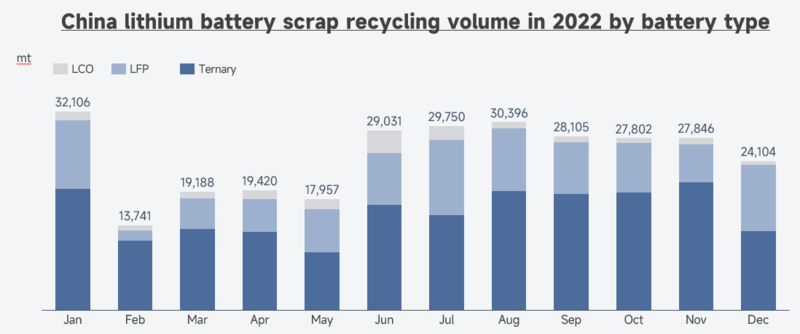

SHANGHAI, Jan 20 (SMM) - According to SMM survey, a total of 300,258 mt of lithium battery scrap was recycled in China in 2022 (including scrap in the form of battery, pole piece and black mass). Among them, 188,692 mt of ternary battery scrap was recycled, accounting for 63% of the total recycling volume, versus 94,551 mt or 31% for LFP battery scrap, and 17,015 mt or 6% for LCO battery scrap.

Driven by lucrative profits, ternary battery scrap was favoured the most last year. Most recyclers only had ternary battery scrap dismantling facilities and hydrometallurgy production lines, while their LFP battery scrap recycling facilities were still under construction. The demand for ternary battery scrap surged with the release of recycling capacity, leaving it in short supply.

Due to recycling capacity bottlenecks, LFP battery scrap was primarily recycled by lithium salt smelters who have recycling facilities. Since 2022, some lithium salt enterprises have accelerated the construction of LFP battery scrap recycling facilities, and some have been put into operation, boosting the demand for LFP battery scrap.

LCO battery scrap was less popular due to weaker-than-expected demand for cobalt and poor cost performance resulting from its higher content of more expensive cobalt. Some recyclers added a small amount of LCO battery scrap into their ternary battery scrap recycling facilities in order to improve the recovery of cobalt.

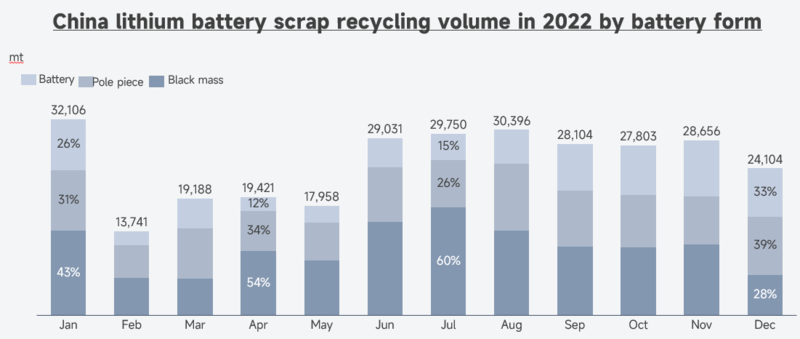

A total of 68,141 mt of lithium batteries (retired power lithium batteries and electronics batteries) were recycled, accounting for 23% of the total recycling volume; 99,024 mt of pole pieces (pole pieces generated during battery production process) were recycled, accounting for 33%; 133,093 mt of black mass (battery powder and pole piece powder) was recycled, accounting for 44%.

Battery scrap mainly includes retired ternary power batteries and LFP power batteries, as well as a small amount of electronics battery scrap. The wave of power battery retirement has not yet arrived. Aggressive expansions by cathode active material (CAM) producers and battery cell makers led to increased supply of battery scrap generated during the production process. As a result, retired batteries accounted for a relatively small share of the total lithium battery scrap recycled last year.

