SHANGHAI, Jan 6 (SMM) - This is a roundup of China's metals weekly inventory as of January 6.

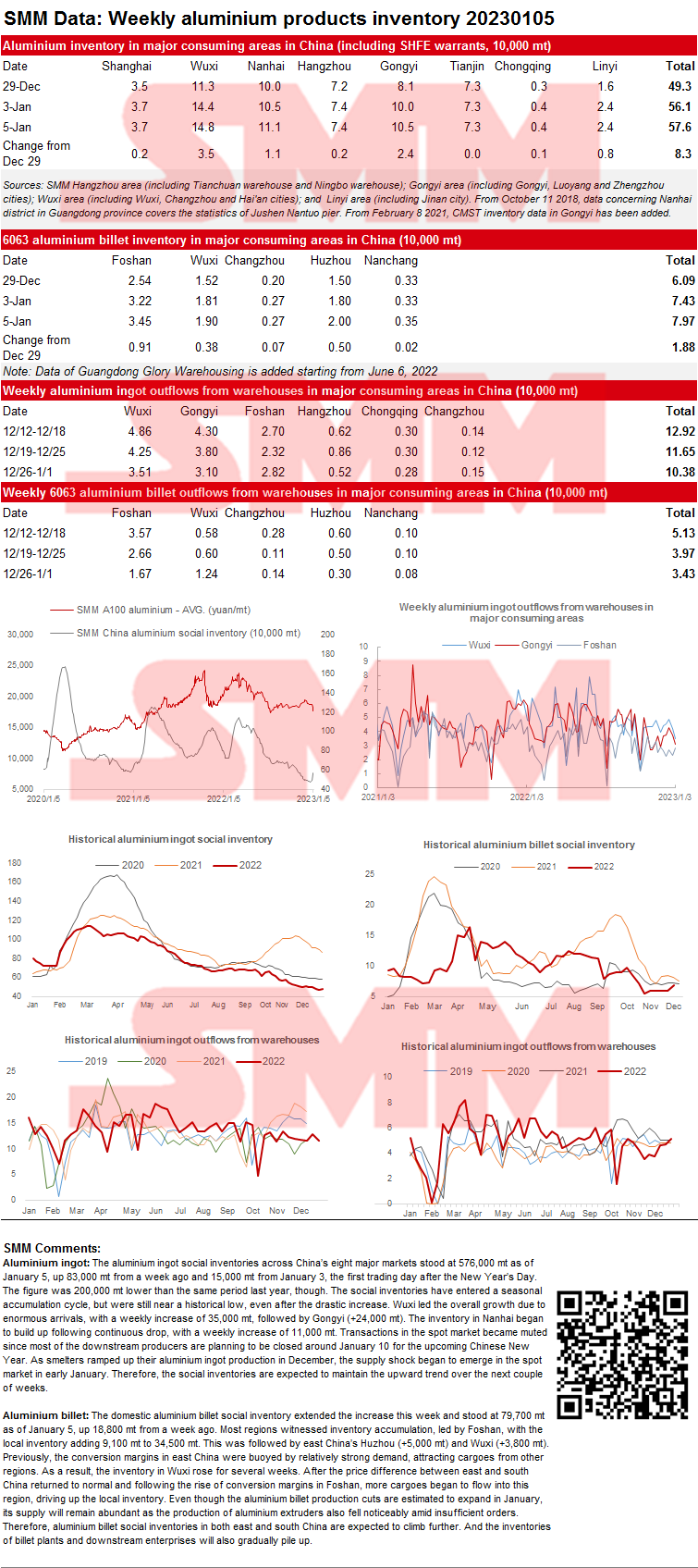

SMM Aluminium Ingot and Billet Social Inventories as of January 5

Aluminium ingot: The aluminium ingot social inventories across China’s eight major markets stood at 576,000 mt as of January 5, up 83,000 mt from a week ago and 15,000 mt from January 3, the first trading day after the New Year’s Day. The figure was 200,000 mt lower than the same period last year, though. The social inventories have entered a seasonal accumulation cycle, but were still near a historical low, even after the drastic increase. Wuxi led the overall growth due to enormous arrivals, with a weekly increase of 35,000 mt, followed by Gongyi (+24,000 mt). The inventory in Nanhai began to build up following continuous drop, with a weekly increase of 11,000 mt. Transactions in the spot market became muted since most of the downstream producers are planning to be closed around January 10 for the upcoming Chinese New Year. As smelters ramped up their aluminium ingot production in December, the supply shock began to emerge in the spot market in early January. Therefore, the social inventories are expected to maintain the upward trend over the next couple of weeks.

