SHANGHAI, Mar 9 (SMM) -

Copper cathode

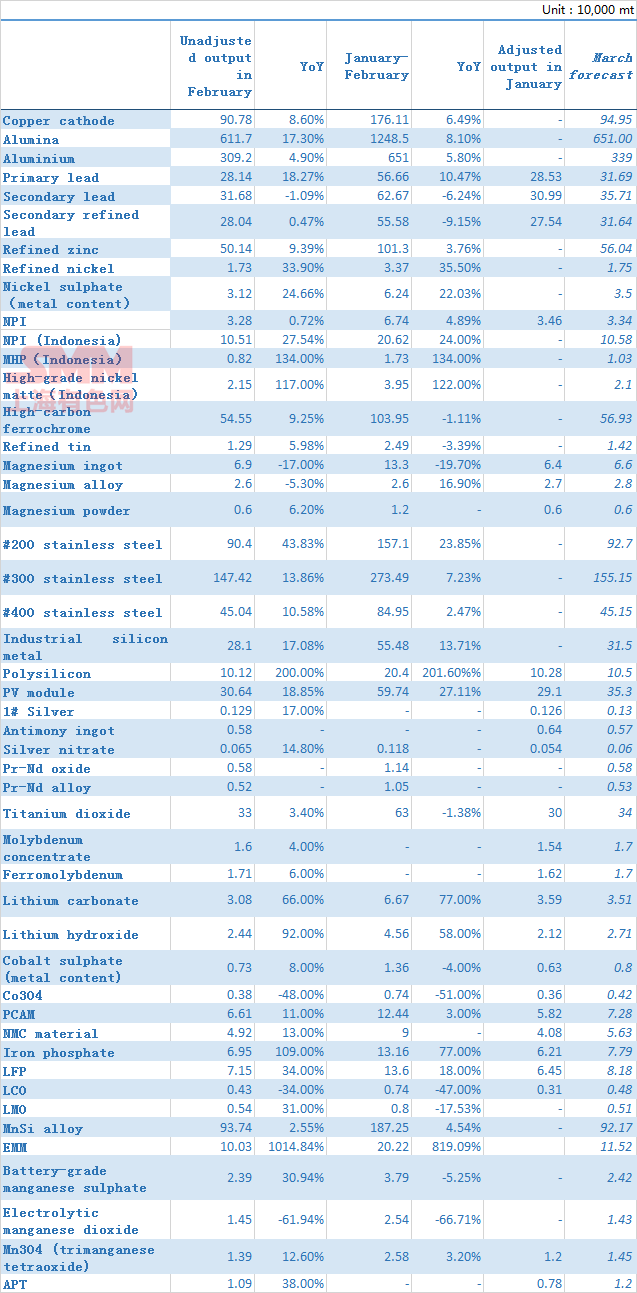

SMM data showed that China’s copper cathode output stood at 907,800 mt in February, up 6.4% from the previous month and 6.49% from the same period in 2022. The actual output was 8,500 mt higher than the expected 899,300 mt.

Although a smelter carried out maintenance ahead of schedule in February, thanks to the ramp-up of new capacity and the resumption of three smelters, the actual output was higher than expected. Coupled with the production increase of some smelters after the Chinese New Year (CNY) holiday. The output of copper cathode in February increased significantly both month-on-month (MoM) and year-on-year (YoY), with average operating rate rising 5 percentage points MoM to 84.87%.

Entering March, despite the maintenance plans of three smelters, the actual output in March will not fall as smelters have restocked sufficient raw materials. Meanwhile, the output of newly commissioned smelters in central China will further increase in March. The sufficient supply of blister copper and copper scrap provides support for the production and the unfavourable news about overseas mines are unlikely to affect the domestic smelters in light of sufficient copper concentrate stocks. Due to statistical cycle of some smelters, fewer working days in February may affect the output. But most smelters calculate output based on natural month, hence the output will increase accordingly.

To sum up, SMM expects that China’s copper cathode output will stand at 949,500 mt in March, up 41,700 mt or 4.59% MoM and 11.9% YoY based on the current production schedules. The output is estimated at 2.71 million mt in January-March, up 8.32% or 208,300 mt year-on-year.

Aluminium

Domestic aluminium output in February (28 days) was up 4.9% year-on-year to 3.09 million mt. From January to February 2023, the domestic aluminium output totalled 6.51 million mt, a year-on-year increase of 5.8%. At the end of February, the aluminium producers in Yunnan intensively reduced their production, but enterprises concentrated on casting ingots. As such, the output did not decline rapidly and the average daily output in February increased 150 mt month-on-month to 110,400 mt. In February, most enterprises in Guizhou, Guangxi, and Sichuan resumed the production, but the slow power supply recovery weighed on the resumption of producers in Guizhou. The total resumed capacity reached 200,000 mt in February. At the same time, Phase II aluminium project of Gansu Zhongrui reached the designed capacity, and the new capacity of Guizhou Xingren Denggao and Baiyinhua ramped up. The total new capacity reached around 160,000 mt. Enterprises in Yunnan reduced the production by 780,000 mt, contributing to most production cuts in February. According to SMM statistics, by the beginning of March, domestic installed aluminium capacity reached 45.26 million mt (including the production capacity that has been installed but has not been put into production). The domestic operating aluminium capacity fell to 39.88 million mt, and the national operating rate averaged about 88.1%. In February, the proportion of aluminium liquid grew 3.5 percentage points month-on-month to 62.7% due to rising output of aluminium billet and aluminium alloy.

