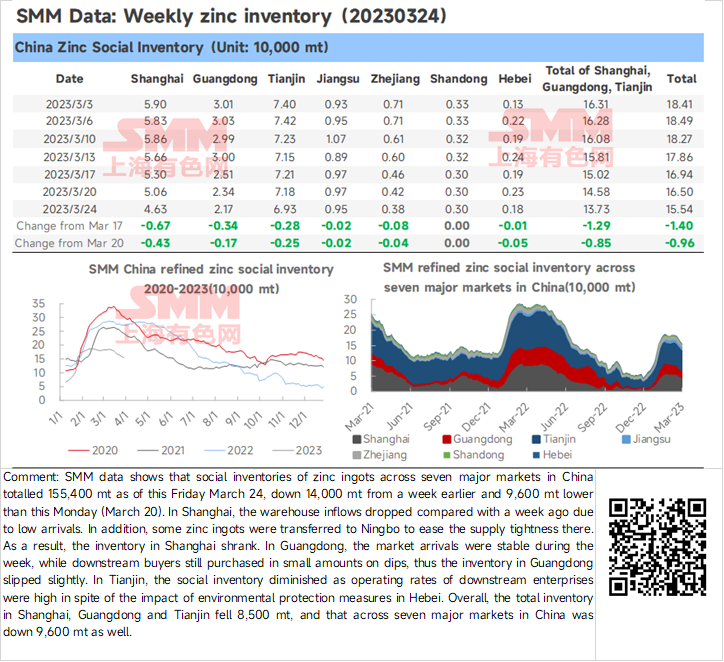

Zinc Ingot Social Inventory Down 9,600 mt from Monday

SMM data shows that social inventories of zinc ingots across seven major markets in China totalled 155,400 mt as of this Friday March 24, down 14,000 mt from a week earlier and 9,600 mt lower than this Monday (March 20).

In Shanghai, the warehouse inflows dropped compared with a week ago due to low arrivals. In addition, some zinc ingots were transferred to Ningbo to ease the supply tightness there. As a result, the inventory in Shanghai shrank. In Guangdong, the market arrivals were stable during the week, while downstream buyers still purchased in small amounts on dips, thus the inventory in Guangdong slipped slightly. In Tianjin, the social inventory diminished as operating rates of downstream enterprises were high in spite of the impact of environmental protection measures in Hebei.

Overall, the total inventory in Shanghai, Guangdong and Tianjin fell 8,500 mt, and that across seven major markets in China was down 9,600 mt as well.

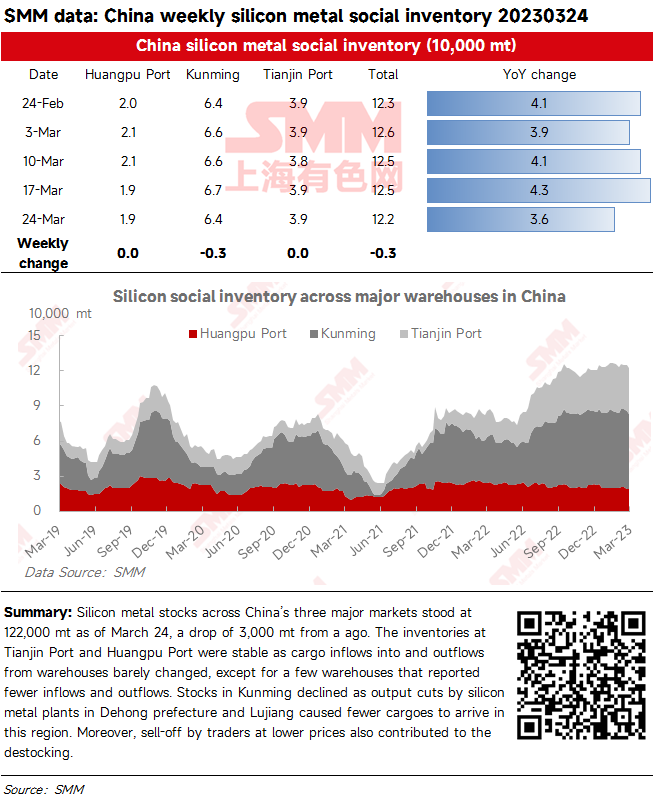

Silicon metal stocks fell

Silicon metal stocks across China’s three major markets stood at 122,000 mt as of March 24, a drop of 3,000 mt from a ago. The inventories at Tianjin Port and Huangpu Port were stable as cargo inflows into and outflows from warehouses barely changed, except for a few warehouses that reported fewer inflows and outflows. Stocks in Kunming declined as output cuts by silicon metal plants in Dehong prefecture and Lujiang caused fewer cargoes to arrive in this region. Moreover, sell-off by traders at lower prices also contributed to the destocking.

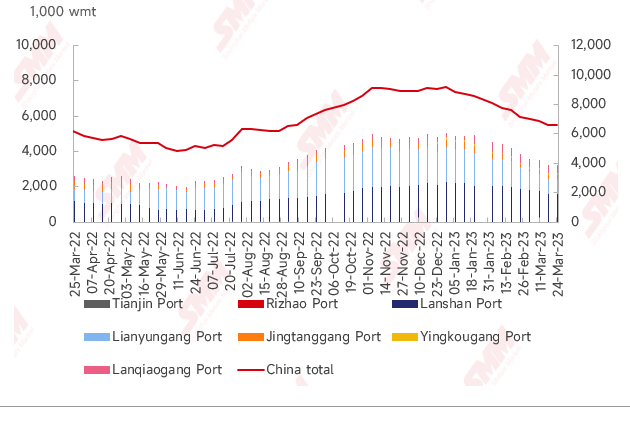

Nickel Ore Inventories at Chinese Ports Dip 185,000 wmt WoW

As of March 24, the nickel ore inventories at Chinese ports dropped 185,000 wmt from a week earlier to 6.41 million wmt. The total Ni content stood at 50,000 mt. The port inventory across seven major Chinese ports stood at 2.99 million wmt, 235,000 wmt lower than last week. Nickel ore prices crashed this week on the falling NPI prices, but buyers still expected a lower ore price. Traders and mines wrestled over the prices. NPI plants were reluctant to purchase due to the dropping NPI prices. The rainy season in the Philippines did not end, thus the port inventory will fall.

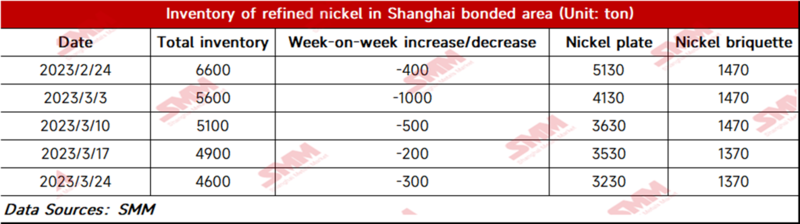

Bonded Zone Inventory of Nickel Falls 300 mt from March 17

Bonded zone inventory of nickel dropped 300 mt to 4,600 mt WoW as of March 24, with the inventory of nickel briquettes and nickel plates standing at 1,370 mt and 3,230 mt respectively, which was in line with market expectations. Nickel prices hovered at lows under pressure. Downstream companies purchased pure nickel on demand. The spread between nickel briquette and nickel sulphate shrank on the fall in pure nickel prices, but the nickel briquette demand from the new energy sector remained critically low.