SHANGHAI, Mar 10 (SMM) - This is a roundup of China's metals weekly inventory as of March 10.

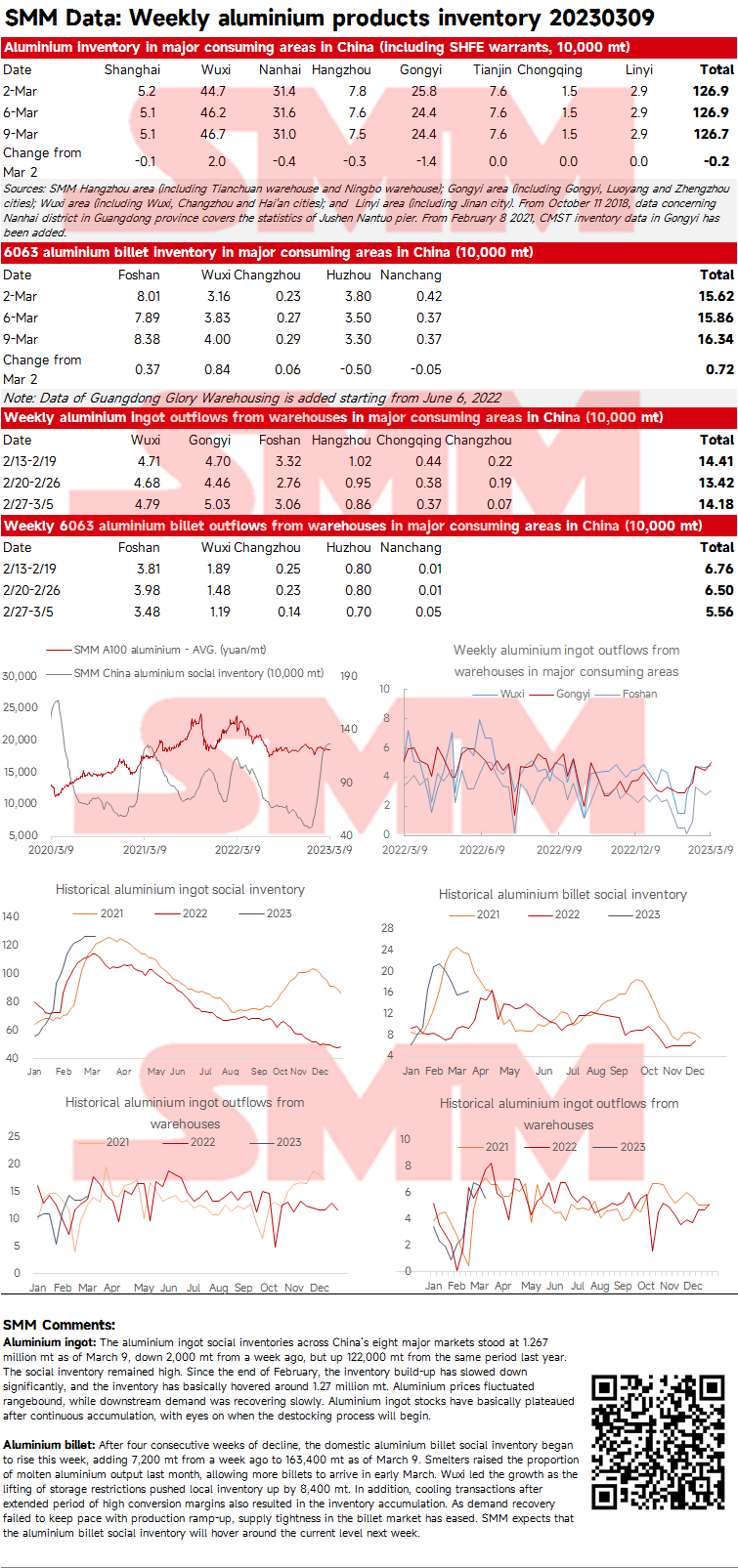

SMM Aluminium Ingot and Billet Social Inventory in China as of March 9

Aluminium ingot: The aluminium ingot social inventories across China's eight major markets stood at 1.267 million mt as of March 9, down 2,000 mt from a week ago, but up 122,000 mt from the same period last year. The social inventory remained high. Since the end of February, the inventory build-up has slowed down significantly, and the inventory has basically hovered around 1.27 million mt. Aluminium prices fluctuated rangebound, while downstream demand was recovering slowly. Aluminium ingot stocks have basically plateaued after continuous accumulation, with eyes on when the destocking process will begin.