Featured by relatively high lithium content and stable nickel-cobalt-lithium ratio, pole piece scrap can avoid the problem of doping. Moreover, pole piece scrap can be crushed into powder more easily than batteries, also making it very popular in the recycling market. However, exorbitant prices of pole piece scrap amid sky-rocketing lithium carbonate prices somehow deterred some recyclers.

Black mass was mostly recycled by hydrometallurgy lithium salt smelters, nickel salt smelters, and cobalt salt smelters. Hydrometallurgy smelters who do not have battery scrap dismantling equipment purchased black mass directly for production.

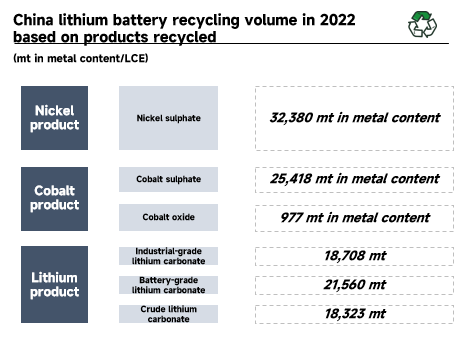

According to SMM data, in December 2022, the volume of nickel sulphate recovered stood at 32,380 mt in metal content, cobalt sulphate 25,418 mt in metal content, cobalt oxide 977 mt in metal content, industrial-grade lithium carbonate 18,708 mt, battery-grade lithium carbonate 21,560 mt, and crude lithium carbonate 18,323 mt.

Looking back on 2022, the lithium battery recycling market experienced several ups and downs. At the beginning of the year, the demand for lithium battery scrap spiked amid soaring lithium carbonate prices, driving the price coefficient of nickel and cobalt to 160% at one point. Nickel prices sky-rocketed in early March, triggering wait-and-see sentiment among recyclers. In late March, China suffered a new wave of Covid outbreak, with Shanghai in two-month lockdown, severely disrupting the supply chain and production of auto makers. As a result, the demand for ternary batteries declined, weighing on the prices of nickel salt, cobalt salt, and lithium salt. Some recyclers slowed down their purchases to minimise the risks on their costs and profits.

After Shanghai lifted its lockdown in early June, the demand for ternary batteries gradually recovered. Recyclers restocked aggressively after running out of their inventories, shoring up battery scrap prices again. With intensified competition in lithium battery recycling market in the second half of the year, the price coefficient of nickel and cobalt contained in battery scrap rose drastically to 240%, while lithium was not priced. To tackle the chaotic market prices, an increasing number of smelters began to price lithium separately when purchasing battery scrap from late August.

The lithium battery recycling boom came to an abrupt end in mid-November due to imminent expiration of NEV subsidies at the end of 2022 and output cuts by ternary battery makers. Industrial-grade lithium carbonate and crude lithium carbonate produced with battery scrap barely found any buyer, while the prices of nickel sulphate and cobalt sulphate went down amid faltering demand. In response, some major smelters proposed to use SMM nickel sulphate, cobalt sulphate, and industrial-grade lithium carbonate prices as the pricing benchmark when purchasing battery scrap so as to avoid the cost risk brought about by volatile metal prices. The recycling market cooled down in December. Recyclers restocked only as needed and were in a rush to clear their inventories.

In 2022, recyclers tried to minimise their risks by responding swiftly to the price fluctuations of battery scrap and their finished products, as well as market trends. The recycling market expanded with the entry of new players.

In 2023, the supply of battery scrap is expected to grow along with the retirement of more power batteries and increased amount of battery scrap generated in production process. It is essential for recyclers to have stable sources of battery scrap amid rapidly expanding recycling market. Some recyclers have set up power battery recycling outlets or cooperated with battery makers to enhance their supply chain stability. Several leading recyclers have emerged amid fierce market competition.

The lithium battery recycling market will be full of opportunities and challenges in 2023, and SMM will keep a close eye on the market dynamics.