SHANGHAI, Feb 3 (SMM) - This is a roundup of China's metals weekly inventory as of February 3.

SMM Aluminium Ingot and Billet Social Inventory Kept Accumulating

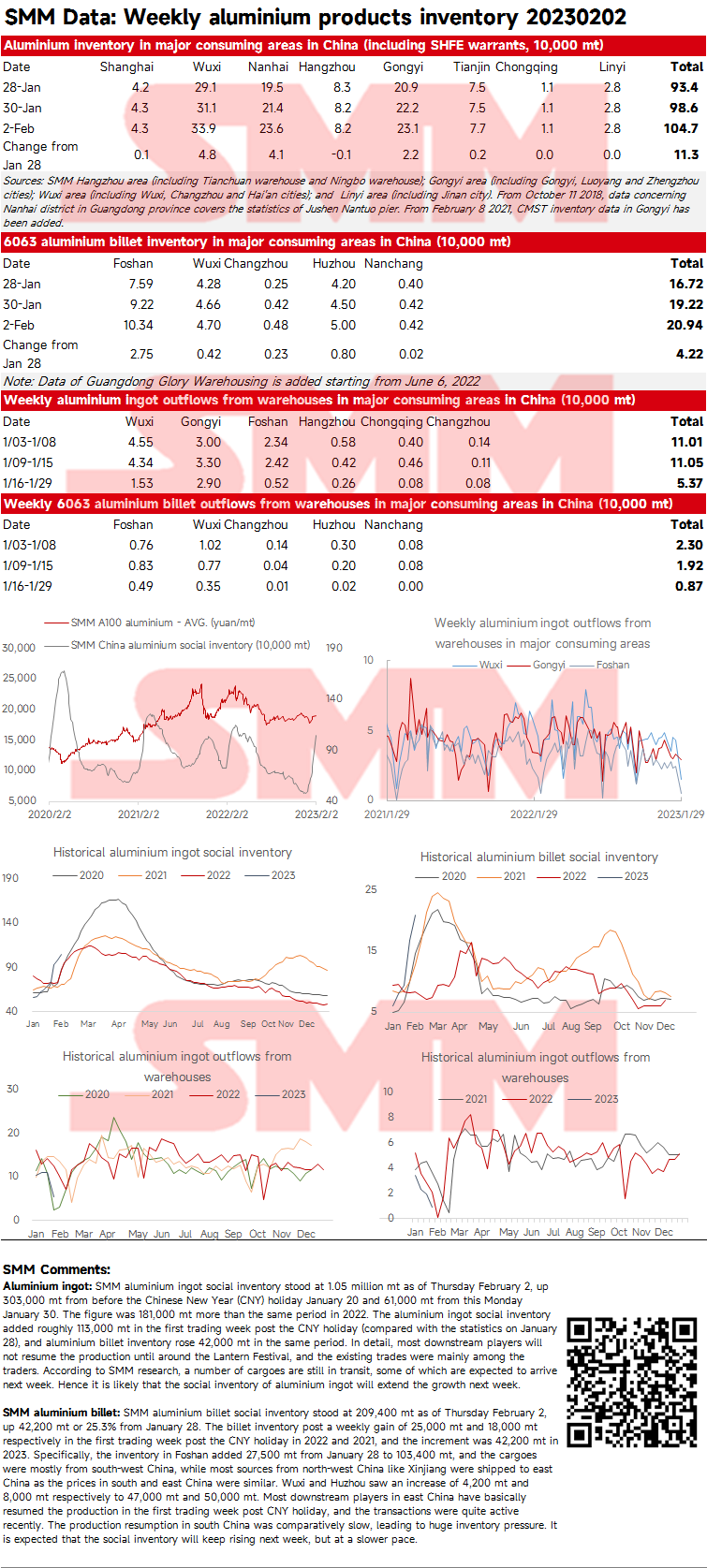

Aluminium ingot: SMM aluminium ingot social inventory stood at 1.05 million mt as of Thursday February 2, up 303,000 mt from before the Chinese New Year (CNY) holiday January 20 and 61,000 mt from this Monday January 30. The figure was 181,000 mt more than the same period in 2022. The aluminium ingot social inventory added roughly 113,000 mt in the first trading week post the CNY holiday (compared with the statistics on January 28), and aluminium billet inventory rose 42,000 mt in the same period. In detail, most downstream players will not resume the production until around the Lantern Festival, and the existing trades were mainly among the traders. According to SMM research, a number of cargoes are still in transit, some of which are expected to arrive next week. Hence it is likely that the social inventory of aluminium ingot will extend the growth next week.