Aluminium billet: After four consecutive weeks of decline, the domestic aluminium billet social inventory began to rise this week, adding 7,200 mt from a week ago to 163,400 mt as of March 9. Smelters raised the proportion of molten aluminium output last month, allowing more billets to arrive in early March. Wuxi led the growth as the lifting of storage restrictions pushed local inventory up by 8,400 mt. In addition, cooling transactions after extended period of high conversion margins also resulted in the inventory accumulation. As demand recovery failed to keep pace with production ramp-up, supply tightness in the billet market has eased. SMM expects that the aluminium billet social inventory will hover around the current level next week.

Copper Inventory in Major Chinese markets Plunged Sharply This Week

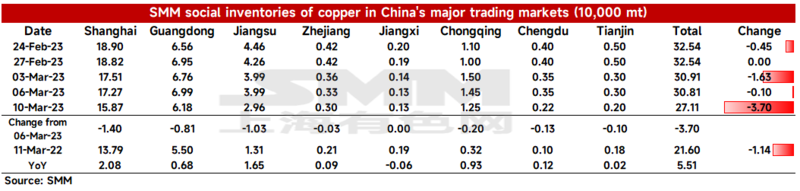

As of Friday March 10, SMM copper inventory across major Chinese markets stood at 271,100 mt, a sharp decline of 37,000 mt from Monday and 38,000 mt from last Friday. Total inventories added 74,500 mt from pre-CNY levels, and fell for two consecutive weeks since end-December 2022. Inventories have staged an inflection point, and the destocking appeared to have accelerated. Compared with Monday, copper inventories fell across China’s major markets. Total domestic inventory grew 55,100 mt from 216,000 mt in the same period last year. The inventory was 20,800 mt higher than the same period last year in Shanghai, 6,800 mt higher in Guangdong, 16,500 mt higher in Jiangsu, and 9,300 mt higher in Chongqing.

Inventories in Shanghai decreased by 14,000 mt to 158,700 mt compared with Monday, and those in Jiangsu decreased by 10,300 mt to 29,600 mt. SMM understood that delivery taking in east China this week increased significantly compared with last week, driven by falling copper prices and increasing orders. Limited customs clearance of imported copper and exports of some copper cathode also contributed to the inventory decline in east China. Inventories in Guangdong decreased by 8,100 mt to 61,800 mt. As the large downstream producers resumed production this week, the consumption in Guangdong has also increased significantly. But this was not reflected in the average daily shipments from Guangdong warehouses due to significant growth in shipments from smelters and lower volumes of delivery taking by downstream buyers.

As the delivery of the SHFE front-month copper contract approaches, it is expected that the amount of shipments from smelters to warehouses will increase. And the customs clearance of imported copper is expected to increase from this week. As such, the total supply next week is expected to increase. Consumption looks set to recover due to the onset of the peak season and lower copper prices. To sum up, SMM expects both supply and demand to grow next week. And inventory would fall, with a smaller decline compared with this week.