Aluminium billet: The domestic aluminium billet social inventory extended the increase this week and stood at 79,700 mt as of January 5, up 18,800 mt from a week ago. Most regions witnessed inventory accumulation, led by Foshan, with the local inventory adding 9,100 mt to 34,500 mt. This was followed by east China’s Huzhou (+5,000 mt) and Wuxi (+3,800 mt). Previously, the conversion margins in east China were buoyed by relatively strong demand, attracting cargoes from other regions. As a result, the inventory in Wuxi rose for several weeks. After the price difference between east and south China returned to normal and following the rise of conversion margins in Foshan, more cargoes began to flow into this region, driving up the local inventory. Even though the aluminium billet production cuts are estimated to expand in January, its supply will remain abundant as the production of aluminium extruders also fell noticeably amid insufficient orders. Therefore, aluminium billet social inventories in both east and south China are expected to climb further. And the inventories of billet plants and downstream enterprises will also gradually pile up.

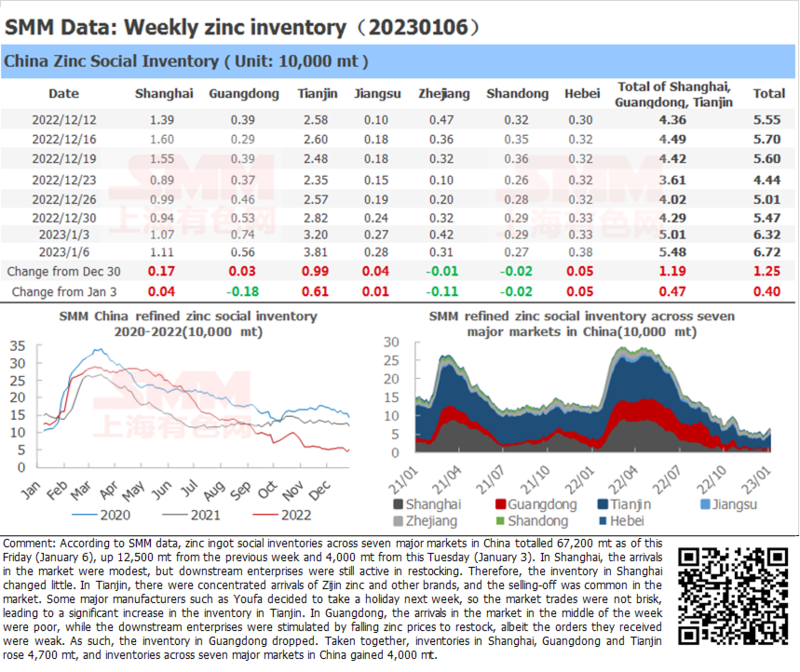

Zinc Ingot Social Inventory Gains 4,000 mt from Tuesday

According to SMM data, zinc ingot social inventories across seven major markets in China totalled 67,200 mt as of this Friday (January 6), up 12,500 mt from the previous week and 4,000 mt from this Tuesday (January 3). In Shanghai, the arrivals in the market were modest, but downstream enterprises were still active in restocking. Therefore, the inventory in Shanghai changed little. In Tianjin, there were concentrated arrivals of Zijin zinc and other brands, and the selling-off was common in the market. Some major manufacturers such as Youfa decided to take a holiday next week, so the market trades were not brisk, leading to a significant increase in the inventory in Tianjin. In Guangdong, the arrivals in the market in the middle of the week were poor, while the downstream enterprises were stimulated by falling zinc prices to restock, albeit the orders they received were weak. As such, the inventory in Guangdong dropped. Taken together, inventories in Shanghai, Guangdong and Tianjin rose 4,700 mt, and inventories across seven major markets in China gained 4,000 mt.