SMM aluminium billet: SMM aluminium billet social inventory stood at 209,400 mt as of Thursday February 2, up 42,200 mt or 25.3% from January 28. The billet inventory post a weekly gain of 25,000 mt and 18,000 mt respectively in the first trading week post the CNY holiday in 2022 and 2021, and the increment was 42,200 mt in 2023. Specifically, the inventory in Foshan added 27,500 mt from January 28 to 103,400 mt, and the cargoes were mostly from south-west China, while most sources from north-west China like Xinjiang were shipped to east China as the prices in south and east China were similar. Wuxi and Huzhou saw an increase of 4,200 mt and 8,000 mt respectively to 47,000 mt and 50,000 mt. Most downstream players in east China have basically resumed the production in the first trading week post CNY holiday, and the transactions were quite active recently. The production resumption in south China was comparatively slow, leading to huge inventory pressure. It is expected that the social inventory will keep rising next week, but at a slower pace.

Zinc Ingot Social Inventory Up 16,200 mt from Monday

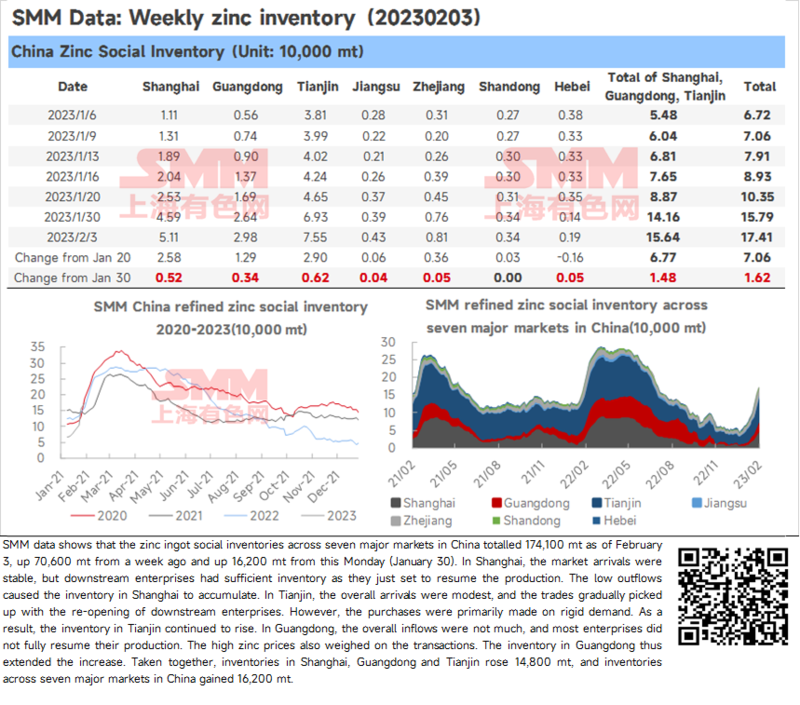

SMM data shows that the zinc ingot social inventories across seven major markets in China totalled 174,100 mt as of February 3, up 70,600 mt from a week ago and up 16,200 mt from this Monday (January 30).

In Shanghai, the market arrivals were stable, but downstream enterprises had sufficient inventory as they just set to resume the production. The low outflows caused the inventory in Shanghai to accumulate. In Tianjin, the overall arrivals were modest, and the trades gradually picked up with the re-opening of downstream enterprises. However, the purchases were primarily made on rigid demand. As a result, the inventory in Tianjin continued to rise. In Guangdong, the overall inflows were not much, and most enterprises did not fully resume their production. The high zinc prices also weighed on the transactions. The inventory in Guangdong thus extended the increase.

Taken together, inventories in Shanghai, Guangdong and Tianjin rose 14,800 mt, and inventories across seven major markets in China gained 16,200 mt.