The previous production reduction in Yunnan will gradually be reflected in the output in March. Although the operating capacity in Guizhou and Sichuan is expected to resume, but it will make little contribution to production increase. The average daily output will actually decline. According to the capacity changes, the domestic operating capacity of aluminium may recover to around 40.19 million mt at the end of March, and output in March (31 days) is expected to increase 2.2% YoY to 3.39 million mt.

On the demand side, in February, domestic downstream demand recovered, hence the new orders and monthly output of aluminium producers improved on the month. Although export orders failed to exceed the level of the same period last year, the overseas demand was better than the fourth quarter in 2022. However, the domestic aluminium social inventory still increased seasonally. In light of the increasing domestic output from January to February, the social inventory of aluminium ingots increased significantly by 280,000 mt in February. With the continuous recovery of downstream demand, the social inventory of aluminium may usher in an inflection point. It is expected that the domestic social inventory may drop to around 1.15 million mt by the end of March.

Alumina

China’s metallurgical-grade alumina output in February (28 calendar days) was 6.12 million mt, down 3.9% MoM but up 16.1% YoY, according to SMM statistics. The average daily output increased 13,000 mt to 219,000 mt. As of the end of February, the domestic installed alumina capacity stood at 97.75 million mt while the operating capacity was 79.14 million mt, implying an average domestic operating rate of 80.9%. On the whole, it is estimated that the net imports of alumina in January will be 110,000 mt, suggesting a slight shortage of 300,000 mt in the month.

The average operating rate of alumina producers and average daily output of alumina in February both increased compared with January, but the total output was lower than last month due to fewer working days in February. The year-on-year output increase is owing to the sharp output decline in February last year caused by unreleased new capacity of Hebei Wenfeng and Chongqing Bosai, the heating season in north China, strict environmental protection policy during the Winter Olympics, and the pandemic outbreak in Guangxi.

In terms of regions, the output in Guizhou and Hebei increased MoM while that of other regions decreased slightly due to fewer natural days. In Henan, the local alumina plants maintained production cuts, and thus the average operating rate of the province was only 54.2%. In the same period last year, under the strong pressure of strict environmental protection policies, poor profits and tight supply, the operating rate was 55.8%. These factors also affected the production in Shanxi where the operating rate was 70.7%; In Guizhou, the two alumina plants affected by power cuts have resumed, driving the operating rate in this province to recover from 73.2% to 89.4%. In Hebei, the monthly output increased 40,000 mt month-on-month. The total installed alumina capacity of Wenfeng alumina plant reached 3.6 million mt, and its current operating rate remained at a high level of 90.5%. In Guangxi and Shandong, the stable supply of raw materials and good profits encouraged local enterprises to produce stably, with an average operating rate of 98.1% and 95.6% respectively.

On the whole, aluminium output in Yunnan was reduced by 783,000 mt in February due to power cuts, and the time for resumption is still unknown. Under the strong pressure of supply surplus, alumina plants with high costs were unwilling to increase the production for the time being, and the ramp-up of new capacity also showed down. It is estimated that the daily output of alumina in March will remain at 210,000 mt, and the total domestic output of metallurgical-grade alumina in March (31 days) will be 6.51 million mt.

Primary lead

SMM data showed that China produced 281,400 mt of primary lead in February, down 1.37% MoM but up 18.27% YoY. For January-February, the combined output surged 10.47% from the same period last year. Production capacities of enterprises involved in the survey in 2023 totalled 5.77 million mt.

According to research, most primary lead smelters resumed the production in February after the Chinese New Year holiday. During this period, some lead smelters in Henan and Hunan carried out maintenance. Coupled with fewer working days in February, the output declined to a certain degree. At the same time, Henan Jinli's new production line was put into production and the maintenance of Hunan Shuikoushan and Guangdong Zhongjin Lingnan was completed, which led to a significant growth in output. On the whole, the output declined only slightly. Compared with the same period last year, the impact of Chinese New Year holiday subsided earlier in this February, hence the operating rates of lead smelters were higher than last year.

Looking forward to March, March has 31 calendar days and more production time will become the main force for output increase in March. At the same time, the new capacity of lead smelters in Henan continued to ramp up, and the production of enterprises such as Yunnan Zhenxing and Hunan Yinxing has resumed after maintenance. SMM expects China's primary lead output will rise more than 30,000 mt to 317,000 mt in March.

Secondary lead

SMM data showed that China produced 316,800 mt of secondary lead in February, up 2.23% MoM but down 1.09% YoY. For January-February, the combined output fell 6.24% from the same period last year to 626,700 mt. China produced 280,400 mt of secondary refined lead in February, up 1.82% MoM but down 0.47% YoY. For January-February, the combined output fell 9.15% YoY to 555,900 mt.

Domestic secondary refined lead output in February was in line with previous expectations, but it did not recover rapidly after the Chinese New Year as several large factories in Shandong, Hebei and Xinjiang either reduced or stopped the production due to technological upgrading and equipment failure. At the same time, many enterprises, including Zhejiang Tianneng, Guangxi Zhenyu, Anhui Chaowei, Tongliao Taiding, and Guangdong Xinyu, resumed the production in February, which brought about some output increases. However, the total output in February was generally stable, failing to recover rapidly as expected.

