SHANGHAI, Dec 30 (SMM) - This is a roundup of China's metals weekly inventory as of December 30.

SMM Updates on Aluminium Ingot and Billet Social Inventories as of December 29

Aluminium ingot: The aluminium ingot social inventories across China’s eight major markets totalled 493,000 mt as of December 29, up 18,000 mt from a week ago. Nevertheless, the figure was down 23,000 mt from the end of November and 306,000 mt less than a year ago. Wuxi led the overall growth, with an increase of 24,000 mt from a week ago to above 110,000 mt. The inventory in Gongyi exceeded 80,000 mt after two consecutive weeks of rise, but the increase was relatively slow. The inventory in Foshan remained at a low level due to limited arrivals and output production in Guizhou, and this situation is expected to continue for some time. Increased aluminium ingot output combined with poor downstream consumption in the off-season are likely to push the social inventory into the cycle of seasonal accumulation. However, in view of the production cuts in Yunnan and Guizhou, market attention should be focused on the pace of cargo arrivals and magnitude of inventory accumulation.

Aluminium billet: The domestic aluminium billet social inventory stood at 60,900 mt as of December 29, up 5,100 mt from a week ago. Despite falling demand, the inventory in Foshan dropped 1,500 mt on a weekly basis as many billet plants reduced their shipments to this region. Wuxi (+4,400 mt) and Huzhou (+3,000 mt) were major contributors to the overall inventory accumulation, while inventories in other regions saw only small changes. Affected by falling orders and soaring pandemic, there were massive output cuts among billet plants. The orders and production of aluminium extruders also declined. The overall billet supply remained abundant. The inventory in south China is expected to gradually grow in the future, while that in east China may rise significantly as relatively higher conversion margins and stocking demand will attract billet plants to ship their cargoes to this region.

Copper Inventory in Major Chinese Markets Adds 18,200 mt from Monday

As of Friday December 30, SMM copper inventory across major Chinese markets stood at 97,900 mt, up 18,200 mt from Monday and 21,700 mt from last Friday, which is the highest inventory level in the past three weeks. In detail, the inventory in Shanghai grew 16,500 mt, the inventory in Guangdong rose 1,100 mt, the inventory in both Sichuan and Chongqing added 100 mt, the inventory in Tianjin increased 500 mt, while the inventory in Jiangsu, Zhejiang and Jiangxi remained unchanged.

The continuous rise in copper prices this week suppressed the downstream companies’ buying interest, and the spreading COVID-19 outbreaks cast a huge impact on consumption. The inventory in Guangdong rose this week, but the total inventory was still at a low level in December, because the imported copper did not flow into the market intensively and the downstream consumption was poor. SMM survey showed that some goods were directly transferred from east China to factories in Guangdong during the week. At the year-end, consumption enthusiasm in various places cooled down, hence the inventories in some places did not change much.

Looking forward, SMM expects that the arrivals of imported copper will still be limited next week, and the downstream consumption is unlikely to boom, hence the inventory will edge higher.

Zinc Ingot Social Inventory Gains 4,600 mt from Monday

SMM data shows that the zinc ingot social inventories across seven major markets in China totalled 54,700 mt as of December 30, up 4,600 mt from this Monday (December 26) and up 10,300 mt from a week earlier (December 23). In Shanghai, the market arrivals were relatively stable. Although most downstream enterprises already finished restocking, a few still picked up cargoes in the last trading week before the holiday. Therefore, the inventory in Shanghai dropped. In Tianjin, the transactions in the spot market were quiet, and downstream enterprises rarely picked up cargoes due to poor orders. As a result, the inventory in Tianjin rose. In Guangdong, a few goods arrived in the market at the beginning of the week, and goods holders basically sold off. Since the market was relatively inactive before the holiday, the overall inventory in Guangdong recorded a small increase despite of a few transactions. Taken together, inventories in Shanghai, Guangdong and Tianjin rose 2,700 mt, and inventories across seven major markets in China gained 4,600 mt.