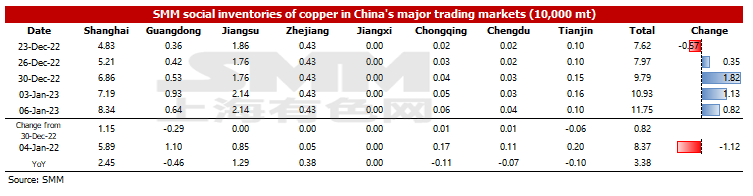

Copper Inventory across Major Chinese Markets Adds 8,200 mt from January 3

As of Friday January 6, SMM copper inventory across major Chinese markets added 8,200 mt from Tuesday January 3 to 117,500 mt, up 19,500 mt from last Friday. Compared with Tuesday's data, the inventory in Shanghai, Chongqing and Chengdu rose, while that in Guangdong and Tianjin decreased slightly. The total inventory was 33,800 mt higher than in the same period last year when the figure was 83,700 mt. The inventory in Shanghai grew 24,500 mt YoY, the inventory in Guangdong dipped 4,600 mt YoY, the inventory in Jiangsu rose 12,900 mt on the year, and the inventory in Zhejiang added 3,800 mt year-on-year.

In detail, the inventory in Shanghai increased 11,500 mt to 68,200 mt compared with Tuesday. The consumption grew compared with last week, but the shipments from domestic smelters were much higher. Smelters in north China ramped up the shipments to east China owing to the poor local consumption, which contributed to the increase in inventory in Shanghai. Inventory in Guangdong dipped 2,900 mt to 6,400 mt. Shipments from nearby smelters were reduced due to their maintenance. Besides, some downstream companies intend to have their Chinese New Year holiday early next week, so they restocked some raw materials amid the falling copper prices this week, which can also be reflected in the increase in the daily shipments flowing out of the warehouses in Guangdong. The decline in inventory in Tianjin was caused by the growing shipments from smelters in north-east China to the east.

Looking forward, the arrival of imported copper will not grow greatly next week, but that of domestic copper will rise WoW. Smelters will increase their shipments of goods to warehouses for delivery owing to the decrease in local consumption. SMM survey showed that most downstream companies will take their Chinese New Year holiday 4-6 days earlier than in previous years, and the operating rates of enterprises that maintain the normal production before the Chinese New Year will drop compared with the previous year. SMM believes that the supply will grow while the consumption may weaken next week, and the inventory will increase further.

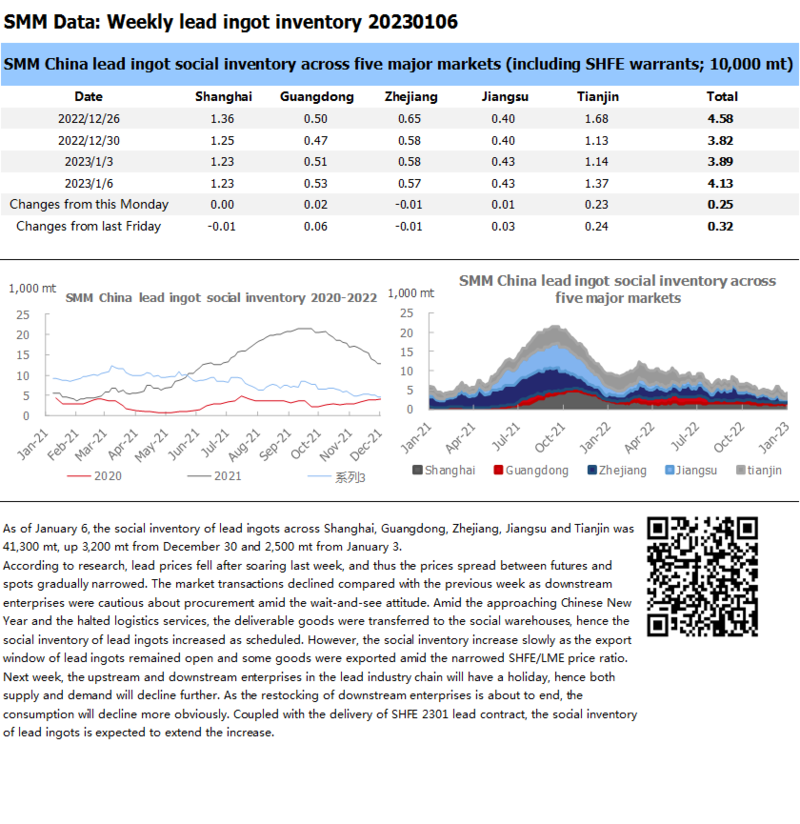

Social Inventory of Lead Ingots Increased as Expected But the Accumulation was Slow Amid the Profitable Exports

As of January 6, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 41,300 mt, up 3,200 mt from December 30 and 2,500 mt from January 3.