Zinc Ingot Social Inventory Down 2,200 mt from this Monday

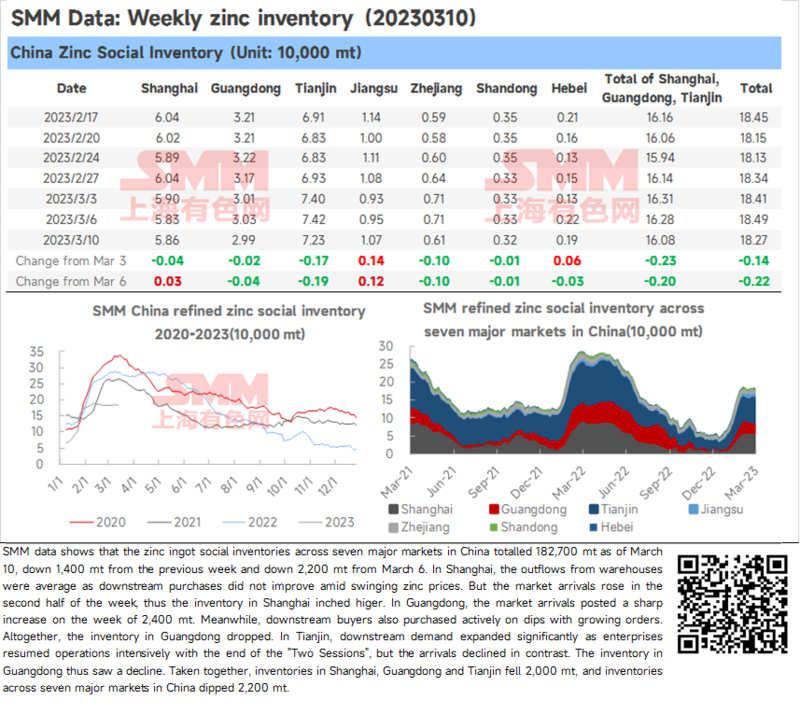

SMM data shows that the zinc ingot social inventories across seven major markets in China totalled 182,700 mt as of March 10, down 1,400 mt from the previous week and down 2,200 mt from March 6. In Shanghai, the outflows from warehouses were average as downstream purchases did not improve amid swinging zinc prices. But the market arrivals rose in the second half of the week, thus the inventory in Shanghai inched higher. In Guangdong, the market arrivals posted a sharp increase on the week of 2,400 mt. Meanwhile, downstream buyers also purchased actively on dips with growing orders. Altogether, the inventory in Guangdong dropped. In Tianjin, downstream demand expanded significantly as enterprises resumed operations intensively with the end of the "Two Sessions", but the arrivals declined in contrast. The inventory in Guangdong thus saw a decline. Taken together, inventories in Shanghai, Guangdong and Tianjin fell 2,000 mt, and inventories across seven major markets in China dipped 2,200 mt.

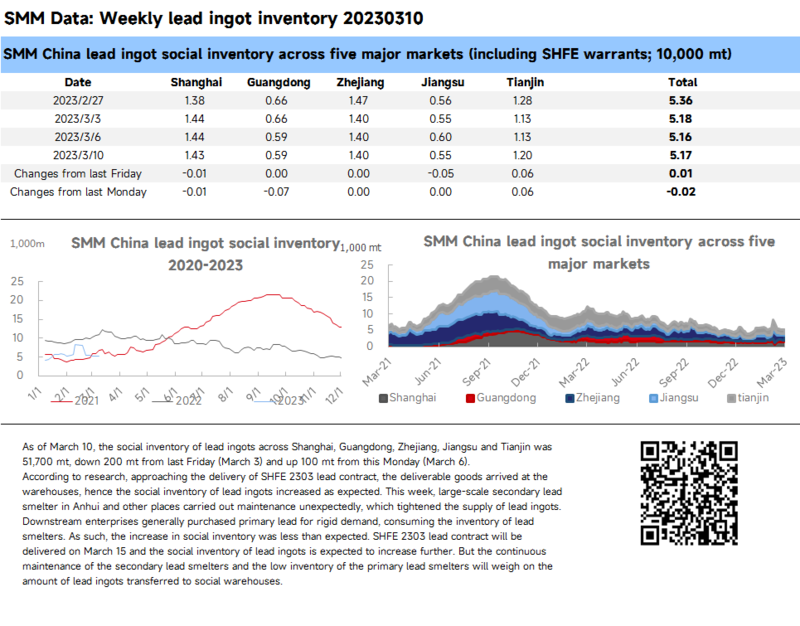

Social Inventory of Lead Ingots Increases Less than Expected

As of March 10, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 51,700 mt, down 200 mt from last Friday (March 3) and up 100 mt from this Monday (March 6).

According to research, approaching the delivery of SHFE 2303 lead contract, the deliverable goods arrived at the warehouses, hence the social inventory of lead ingots increased as expected. This week, large-scale secondary lead smelter in Anhui and other places carried out maintenance unexpectedly, which tightened the supply of lead ingots. Downstream enterprises generally purchased primary lead for rigid demand, consuming the inventory of lead smelters. As such, the increase in social inventory was less than expected. SHFE 2303 lead contract will be delivered on March 15 and the social inventory of lead ingots is expected to increase further. But the continuous maintenance of the secondary lead smelters and the low inventory of the primary lead smelters will weigh on the amount of lead ingots transferred to social warehouses.

