SHANGHAI, Dec 16 (SMM) - This is a roundup of China's metals weekly inventory as of December 16.

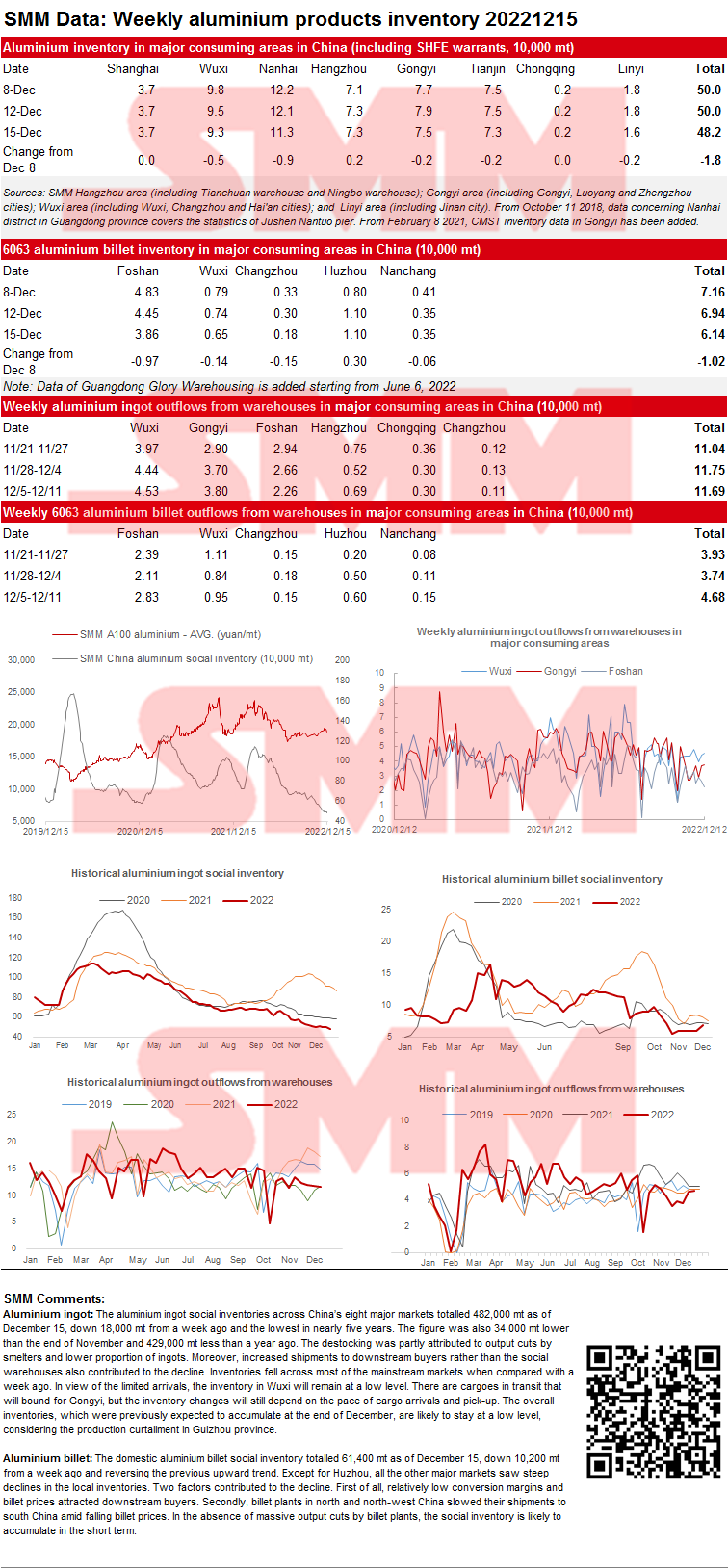

SMM China Aluminium Ingot and Billet Social Inventories as of December 15

Aluminium ingot: The aluminium ingot social inventories across China’s eight major markets totalled 482,000 mt as of December 15, down 18,000 mt from a week ago and the lowest in nearly five years. The figure was also 34,000 mt lower than the end of November and 429,000 mt less than a year ago. The destocking was partly attributed to output cuts by smelters and lower proportion of ingots. Moreover, increased shipments to downstream buyers rather than the social warehouses also contributed to the decline. Inventories fell across most of the mainstream markets when compared with a week ago. In view of the limited arrivals, the inventory in Wuxi will remain at a low level. There are cargoes in transit that will bound for Gongyi, but the inventory changes will still depend on the pace of cargo arrivals and pick-up. The overall inventories, which were previously expected to accumulate at the end of December, are likely to stay at a low level, considering the production curtailment in Guizhou province.