According to research, lead prices fell after soaring last week, and thus the prices spread between futures and spots gradually narrowed. The market transactions declined compared with the previous week as downstream enterprises were cautious about procurement amid the wait-and-see attitude. Amid the approaching Chinese New Year and the halted logistics services, the deliverable goods were transferred to the social warehouses, hence the social inventory of lead ingots increased as expected. However, the social inventory increase slowly as the export window of lead ingots remained open and some goods were exported amid the narrowed SHFE/LME price ratio. Next week, the upstream and downstream enterprises in the lead industry chain will have a holiday, hence both supply and demand will decline further. As the restocking of downstream enterprises is about to end, the consumption will decline more obviously. Coupled with the delivery of SHFE 2301 lead contract, the social inventory of lead ingots is expected to extend the increase.

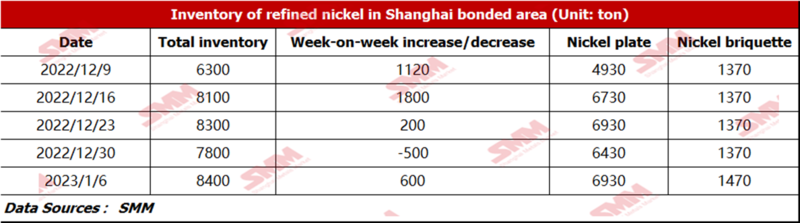

Bonded Zone Inventory of Nickel Grows 600 mt from December 30, 2022

As of January 6, 2023, bonded zone inventory of nickel rose to 8,400 mt, with the inventory of nickel briquettes and nickel plates of 1,470 mt and 6,930 mt respectively. Imports of pure nickel have suffered losses for more than two months, which was narrowed by the decline in LME nickel prices overnight, hence some NORNICKEL nickel cleared customs. The supply tightness of pure nickel was eased, and the SHFE/LME nickel price ratio has improved. Some pure nickel arriving at ports was waiting for customs clearance this week amid the expected import profits.

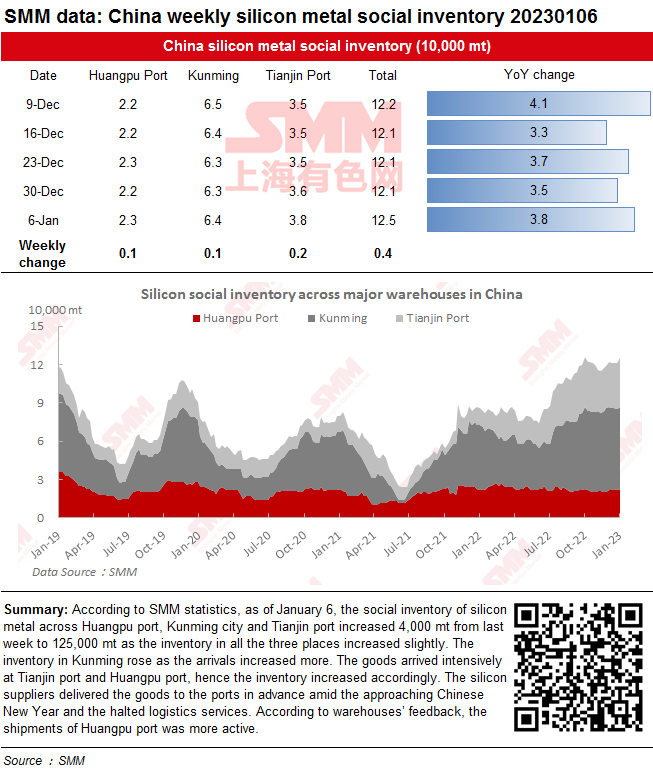

Social Inventory of Silicon Metal Increased as Arrivals Increased

According to SMM statistics, as of January 6, the social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port increased 4,000 mt from last week to 125,000 mt as the inventory in all the three places increased slightly. The inventory in Kunming rose as the arrivals increased more. The goods arrived intensively at Tianjin port and Huangpu port, hence the inventory increased accordingly. The silicon suppliers delivered the goods to the ports in advance amid the approaching Chinese New Year and the halted logistics services. According to warehouses’ feedback, the shipments of Huangpu port was more active.