Social Inventory of Lead Ingots Declines amid Downstream Restocking Demand

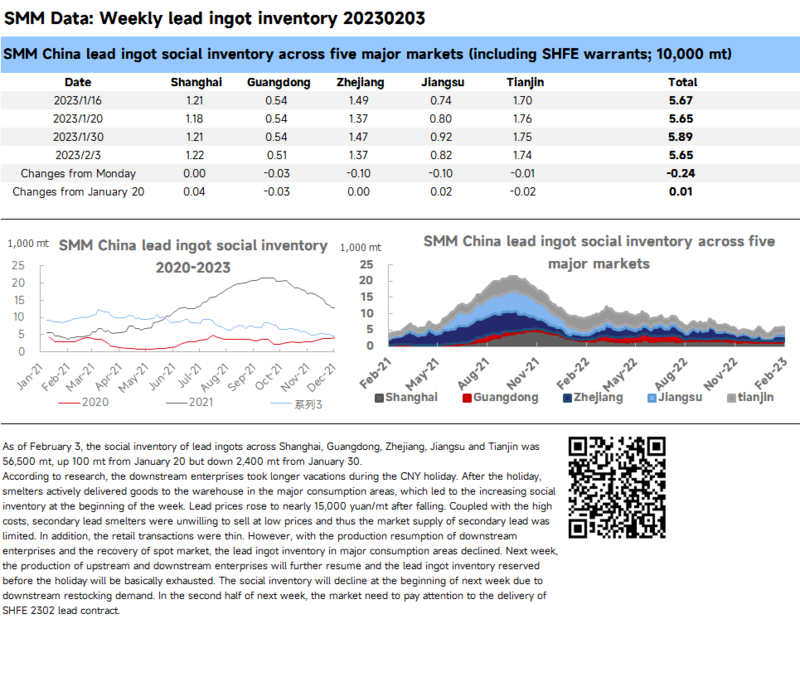

As of February 3, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 56,500 mt, up 100 mt from January 20 but down 2,400 mt from January 30.

According to research, the downstream enterprises took longer vacations during the CNY holiday. After the holiday, smelters actively delivered goods to the warehouse in the major consumption areas, which led to the increasing social inventory at the beginning of the week. Lead prices rose to nearly 15,000 yuan/mt after falling. Coupled with the high costs, secondary lead smelters were unwilling to sell at low prices and thus the market supply of secondary lead was limited. In addition, the retail transactions were thin. However, with the production resumption of downstream enterprises and the recovery of spot market, the lead ingot inventory in major consumption areas declined. Next week, the production of upstream and downstream enterprises will further resume and the lead ingot inventory reserved before the holiday will be basically exhausted. The social inventory will decline at the beginning of next week due to downstream restocking demand. In the second half of next week, the market need to pay attention to the delivery of SHFE 2302 lead contract.

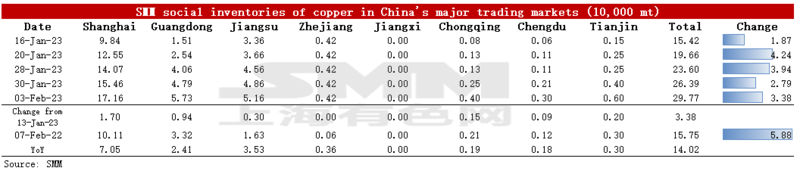

Copper Inventory in Major Chinese Markets Increased 33,800 mt

As of Friday February 3, copper stocks in mainstream markets increased by 33,800 mt from Monday to 297,700 mt, and grew by 61,700 mt from Saturday January 28. The inventories increased 101,100 mt from pre-CNY holidays levels and were 86,600 mt above the same period last year. Since the end of December, the domestic copper inventory has increased for six consecutive weeks. The growth is mainly attributable to more shipments from smelters around CNY holidays and inactive downstream purchases. The inventory has increased across China with the total inventory 140,200 mt higher than the 157,500 mt in the same period last year. The inventory was 70,500 mt higher than the same period last year in Shanghai, 24,100 mt higher in Guangdong, and 35,300 mt higher in Jiangsu. The inventory in Zhejiang exceeded the same period last year by 3,600 mt, and that in Tianjin was 3,000 mt higher than the same period last year.

Specifically, the inventory in Shanghai increased by 17,000 mt from Monday to 171,600 mt, and the inventory in Jiangsu increased by 3,000 mt to 51,600 mt. Shipments arrivals of imported cargoes were limited this week, and the stock accumulation was mainly driven by higher shipments from smelters. The smelters in north China delivered cargoes aggressively to east China before delivery of the SHFE front-month copper contract, which is the main cause of the inventory growth in east China. Inventory in Guangdong increased by 9,400 mt to 57,300 mt. The slower downstream replenishment after CNY holidays has resulted in a big growth in inventory, which is reflected in the recent slow growth in the daily average shipments from Guangdong. Overall, the domestic market is in oversupply.