Entering March, most secondary refined lead smelters in Anhui have already operated at full capacity, and some smelters plan to increase the production to full production. But a smelter in Anhui has stopped production due to equipment failure, and it is estimated to complete the equipment in April. In addition, some enterprises that resumed production in mid and late-February will also gradually increase their production to full production. A smelter in Xinjiang will also run at full production. It is expected that more secondary refined lead smelters will increase production in March, which will bring significant increments.

Refined zinc

China's refined zinc output stood at 501,400 mt in February, down 9,800 mt or 1.91% MoM and up 43,000 mt or 9.39% YoY, which was basically in line with expectations. Fewer working days in February led to an output cut of about 30,700 mt.

In February, the domestic zinc concentrate TCs stood at 5,500 yuan/mt in metal content and the average TCs were 7,100 yuan/mt in metal content. The prices of zinc remained above 23,000 yuan/mt, hence the profits of zinc processing was 1,000-2,000 yuan/mt in metal content. Coupled with the soaring prices of domestic minor metals in February, the operating rates of domestic zinc smelters reached full capacity in light of high profits. In addition, the zinc smelters and secondary zinc smelters that were shut down for maintenance and during the Chinese New Year holiday resumed the production successively, bringing additional increments. In February, most smelters that carried out overhauls were based in Guangxi and Hunan.

SMM predicts that in March 2023, domestic refined zinc production will increase 59,000 mt MoM and 13% YoY to 560,400 mt. The output from January to March will reach 1.57 million mt, an increase of 6.87% year-on-year. Entering March, power cuts in Yunnan have affected the smelters in Qujing and Kunming. However, due to the fewer working days in February, the output decline will be limited. At present, due to production restriction, production of most smelters in Yunnan has been reduced by 10%-20%, except that the smelter of Honghe cut the output owing to routine maintenance. Meanwhile, the overproduction plan of domestic smelters and the resumption of secondary zinc smelters will bring about some extra increments. In addition, the maintenance plans of Huludao Zinc and Gansu Baohui have been postponed to April. Judging from the current production schedules, the excess zinc concentrate has been produced into ingots.

Refined nickel

The domestic refined nickel output in February increased 5.49% on the month and 33.9% on the year to 17,300 mt. Total refined nickel output increased in February in line with expectations as the new capacity of electrowinning nickel was fully released in February. In addition, the electrowinning nickel capacity of some enterprises was still in the expansion stage during February.

The domestic refined nickel output in March is expected to increase 1.16% on the month and 38.89% on the year to 17,500 mt. The domestic refined nickel output in March is expected to increase only slightly compared with that in February as most new production lines have already been fully put into production. Many companies still have expansion plans in the second quarter, and thus China's refined nickel output is expected to hit a new high in the second quarter.

Refined tin

Chinese refined tin output was 12,892 mt in February, up 7.52% MoM and 5.98% YoY. The total output from January to February dipped 3.39% on the year. Some smelters suffered raw material shortages.

In terms of regions, the output of smelters in Yunnan and Jiangxi dropped from the previous month. The tight raw material supply and low TCs squeezed the profit margins of smelters. The actual production of smelters in Yunnan and Jiangxi varied, and the output of smelters with higher production capacity declined more significantly. The equipment maintenance also affects the actual production in February and the output forecast in March. Other smelters maintained stable production. The production ramp-up of some smelters failed to make up for the output losses caused by production cuts of others.

In March, the tight raw material supply and the falling TCs may further suppress the profits of smelters. On the other hand, tin prices continued to fall, and the recovery of orders was slower than expected, resulting in a stronger wait-and-see sentiment among downstream sectors, thus the spot trading was slack. Some Chinese smelters have lowered their expected output, and some are about to end their maintenance. The refined tin output will grow MoM in March to 14,200 mt.

NPI

Chinese NPI output stood at 305,000 mt in physical content in February, up 8.56% MoM and 0.72% year-on-year. The total Ni content was 32,800 mt. In February, the downturn in the stainless steel sector resulted in a large accumulation of NPI stocks, which further greatly dragged down the NPI output in the month. The month-on-month increase was due to the production resumption of low-grade NPI plants. In detail, the output of high-grade NPI was about 26,100 mt in Ni content, down 5.19% from the previous month, which was contributed by the slower-than-expected commissioning of integrated stainless steel mills. At the same time, some NPI plants that did not overhaul before the Chinese New Year carried out maintenance in February, which reduced their cost pressures while alleviating market oversupply. In addition, some high-grade NPI plants saw declining output due to furnace problems. The low-grade NPI output ballooned 26.91% to 6,700 mt in Ni content as previous output was low when integrated enterprises carried out large-scale maintenance at the end of last year. In February, the production of 200-series stainless steel was still profitable, so the low-grade NPI output improved.

It is estimated the Chinese NPI output in March will increase 1.63% from January to around 33,400 mt in Ni content. In March, some high-grade NPI plants were still under maintenance, but the increase in working days in the month will slightly push up the output. On the other hand, stainless steel mills carry high in-plant inventories of NPI, which will limit the output growth of NPI in March.