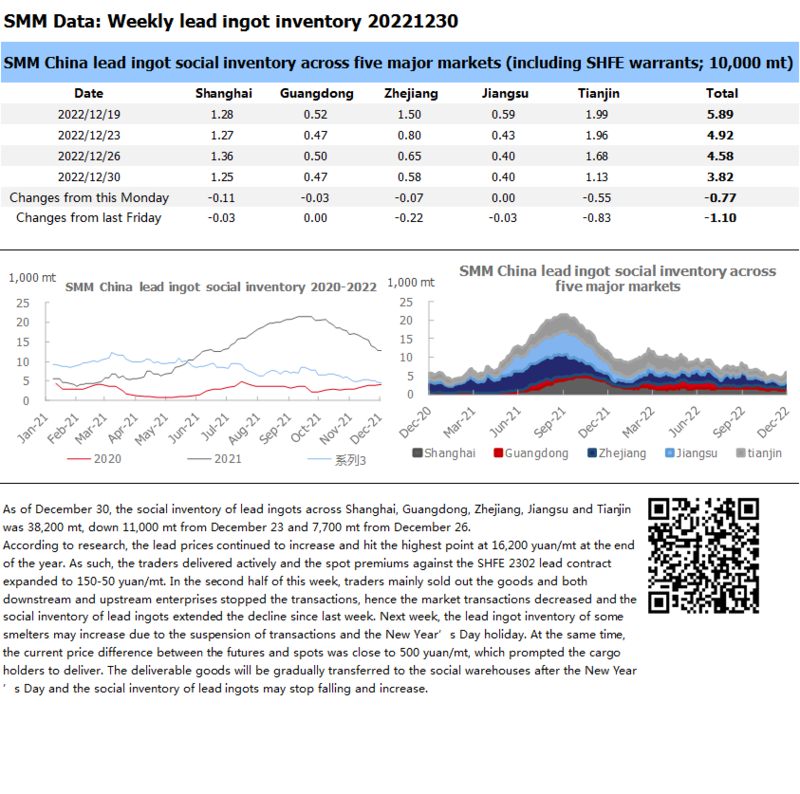

Social Inventory of Lead Ingots Continued to Decline as the Cargo Holders Sold Out Their Goods and Dowsntream Enterprises Restocked at the End of the Year

As of December 30, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 38,200 mt, down 11,000 mt from December 23 and 7,700 mt from December 26.

According to research, the lead prices continued to increase and hit the highest point at 16,200 yuan/mt at the end of the year. As such, the traders delivered actively and the spot premiums against the SHFE 2302 lead contract expanded to 150-50 yuan/mt. In the second half of this week, traders mainly sold out the goods and both downstream and upstream enterprises stopped the transactions, hence the market transactions decreased and the social inventory of lead ingots extended the decline since last week. Next week, the lead ingot inventory of some smelters may increase due to the suspension of transactions and the New Year’s Day holiday. At the same time, the current price difference between the futures and spots was close to 500 yuan/mt, which prompted the cargo holders to deliver. The deliverable goods will be gradually transferred to the social warehouses after the New Year’s Day and the social inventory of lead ingots may stop falling and increase.

Social Inventory of Silicon Metal Remained Stable as the Inventory in North China Increased while that in South China Declined

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port remained stable at 121,000 mt as of December 30. The shipment flow at Huangpu port and Tianjin port was still active this week. The inventory of Huangpu port decreased slightly as some goods have not yet arrived at the warehouses. The inventory of Tianjin port increased slightly as the arrivals were considerable. The shipment flow in Kunming was not active and the inventory remained stable. Amid the approaching Chinese New Year, the transactions in the spot market may continue to weaken due to the insufficient transportation capacity.

Bonded Zone Inventory of Nickel Drops Slightly from December 23

SMM research showed that the bonded zone inventory of nickel fell WoW this week to 7,800 mt, with the inventory of nickel briquettes and nickel plates of 1,370 mt and 6,430 mt respectively. Nickel plate inventory dropped 500 mt. Recently, the SHFE/LME nickel price ratio has remained low, and the spot imports suffered losses. Traders shipped some sources of nickel plates to LME for delivery amid the surging nickel prices in the overseas market. The inventory of nickel briquettes remained unchanged. Domestic salt factories dumped their in-plant inventories of nickel briquettes due to the decline in the cost efficiency, while domestic demand for nickel briquettes dropped.

Copper Inventories in Domestic Bonded Zones Add 5,100 mt from December 23

As of December 30, copper inventories in the domestic bonded zone rose 5,100 mt from December 23, according to SMM survey. The bonded zone inventory in Guangdong fell 600 mt WoW, which was contributed by the normal customs clearance, while that in Shanghai grew 5,700 mt WoW. At the end of the year, domestic spot trading was sluggish. Besides, the import losses expanded to around 600-700 yuan/mt, which failed to encourage the customs declaration. Moreover, some traders converted the bill of lading arriving at ports into warrants, pushing up the inventory. The import market trading was sluggish as the LME market only got three trading days this week and the Hong Kong market suspended trading on December 26 and December 27, so shipments flowing output of the bonded zone warehouses decreased. In the follow-up, the market needs to pay attention to the warehouse operations of goods arriving at ports after some COVID-19-infected port workers return to work.

Nickel Ore Inventory Up 141,000 wmt from December 23

As of December 30, inventory of nickel ore across Chinese ports added 141,000 wmt to 9.18 million wmt compared with last Friday. The total Ni content stood at around 72,000 mt. The port inventory of nickel ore across seven major Chinese ports stood at 5.04 million wmt, 141,000 wmt higher than the previous week. The arrivals at Lanshan Port increased significantly. In the rainy season in the Philippines, the nickel ore shipments reduced, tightening the supply. Downstream demand was slack. NPI plants maintained their production, but the operating rates were low, and their in-plant inventory of nickel ore was consumed slowly. It is expected that the subsequent port inventory of nickel ore will be maintained at the current level in the short term, while in the long run, the inventory may fall.