Domestic smelters will contribute to most of the arriving shipments next week as the imports of seaborne cargoes will be limited. Big discounts will fuel the deliveries by smelters. Downstream consumption is expected to gradually recover next week. On the whole, both supply and consumption will pick up next week, and the stock accumulation will be slower than this week.

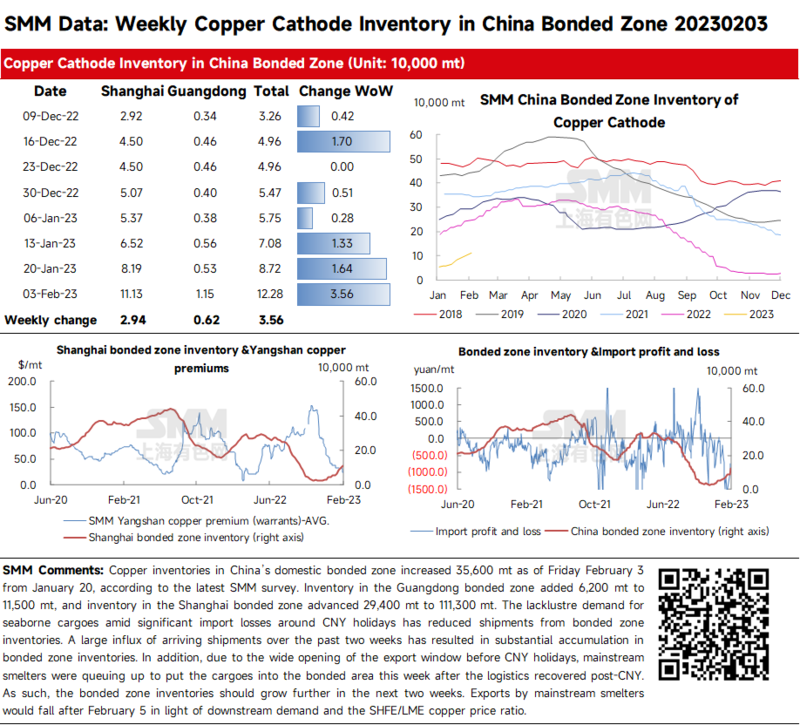

Copper Inventory in China Bonded Zone Grew 35,600 mt from Pre-CNY Level

Copper inventories in China’s domestic bonded zone increased 35,600 mt as of Friday February 3 from January 20, according to the latest SMM survey. Inventory in the Guangdong bonded zone added 6,200 mt to 11,500 mt, and inventory in the Shanghai bonded zone advanced 29,400 mt to 111,300 mt.

The lacklustre demand for seaborne cargoes amid significant import losses around CNY holidays has reduced shipments from bonded zone inventories. A large influx of arriving shipments over the past two weeks has resulted in substantial accumulation in bonded zone inventories. In addition, due to the wide opening of the export window before CNY holidays, mainstream smelters were queuing up to put the cargoes into the bonded area this week after the logistics recovered post-CNY. As such, the bonded zone inventories should grow further in the next two weeks. Exports by mainstream smelters would fall after February 5 in light of downstream demand and the SHFE/LME copper price ratio.

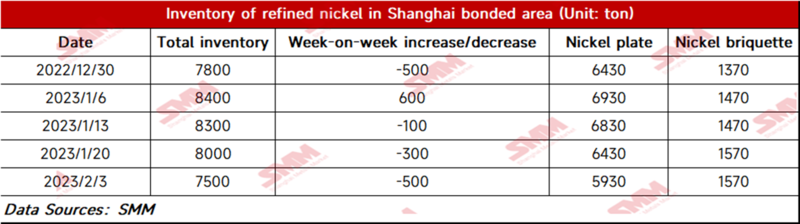

Bonded Zone Inventory of Nickel Drops Slightly from January 20

As of February 3, bonded zone inventory of nickel fell to 7,500 mt, with the inventory of nickel briquettes and nickel plates of 1,570 mt and 5,930 mt respectively. Spot imports suffered losses again. And the import losses of NORNICKEL nickel stood at 5,000-8,000 yuan/mt this week. The inventory of nickel plates dropped slightly this week. The nickel briquette demand from the nickel sulphate producers continued to decrease since the prices were still high.