Aluminium billet: The domestic aluminium billet social inventory totalled 61,400 mt as of December 15, down 10,200 mt from a week ago and reversing the previous upward trend. Except for Huzhou, all the other major markets saw steep declines in the local inventories. Two factors contributed to the decline. First of all, relatively low conversion margins and billet prices attracted downstream buyers. Secondly, billet plants in north and north-west China slowed their shipments to south China amid falling billet prices. In the absence of massive output cuts by billet plants, the social inventory is likely to accumulate in the short term.

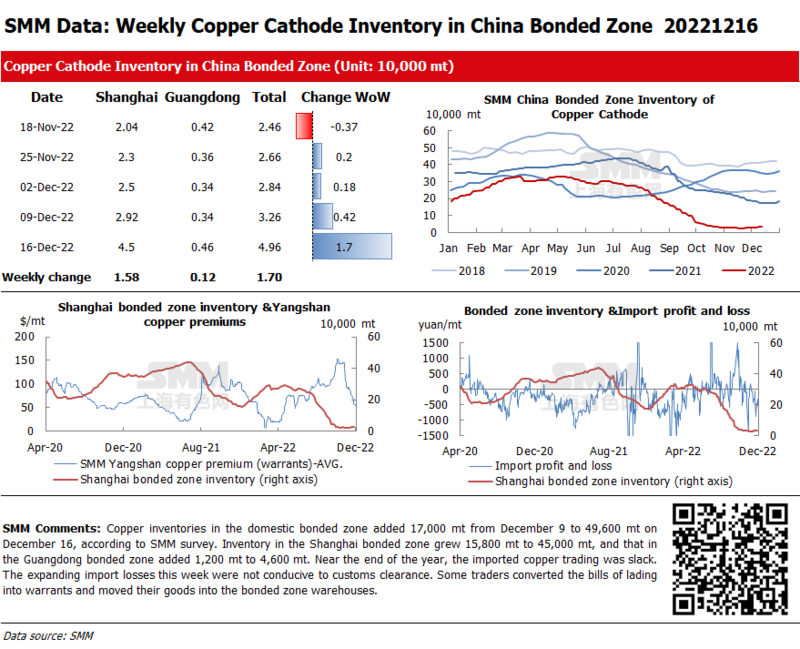

Copper Inventories in Domestic Bonded Zones Up 17,000 mt from December 9

Copper inventories in the domestic bonded zone added 17,000 mt from December 9 to 49,600 mt on December 16, according to SMM survey. Inventory in the Shanghai bonded zone grew 15,800 mt to 45,000 mt, and that in the Guangdong bonded zone added 1,200 mt to 4,600 mt. Near the end of the year, the imported copper trading was slack. The expanding import losses this week were not conducive to customs clearance. Some traders converted the bills of lading into warrants and moved their goods into the bonded zone warehouses.