Indonesia NPI

Indonesia NPI output stood at 105,100 mt in Ni content in February, up 3.96% month-on-month and 27.54% year-on-year. The year-to-date output amounted to 206,200 mt in Ni content. In February, two NPI production lines were newly built in Indonesia, while the commissioning of some production lines was delayed. The output of some new production lines that were constructed in January was not released as scheduled in February. With the improvement of the new energy sector, the companies were more active in switching the high-grade NPI-based production lines to produce high-grade nickel matte spurred by the higher profits of the latter. According to SMM research, the high-grade nickel ore supply in Indonesia has tightened recently, which will push up the NPI plants’ costs, but it has not affected the production of high-grade NPI so far. In addition, problems with power equipment in some industrial parks in Indonesia are expected to continue to affect the production pace of NPI in March. SMM believes that the Indonesia NPI output will reach 105,800 in Ni content in March.

Nickel sulphate

Chinese nickel sulphate output stood at 141,900 mt in physical content or 31,200 mt in metal content, up 0.06% on the month and 24.66% on the year. The main reasons for the small output increase are as follows. 1. Driven by the demand from the electrowinning nickel sector, the prices of nickel sulphate soared in February, with an average price of 39,373 yuan/mt. However, the recovery of demand from ternary precursor manufacturers did not meet expectations. The precursor companies could accept low purchase prices of nickel sulphate, and the market saw almost no transactions of small orders except for the delivery of long-term orders. 2. In February, the supply tightness of raw materials was not eased. The MHP processing fees dropped from 36,500 yuan/mt in metal content to 29,000 yuan/mt in metal content. The above factors caused some nickel sulphate enterprises to reduce their production. Some liquid nickel sulphate companies produced according to their orders in consideration of the warehousing capacity. In March, as the price difference between nickel sulphate and pure nickel continues to narrow, nickel sulphate prices are bound to drop compared with the previous month. At the same time, ternary precursor manufacturers will restock some nickel sulphate owing to the raw material consumption in the first two months. SMM believes that the nickel sulphate output will gain 12.30% MoM in March to 35,000 mt in metal content.

Battery-grade manganese sulphate

China produced 23,900 mt of high-purity manganese sulphate in February, up 70.71% MoM, which was contributed by the normal rebound of demand from ternary precursor companies after the Chinese New Year. According to SMM survey, terminal consumption of domestic NEV was slack in February, which greatly dragged down the power battery demand. Therefore, the output growth of mid and low-nickel precursors was limited. On the contrary, overseas demand was relatively stable, driving up Chinese high-nickel precursor output. The overall output of high-purity manganese sulphate rebounded sharply in February.

In March, due to the crashing lithium carbonate prices and the high in-plant inventories of finished products held by battery cell markers, most battery cell manufacturers hold a strong wait-and-see attitude and are cautious in production, which will slow down the production of precursor enterprises. As a result, the supply of high-purity manganese sulphate will not increase greatly. The output in March is expected to be around 24,200 mt in physical content, up 1.26% MoM.

Electrolytic manganese dioxide

Chinese electrolytic manganese dioxide (EMD) output was 14,500 mt (including 900 mt used in LMO battery, 8,000 mt used in alkaline manganese battery, and 5,600 mt for zinc-carbon battery) in February, up 33.03% MoM and down 61.94% YoY. EMD output in the first two months of 2023 stood at about 25,400 mt, down 66.71% YoY. The output of EMD used in zinc-carbon batteries and alkali manganese batteries rose more. On one hand, manganese salt plants gradually resumed operation after the Chinese New Year holiday. On the other hand, the downstream demand improved, boosting the companies’ production.

In March, due to the lower operating rates of LMO battery companies, the demand for EMD (used in LMO batteries) may decline further, and the output will fall slightly. The output of EMD used in zinc-carbon and alkali manganese batteries is expected to be stable with larger proportion. Therefore, the decline will be limited, and total EMD output will be about 14,300 mt.

Tricobalt tetraoxide (Mn3O4)

SMM data showed that in February 2023, Chinese tricobalt tetraoxide (Mn3O4) output was 13,900 mt (including 8,400 mt of electronics-grade Mn3O4 and 5,500 mt of battery-grade Mn3O4), up 15.9% MoM and 12.60% YoY. Mn3O4 output in the first two months of 2023 stood at about 25,800 mt, up 3.20% YoY. After the CNY holiday, the producers gradually resumed their operations.

The manganese salt factories hold varied opinions toward the production in March. At present, they are less willing to cut production because of acceptable profit margins. In addition, it was learned that some enterprises may increase their output for long-term contract delivery. It is estimated that the Mn3O4 output in China will be about 14,500 mt in March.

High-carbon ferrochrome

Chinese high-carbon ferrochrome output stood at 545,500 mt in February, up 51,500 mt or 10.43% from the previous month and 46,200 mt or 9.25% on the year. The output in Inner Mongolia was 318,400 mt, up 7,900 mt or 2.54% MoM, and that in Guizhou stood at 33,800 mt, up 104.85% MoM. Some ferrochrome plants suffered losses from the high chrome ore prices and the off-season. However, most were enthusiastic about production amid the further rise in bid price offered by mainstream stainless steel mills in the month and the expected strong recovery of consumption. Plants in north China maintained high operating rates, and those in the south which carried low-priced raw material stocks also ramped up production amid the growing profits.

In March, the output of high-carbon ferrochrome is expected to rise to 569,300 mt. The market has heard frequent production reduction plans from stainless steel mills owing to the slower-than-expected recovery of consumption, but the output still stands at a high level, and the ferrochrome demand is growing. Besides, the bid price of ferrochrome in March increases, which will push up the manufacturers’ profit margins and keep the output at high levels.