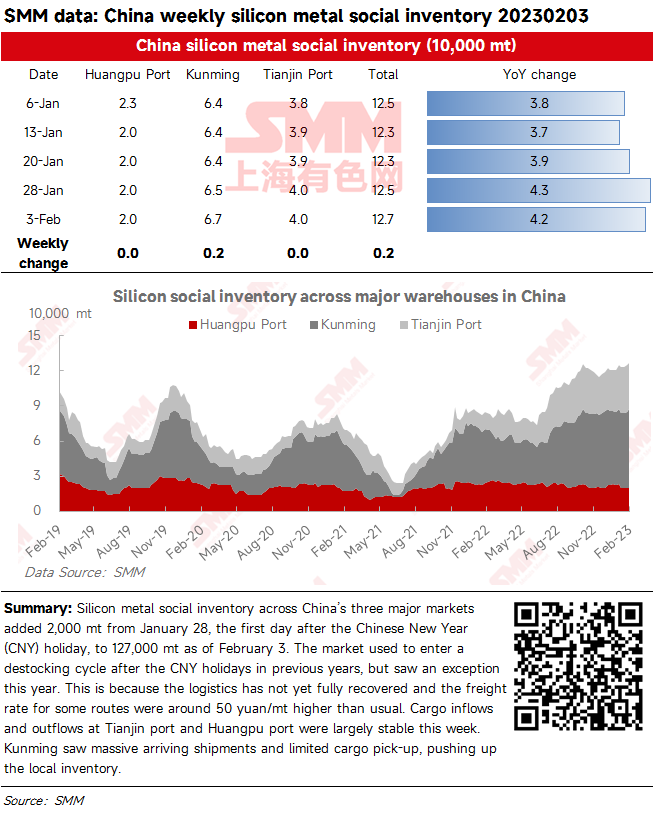

Silicon Metal Social Inventories across China’s Three Major Markets Extend Growth, Driven by Significant Arrivals in Kunming

Silicon metal social inventory across China’s three major markets added 2,000 mt from January 28, the first day after the Chinese New Year (CNY) holiday, to 127,000 mt as of February 3. The market used to enter a destocking cycle after the CNY holidays in previous years, but saw an exception this year. This is because the logistics has not yet fully recovered and the freight rate for some routes were around 50 yuan/mt higher than usual. Cargo inflows and outflows at Tianjin port and Huangpu port were largely stable this week. Kunming saw massive arriving shipments and limited cargo pick-up, pushing up the local inventory.

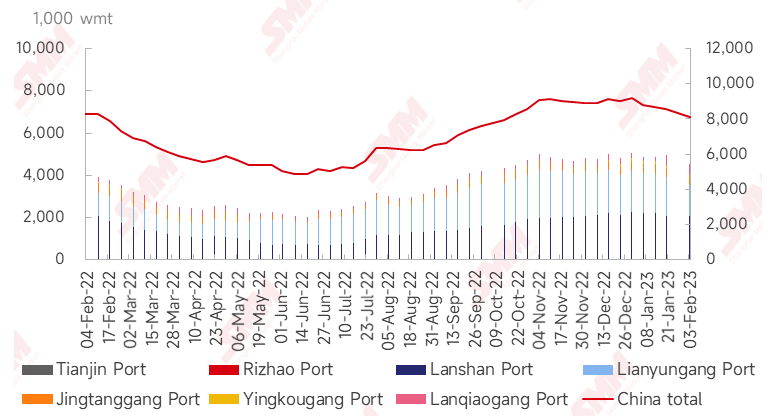

Port Inventories of Nickel Ore Dip 484,000 wmt from January 20

As of February 3, port inventories of nickel ore in China fell 484,000 wmt to 8.1 million wmt from January 20. The total Ni content dropped 4,000 mt to about 64,000 mt. The port inventory across seven major Chinese ports stood at 4.52 million wmt, down 424,000 wmt from January 20. The inventory at Lianyungang Port decreased the most. During the Chinese New Year holiday, nickel ore trading was slack. And ore shipments from the Philippines stood low owing to the rainy season in the country. On the demand side, NPI factories and steel mills maintained their production. In such a context, the nickel ore inventory dropped palpably. It is expected that the port inventory of nickel ore will maintain a downward trend.