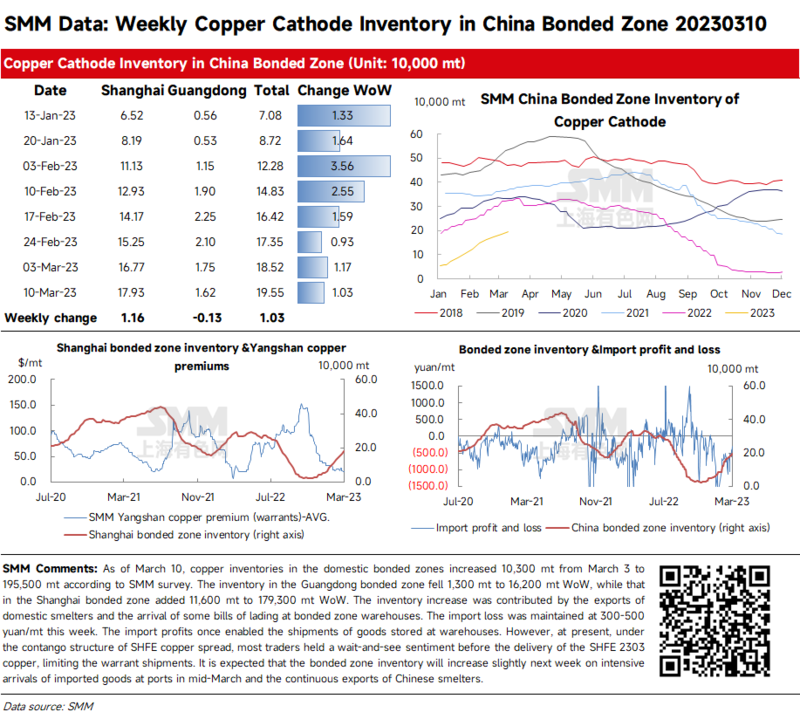

Copper Inventories in Domestic Bonded Zone Add 10,300 mt from March 3

As of March 10, copper inventories in the domestic bonded zones increased 10,300 mt from March 3 to 195,500 mt according to SMM survey. The inventory in the Guangdong bonded zone fell 1,300 mt to 16,200 mt WoW, while that in the Shanghai bonded zone added 11,600 mt to 179,300 mt WoW. The inventory increase was contributed by the exports of domestic smelters and the arrival of some bills of lading at bonded zone warehouses. The import loss was maintained at 300-500 yuan/mt this week. The import profits once enabled the shipments of goods stored at warehouses. However, at present, under the contango structure of SHFE copper spread, most traders held a wait-and-see sentiment before the delivery of the SHFE 2303 copper, limiting the warrant shipments. It is expected that the bonded zone inventory will increase slightly next week on intensive arrivals of imported goods at ports in mid-March and the continuous exports of Chinese smelters.

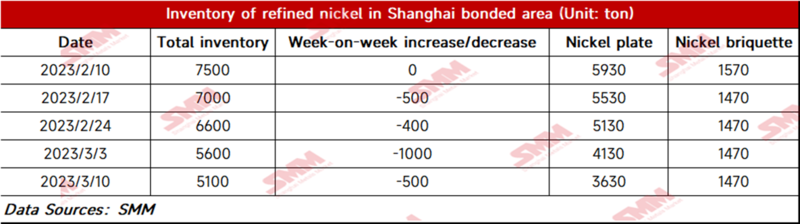

Bonded Zone Inventory of Nickel Drops Slightly from March 3

Bonded zone inventory of nickel dropped 500 mt to 5,100 mt WoW as of March 10, with the inventory of nickel briquettes and nickel plates standing at 1,470 mt and 3,630 mt respectively. The small fall in bonded zone inventory was basically in line with expectations. Nickel plate inventory fell more despite the poor downstream demand amid the dropping nickel prices. Nickel briquette demand from the stainless steel sector was low, thus the bonded zone inventory of nickel briquettes stood flat WoW this week.