Stainless steel

According to SMM survey, Chinese stainless steel output totalled 2.83 million mt in February, up 21.58% MoM and 21.37% YoY. Specifically, the output of 200-series stainless steel added 35.53% from the previous month to 904,000 mt, that of the 300-series gained 16.94% to 1.47 million mt, and that of the 400-series stood at 450,400 mt, up 12.91% MoM.

In February, stainless steel mills that had arranged year-end maintenance in January resumed normal production. The production of the 200-series increased greatly owing to the better profits, while that of 300 and 400-series stainless steel resumed to the previous situation.

In March, the stainless steel output may rise slightly. The mainstream 200-series stainless steel mills may produce cautiously, whose output will not grow sharply. In terms of 300-series, a large stainless steel mill carried out an overhaul due to equipment failure, which has a limited impact on the output. Besides, some stainless steel mills, including some state-owned ones, may increase their production to a certain extent. Therefore, the output of 300-series stainless steel in China will grow slightly. In addition, Indonesia also has a certain plan to ramp up stainless steel production. In March, the operating rates of 400-series stainless steel mills will be maintained at the current level, and the output will not grow sharply. The high stainless steel inventory will still curb the prices from a further rise. It is necessary to pay attention to the costs of raw materials and the recovery of terminal demand. To sum up, SMM believes that the prices of stainless steel may fall in March.

EMM

Chinese EMM output stood at 100,300 mt in February, down 1.48% on the month and up 1,014.84% on the year, SMM data showed. EMM output in the first two months of 2023 stood at around 202,200 mt, up 819.09% year-on-year. The main reasons for the decline in output in February are as follows. 1. There are fewer working days in February. Large EMM plants lowered their operating rates in the month. 2. Some plants delayed production resumption after the CNY, and the overall daily output did not stabilise until mid-to-late February.

In March, although the terminal demand has not improved significantly, most EMM plants now keep their average daily output at about 4,000 mt. The EMM output throughout March is expected to be around 115,200 mt.

Polysilicon

According to SMM statistics, Chinese polysilicon output was about 101,200 mt in February, down 1.6% from January. The monthly output finally dropped after a continuous increase of six months.

The reasons for the MoM decline are as follows. 1. A leading producer carried out maintenance in February, and its output dropped about 1,000-2,000 mt. 2. There are fewer production days in February. The average daily polysilicon output in January was about 3,300 mt, while that in February grew to about 3,600 mt. In addition, factors such as the COVID-19 outbreak in the early stage and the CNY break postponed the commissioning of some production lines in the first quarter of 2023, and thus almost no new production capacity was added in January and February.

Industrial silicon metal

SMM data shows that China's industrial silicon metal output was 281,000 mt in February, an increase of 7,000 mt or 2.64% month on month and 17.1% year on year.

Although calendar days in February is 3 days fewer than in January, the domestic total output rose month-on-month in February. The output growth was mainly contributed by silicon companies in Xinjiang and Inner Mongolia. According to SMM data, by the end of 2022, 400,000 mt of new industrial silicon production capacity in Xinjiang was built, which was commissioned after CNY holidays. This, together with high operating rates at other silicon companies in the region, increased local output by 3,000-6,000 mt in February, driving the domestic output to rise. Output in Yunnan, Sichuan, Hunan and other places in south China decreased slightly, as the producers lacked motivation to resume production amid low silicon prices.

In March, the supply of industrial silicon will remain strong in the north and weak in the south. The output in Xinjiang and Inner Mongolia is expected to continue to increase driven by new production capacity. Emerging silicon companies such as Hexi Silicon and Hongdian Ferroalloy in Gansu and Qinghai will also ratchet up their output to a certain extent. In Sichuan, the operating rates remained low as the low-water period has bolstered costs. The silicon enterprises in Nujiang and Yunnan have been affected by substation maintenance, and the affected output is estimated at 3,000 mt. Some silicon enterprises in Dehong Prefecture have plans to shut down their furnaces for maintenance. In general, domestic industrial silicon supply in March will increase to around 310,000-320,000 mt in view of more calendar days in March than in February.

Photovoltaic

According to SMM statistics, domestic photovoltaic module output in February was about 30.64 GW, up 5.29% from the previous month. Some module companies produced actively for order delivery due in February, leading to the output growth. In addition, the recovery of demand also provided some support for module output due to bid solicitations by end-users after CNY holidays. The fewer calendar days in February had a negative impact on production, though. In March, as the number of calendar day increases and end-users continue to enter the market, module output is expected to reach around 35 GW.

Silicon-manganese alloy

China produced 937,400 mt of silicon-manganese alloy in February, up 0.25% MoM and 2.55% YoY, according to SMM statistics. From January to February 2023, the silicon-manganese alloy output in China was 1.87 million mt, an increase of 4.54% year-on-year. According to SMM survey, the main reason for the output growth is that the silicon-manganese manufacturers in south China that had shut down before CNY holidays resumed production, raising operating rates. Operating rate in north China remained high thanks to healthy profit. In addition, some of the furnaces restarted operations after maintenance in February. However, considering that the actual number of days in February has decreased compared with January, the national production of silicon-manganese increased only slightly compared with January.