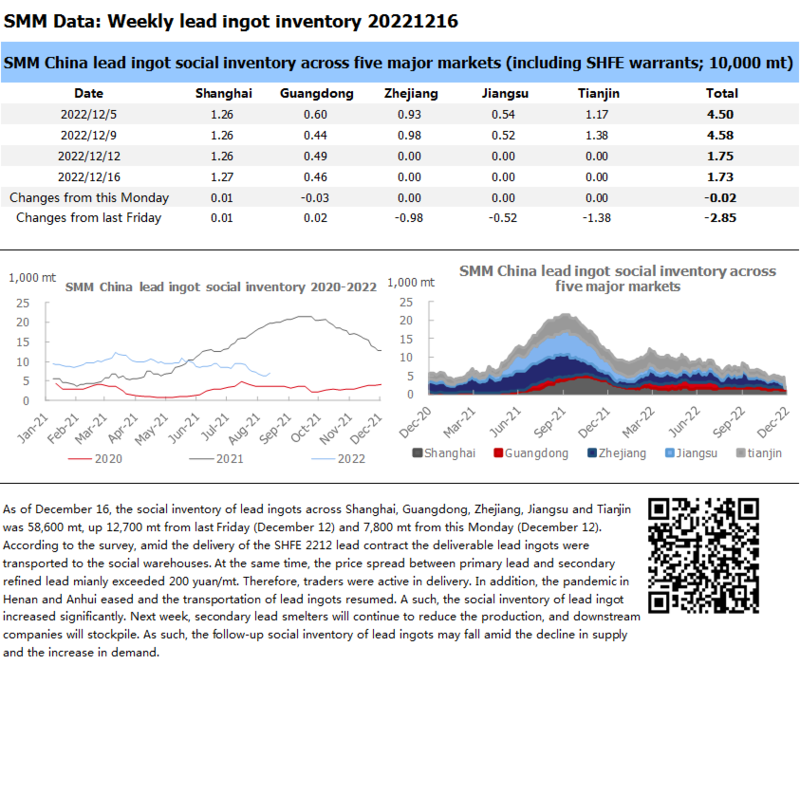

Social Inventory of Lead Ingots may Fall amid the Decline in Supply and the Increase in Demand

As of December 16, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 58,600 mt, up 12,700 mt from last Friday (December 12) and 7,800 mt from this Monday (December 12).

According to the survey, amid the delivery of the SHFE 2212 lead contract the deliverable lead ingots were transported to the social warehouses. At the same time, the price spread between primary lead and secondary refined lead mianly exceeded 200 yuan/mt. Therefore, traders were active in delivery. In addition, the pandemic in Henan and Anhui eased and the transportation of lead ingots resumed. A such, the social inventory of lead ingot increased significantly. Next week, secondary lead smelters will continue to reduce the production, and downstream companies will stockpile. As such, the follow-up social inventory of lead ingots may fall amid the decline in supply and the increase in demand.