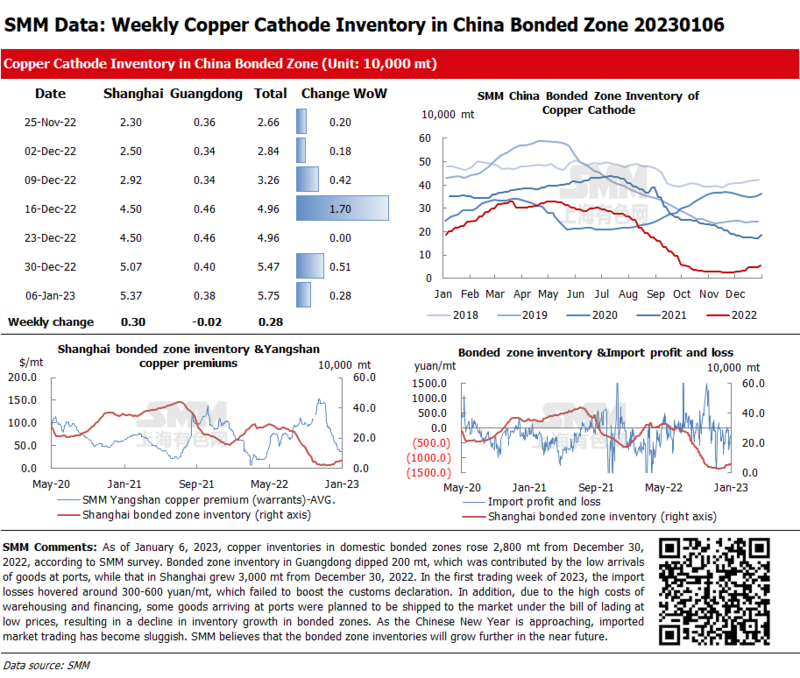

Copper Inventories in Domestic Bonded Zone Add 2,800 mt from December 30, 2022

As of January 6, 2023, copper inventories in domestic bonded zones rose 2,800 mt from December 30, 2022, according to SMM survey. Bonded zone inventory in Guangdong dipped 200 mt, which was contributed by the low arrivals of goods at ports, while that in Shanghai grew 3,000 mt from December 30, 2022. In the first trading week of 2023, the import losses hovered around 300-600 yuan/mt, which failed to boost the customs declaration. In addition, due to the high costs of warehousing and financing, some goods arriving at ports were planned to be shipped to the market under the bill of lading at low prices, resulting in a decline in inventory growth in bonded zones. As the Chinese New Year is approaching, imported market trading has become sluggish. SMM believes that the bonded zone inventories will grow further in the near future.

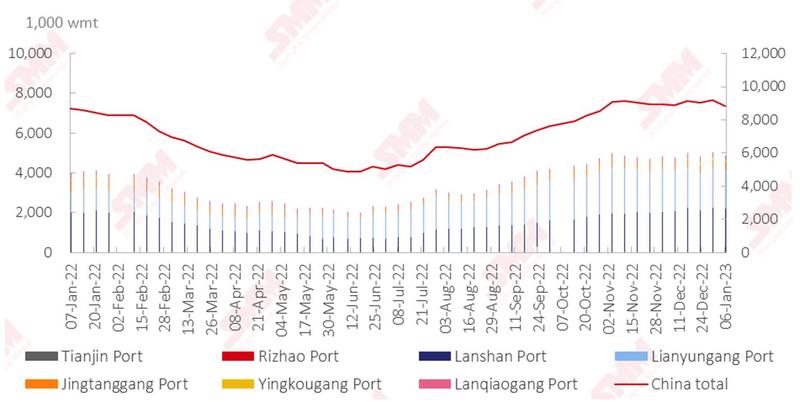

Nickel Ore Inventories at Chinese Ports Down 370,000 wmt from Last Friday

As of January 6, inventory of nickel ore across Chinese ports dipped 370,000 wmt to 8.81 million wmt compared with last Friday. The total Ni content fell 3,000 mt to about 70,000 mt. The inventory across seven major ports totalled 4.88 million wmt. The inventory of nickel ore at ports trended lower in the rainy season in the Philippines. Due to poor weather conditions in the Philippines, the supply of nickel ore is tight. On the demand side, NPI prices remained rangebound, and the in-plant inventories of nickel ore carried by NPI plants were consumed normally. The nickel ore inventory at ports will continue to fall in the near future. The market expects the nickel ore demand to improve after the Chinese New Year holiday, which may accelerate the decrease in port inventory of nickel ore.

![[SMM Analysis] Futures Lack Momentum to Rise Further, Pre-Holiday Demand Stalls, and Stainless Steel Social Inventory Accumulation Intensifies](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)