Entering March, the electricity tariff in Guangxi was raised, the resultant high cost of silicon-manganese and actual demand having not improved suppressed the production enthusiasm of the producers. Some plants have halted production in March, and some are also expected to cut or suspend production in the near term. Power shortages in Xingyi, Guizhou province, driven by local power grid issues, have also affected production. The output of alloy is projected to fall to around 921,700 mt in March.

Magnesium ingot

China's magnesium ingot output stood at 69,000 mt in February, up 7.5% MoM but down 17% YoY, according to SMM statistics. The output totalled 133,000 mt in January-February 2023, a year-on-year decrease of 19.7%.

With the returning of migrant workers to their workplace after CNY holidays, operating rates at magnesium plants rose compared to January. However, the performance of the downstream market after the holidays fell short of market expectations. This, coupled with lower magnesium prices, resulted in great cost pressure on magnesium factories in Shanxi. And some alloy enterprises reduced the proportion of primary magnesium production. The head of a large magnesium factory said that the current downstream environment is poor, and the actual market demand has dropped by 20-30% compared with the same period last year. Should downstream demand remain sluggish, the magnesium ingot will not rule out cutting output to tackle ample supply. The output at magnesium plants is expected to fall in March to some 66,000 mt. SMM will continue to pay attention to the changes in production in the main producing areas.

Magnesium alloy

China's magnesium alloy output stood at 26,000 mt in February, down 5.3% MoM but up 10.6% YoY, according to SMM statistics. Alloy output totalled 53,000 mt in January-February 2023, a year-on-year increase of 16.86%.

According to domestic magnesium alloy enterprises, affected by the drop in the price of magnesium ingots, some alloy plants using magnesium ingots lacked production enthusiasm. Downstream demand still remains poor, as reflected in the sluggish orders after CNY holidays. As such, alloy output should remain low in March and stand at around 26,500 mt.

Magnesium powder

China's magnesium powder output stood at 6,000 mt in February, up 4.1% MoM. YTD output as the end of February totalled 12,000 mt.

In February, operating rates at domestic magnesium powder enterprises remained at a low level, and the sluggish end-user market triggered pessimism among magnesium powder enterprises. The head of a large magnesium powder company said that after CNY holidays, the market demand has shrunk by nearly 40% compared with the same period last year. The decline in overseas demand was particularly significant. The magnesium powder market is poised to remain subdued in the near term unless domestic demand improves. China’s magnesium powder in March is estimated at around 6,000 mt.

PrNd oxide

Domestic output of PrNd oxide in February 2023 stood at 5,767 mt, up 2.6% MoM. Output increased across Guangxi, Sichuan, Jiangxi and Jiangsu to varying degrees.

According to SMM survey, due to the continuous decline in the prices of PrNd oxide, metal factories were also more cautious in purchasing. And the actual transaction of separation plants and waste recycling companies was also dim. Some manufacturers shuttered in January for CNY, and the output was low. Most of them fully resumed normal production in February. The output in Guangxi increased by 20% month-on-month; the output in Jiangsu and Jiangxi both increased by about 10% month-on-month. With the continuous development of the rare earth end-user industries and the recovery of orders from downstream magnetic material companies, SMM expects that the output of PrNd oxide will continue to increase in March.

PrNd alloy

Domestic output of PrNd alloy in February 2023 stood at 5,244 mt, up 0.4% MoM. Sichuan accounted for most of the output growth, while the output in Jiangsu decreased slightly. Output in other regions changed little compared with January.

In February, the prices of PrNd alloy remained on the downswing. After the CNY holiday, the orders of downstream magnetic material enterprises remained sluggish. Most of them mainly worked through existing inventories. However, considering that the reduction and shutdown of production will cause great losses to metal manufacturers, metal factories mostly maintained normal production despite the weak market. Some manufacturers even reported output growth. The output in Sichuan grew by 7.5% month on month. SMM predicts that the output of PrNd alloy may continue to increase slightly in March 2023.

Molybdenum concentrate

In February 2023, China’s molybdenum concentrate output was 16,000 mt, a rise of 4% MoM.

Due to the weakening impact from maintenance and shutdown during the CNY holiday, the mines in south China and private mines started to resume production in February, which has brought about a small increase in the output of molybdenum concentrate. Some mines that resumed production late have not reached full production due to fewer calendar days in February, and there is still room for a certain increase in output.

In March, the price of molybdenum concentrates in the market remains at a high level, so the production enthusiasm of mines is generally strong. Absent external factors such as environmental protection, it is expected that molybdenum mining enterprises will run at full capacity in March, growing output of molybdenum concentrate.

Ferro-molybdenum

In February 2023, China’s ferro-molybdenum output was 17,100 mt, a growth of 6% MoM.

The increase in ferro-molybdenum production in February was mainly attributable to two factors. First, ferro-molybdenum smelters gradually resumed production and increased operating rates after CNY holidays. Second, ferro-molybdenum orders placed before CNY needed to be delivered in February, driving smelters to produce actively.

Entering March, new orders in the market are limited since the bid solicitation volume of ferro-molybdenum by steel mills hit a new low last month. Moreover, high cost of molybdenum concentrate and steel mills pushing for lower bid prices have put some smelters at risk of incurring losses, and they plan to cut output. As such, the output of ferro-molybdenum will decrease to a certain extent in March.