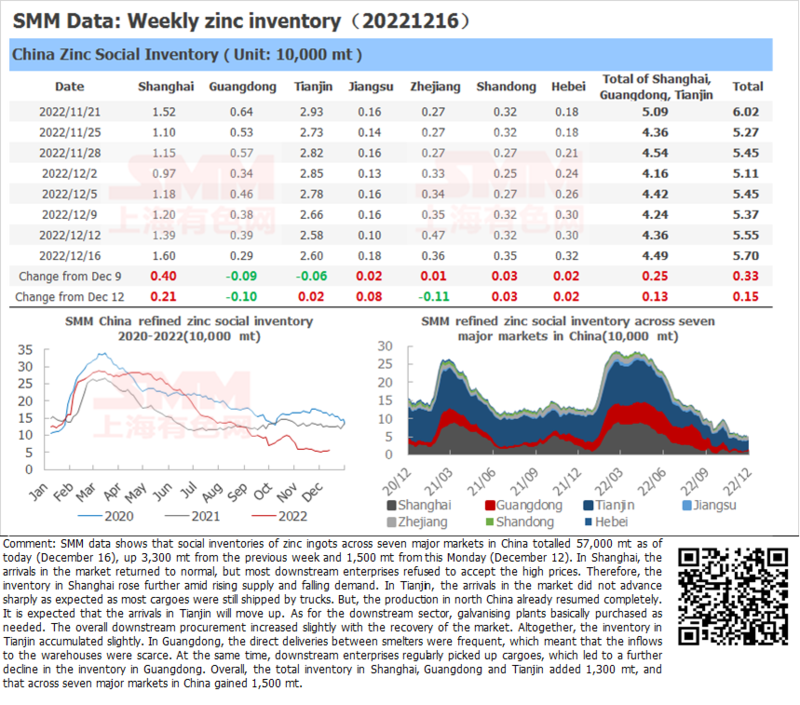

Zinc Ingot Social Inventory Gains 1,500 mt from Monday

SMM data shows that social inventories of zinc ingots across seven major markets in China totalled 57,000 mt as of today (December 16), up 3,300 mt from the previous week and 1,500 mt from this Monday (December 12). In Shanghai, the arrivals in the market returned to normal, but most downstream enterprises refused to accept the high prices. Therefore, the inventory in Shanghai rose further amid rising supply and falling demand. In Tianjin, the arrivals in the market did not advance sharply as expected as most cargoes were still shipped by trucks. But, the production in north China already resumed completely. It is expected that the arrivals in Tianjin will move up. As for the downstream sector, galvanising plants basically purchased as needed. The overall downstream procurement increased slightly with the recovery of the market. Altogether, the inventory in Tianjin accumulated slightly. In Guangdong, the direct deliveries between smelters were frequent, which meant that the inflows to the warehouses were scarce. At the same time, downstream enterprises regularly picked up cargoes, which led to a further decline in the inventory in Guangdong. Overall, the total inventory in Shanghai, Guangdong and Tianjin added 1,300 mt, and that across seven major markets in China gained 1,500 mt.

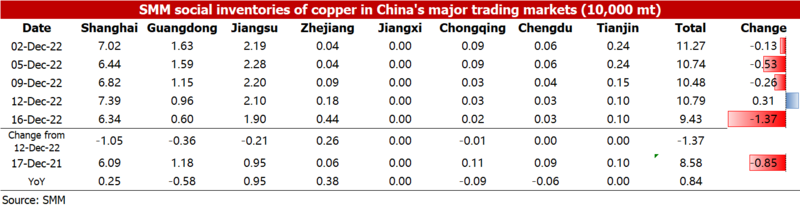

Copper Inventory in Major Chinese Markets Dips 13,700 mt from Monday

As of Friday December 16, SMM copper inventory across major Chinese markets stood at 94,300 mt, down 13,700 mt from Monday and 4,800 mt from last Friday. Compared with Monday's data, except for Zhejiang, the inventory in other mainstream regions such as Shanghai, Guangdong and Jiangsu dropped, while that in Jiangxi, Chengdu and Tianjin remained unchanged. The total inventory was 8,500 mt higher than in the same period last year when the figure was 85,800 mt.

In detail, the inventory in Shanghai dipped 10,500 mt to 63,400 mt compared with Monday. The SHFE/LME copper price ratio continued to drop this week. COVID-19 outbreaks still hindered the inflow of imported copper to some extent, and the Shanghai market witnessed almost no imported copper arriving in the region. In addition, some traders shipped copper cathode from Shanghai to Guangdong attracted by the spread between the two places. Inventory in Guangdong fell 3,600 mt to 6,000 mt. In addition to the same decrease in imported copper as the Shanghai market, the shipments from surrounding smelters which were under maintenance dropped. The daily inventory in Guangdong has dropped for ten consecutive days, and the total inventory kept falling during the week. The inventory in Tianjin declined as the smelters in the north preferred to ship their goods to east China.

Looking forward, according to SMM research, the arrivals of imported copper will change little WoW next week. In late December, downstream companies will increase their restocking. SMM believes that the inventory next week will fall slightly if the subsequent arrivals cannot grow.