Silver

According to SMM survey, domestic #1 silver output stood at 1,293.80 mt (silver output produced with ore stood at 1,163.80 mt) in February 2023, up 2.6% on the month and 17% year on year. The significant year-on-year growth is because producers halted production for CNY holidays in February 2022, while the 2023 CNY holiday came earlier in January. Therefore, silver producers suspended production in January for CNY holidays and maintained production after CNY holidays through the remaining of the month. Besides, some plants suspended production for maintenance, and resumed production in February. The output at some plants declined in February due to fewer calendar days and production schedules. SMM expects the output to rise slightly in March.

On the macro side, the number of initial jobless claims in the United States for the week ending February 24 was 190,000, lower than the previous reading of 192,000, and the expected figure of 195,000. According to Federal Reserve Chairman Powell’s speech on March 7 US time, the latest economic data topped expectations, and the Fed may raise interest rates in the future more than previously expected. If the overall data show that the pace of tightening needs to be accelerated, the Fed will accelerate the pace of interest rate hikes in the future, having a negative impact on the market.

Antimony ingot

According to SMM survey, China’s antimony ingot output (including antimony ingot, crude antimony, antimony cathode, etc.) in February fell sharply by 7.68% MoM to 5,820 mt, the lowest in recent years. On the whole, antimony raw material resources remained tight in February. Despite antimony ore auctions by Russian Polyus in February, large inflows of Russian antimony ore into the domestic market are unlikely to materialise in the short term. Meanwhile, there has also been issues with Tajikistan’s raw material supply, and frequent war in southern Myanmar is affecting the exploiting of antimony ore. In this scenario, domestic and overseas antimony ore resources cannot increase noticeably in the short term. The price of antimony products has recently reached a plateau. But inventories of antimony ingots in Lengjiang city have dropped to what market participants said was a record low of around 2,000 mt. Therefore, from the current fundamentals, there is still a strong support for the upside trend of antimony prices.

In terms of production details of individual manufacturer, among the 33 respondents in SMM survey, 15 manufacturers suspended the production, one more than the previous month; 14 reduced their production, up by one; and 4 maintained normal production, one fewer than in January. SMM predicts that the supply-demand structure of the domestic antimony market in March 2023 will not be overturned under the current economic situation. China’s antimony ingot output in March is anticipated to decline on a monthly basis.

Refined bismuth

According to SMM survey, the output of refined bismuth in China was 2,419 mt in February, up 15.86% MoM. On the one hand, refined bismuth production recovered after being disrupted by the Chinese New Year (CNY) holiday. On the other hand, many refined bismuth producers were still plagued by raw material shortages, preventing their operating rates from picking up significantly. Bismuth concentrates were still in shortfalls, and there was only a small amount of bismuth-containing scrap from the lead industry that was available in the market. Rising refined bismuth prices left bismuth raw material suppliers more willing to sell, though. SMM surveyed 24 refined bismuth producers in February. Although two more producers were shut down than in January and two producers reported sharp declines in their output, significant output increase at six other producers allowed the overall production to rise in February.

It is expected that refined bismuth prices will still have upside room in March. In view of tight raw material supply, SMM predicts that the domestic refined bismuth production will change little in March.

Silver nitrate

The domestic silver nitrate plants with sales qualification together produced 614 mt of silver nitrate in February, up 14.8% MoM. The total output of silver nitrate nationwide reached 646 mt. Silver nitrate plants worked against the clock after the CNY break in order to deliver their backlog orders received before the holiday. The entry of new players also contributed to the output growth.

Silver nitrate market has stabilised in early March. SMM expects that the output of silver nitrate will drop slightly in March as the market digests the overbooked orders in February.

Titanium dioxide

SMM data showed that China's titanium dioxide output stood at 327,000 mt in February, up 8.9% MoM and 3.42% YoY. The output totalled 628,000 mt in the first two months of this year, down 1.4% YoY.

As the weather got warmer, the production of end-users picked up and the construction industry also recovered, boosting the demand for titanium dioxide and enabling titanium dioxide producers to hike their prices twice in February. Hence, titanium dioxide producers were keen on stepping up their production.

SMM predicts that the domestic titanium dioxide output will climb further to 340,000 mt in March, driven by policy support and recovering infrastructure sector.

APT

The APT output in China stood at 11,000 mt in February, up 38% on a monthly basis, which was basically in line with market expectations.

APT smelters resumed their production after the CNY holiday. Some smelters were operating at full capacity as government efforts to boost consumption kept them optimistic about the tungsten market and prices.

Entering March, although smelters were optimistic about the tungsten market, the increase in downstream orders fell short of expectations. APT output is expected to stabilise in March as smelters are under cost pressure.

Lithium carbonate

China’s lithium carbonate output stood at 30,802 mt in February, down 14% MoM, but up 66% YoY. Some spodumene and lepidolite-based smelters ramped up their production after the weather warmed up. However, extended maintenance by large spodumene-based smelters and production disruptions to some lepidolite-based smelters due to environmental protection checks in late February, coupled with dismal recycling market, caused lithium carbonate output to drop on a MoM basis.

While some lepidolite-based smelters in Jiangxi will remain under maintenance, the capacity ramp-up by spodumene and salt lake-based smelters is expected to allow the domestic lithium carbonate output to recover to 35,058 mt in March, up 14% MoM and 34% YoY.

Lithium hydroxide

China’s lithium hydroxide output stood at 24,371 mt in February, up 15% MoM and 92% YoY. From the perspective of smelting, although some large smelters reduced their production further due to insufficient supply of ore, the capacity ramp-up of new projects and production recovery after maintenance pushed up the overall output. From the perspective of causticisation, causticisation plants were keen on purchasing lithium carbonate to produce lithium hydroxide due to the big price difference between the two and strong demand.

With smelting and causticising activities both increasing, SMM estimates that the domestic lithium hydroxide output will reach 27,112 mt in March, up 11% MoM and 54% YoY.

Cobalt sulphate

China’s cobalt sulphate output stood at 7,336 mt in cobalt content in February, up 16% MoM and 8% YoY. The increase was driven by improving demand and fading impact from the CNY holiday. On the demand side, the output of precursors rebounded from a low level, but the overall increase was limited. The production of large-scale integrated precursor plants recovered only slightly. Traders stocked up after cobalt sulphate prices fell to a low level. The performance of digital electronics market remained poor.

SMM predicts that China’s cobalt sulphate output will rise 10% MoM and 7% YoY to 8,034 mt in cobalt content in March alongside recovering downstream demand.

Tricobalt tetraoxide (Co3O4)

The output of Co3O4 in China stood at 3,808 mt in February, up 7% MoM, but down 48% YoY. Co3O4 production gradually recovered after the CNY holiday. The production of a top-tier Co3O4 producer was still constrained in February, and will not recover until March. On the demand side, sluggish digital electronics market and unstable lithium carbonate prices kept LCO producers cautious about raw material procurement.

A large Co3O4 producer will resume production in March, while others will maintain stable production or cut their output slightly. The domestic Co3O4 output is estimated to total 4,205 mt in March, up 10% MoM, but down 34% YoY.

PCAM

Domestic PCAM (precursor of cathode active materials) output stood at 66,056 mt in February, up 13% MoM and 11% YoY. The recovery of domestic end-user demand has not yet been fully transmitted to the precursor market. Ternary cathode material producers maintained destocking strategy. Some precursor plants resumed production after maintenance and the CNY holiday. Precursor exports picked up thanks to recovering overseas demand.

Driven by recovering domestic and overseas demand, the domestic PCAM output is projected to rise 10% MoM and 14% YoY to 72,832 mt in March.

Ternary cathode material

The domestic ternary cathode material output stood at 49,170 mt in February, up 21% MoM and 13% YoY. Most ternary cathode material factories resumed their production after the CNY holiday. Downstream battery cell makers restocked and some stepped up purchases due to growing overseas orders, also contributing to higher ternary cathode material output.

In March, the domestic demand will recover slowly, while demand from overseas NEV market will continue to improve. SMM estimates China’s ternary cathode material output at 56,259 mt in March, up 14% MoM and 13% YoY.

Iron phosphate

China produced 69,490 mt of iron phosphate in February, an increase of 12% month-on-month and 109% year-on-year. The operating rates of iron phosphate enterprises continued to rise last month, and new capacity also ramped up. Iron phosphate shipments increased amid slightly recovering downstream demand. Iron phosphate producers reported inventory backlogs as the increase in production outpaced that of demand. In terms of raw materials, phosphoric acid prices fell initially and then rebounded slightly in February, while phosphate rock prices stayed at high, leaving iron phosphate costs relatively stable.

As the market continues to recover, China’s iron phosphate output is forecast to increase 12% month-on-month and 132% year-on-year to 77,857 mt in March.

LFP

China produced 71,474 mt of LFP in February, an increase of 11% month-on-month and 34% year-on-year. LFP production recovered in February after a drastic decline in January. Demand from power battery market recovered slowly, while demand from energy storage sector was relatively strong. The finished product inventory of LFP enterprises was relatively high amid limited new orders. As the prices of lithium carbonate kept falling in February, LFP companies were cautious about purchasing. The prices of iron phosphate were temporarily stable. Thus, the overall costs of LFP enterprises declined.

China’s LFP output is forecast to rise 15% month on month and 32% year on year to 81,839 mt in March as end-user demand is expected to continue to recover.

LCO

China’s LCO output stood at 4,372 mt in February, up 39% MoM, but down 34% YoY. On the supply side, the output of top-tier LCO plants recovered in February, but was significantly below that in the same period last year due to poor demand from the digital electronics market. LCO plants maintained low operating rates amid rapidly falling lithium carbonate prices and slack demand. On the demand side, the mobile phone market remained sluggish. Although new mobile phone products were launched, new orders from battery cell makers were few as they were working through raw material stocks. The market demand for laptops and tablet computers was still weak. The operating rates of electronic cigarette industry recovered slightly after the CNY holiday, encouraging some LCO enterprises to increase their production of related LCO.

The production schedules of LCO companies will increase in March, but dismal digital electronics market will constrain the upside room. SMM predicts that the domestic LCO output will stand at 4,888 mt in March, up 12% MoM, but down 30% YoY.

LMO

China’s LMO output stood at 5,397 mt in February, up 107% MoM and 31% YoY. On the supply side, most LMO enterprises resumed their production after the CNY holiday. In particular, the operating rates of top-tier LMO enterprises reached 90%. On the demand side, battery cell makers were cautious about purchasing LMO amid the downward trend of lithium carbonate prices.

Considering that lithium carbonate prices remain in a downward path in March, battery cell makers will continue to push for lower LMO prices. Some loss-making LMO enterprises may be forced to halt their production. SMM predicts that the domestic LMO output will total 5,093 mt in March, down 6% MoM and 11% YoY.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)