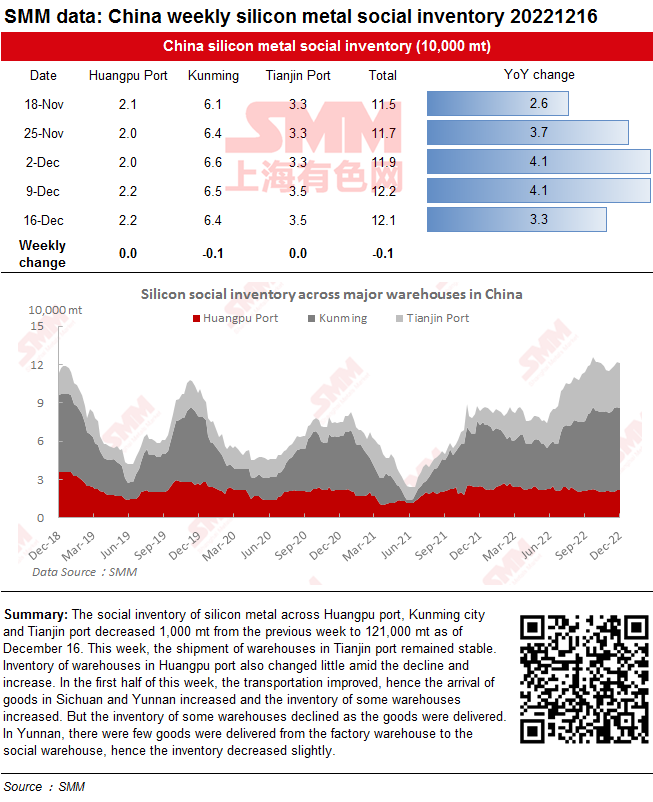

Social Inventory of Silicon Metal Declines This Week

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port decreased 1,000 mt from the previous week to 121,000 mt as of December 16.

This week, the shipment of warehouses in Tianjin port remained stable. Inventory of warehouses in Huangpu port also changed little amid the decline and increase. In the first half of this week, the transportation improved, hence the arrival of goods in Sichuan and Yunnan increased and the inventory of some warehouses increased. But the inventory of some warehouses declined as the goods were delivered. In Yunnan, there were few goods were delivered from the factory warehouse to the social warehouse, hence the inventory decreased slightly.

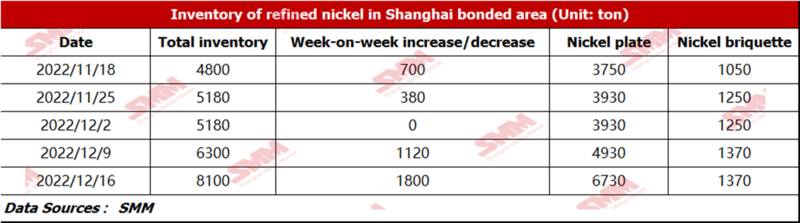

Bonded Zone Inventory of Nickel Adds 1,800 mt from December 9

As of December 16, bonded zone inventory of nickel stood at 8,100 mt, with the inventory of nickel briquette and nickel plate of 1,370 mt and 6,730 mt respectively. Since November 1, the spot imports have suffered great losses amid the low SHFE/LME nickel price ratio. In such a context, the export window opened, thus the nickel plate for exports was shipped to ports, pushing up the bonded zone inventory this week.

Nickel Ore Inventories at Chinese Ports Up 235,000 wmt WoW

As of December 16, port inventories of nickel ore in China added 235,000 wmt to 9.12 million wmt compared with last Friday. The total Ni content stood at around 72,000 mt. The port inventory of nickel ore across seven major Chinese ports stood at 4.99 million wmt, 215,000 wmt higher than the previous week. The arrival volume is reduced in the rainy season. The domestic NPI plants were less willing to produce amid the low profit margins, thus the nickel ore demand decreased. Therefore, the overall port inventory fluctuated upwards. In December, the overall NPI demand was slack. The market transactions will fall greatly after the downstream companies complete their pre-holiday stockpiling. SMM believes that the nickel ore inventory will not fall sharply in the rainy season since the demand weakens.

![[SMM Analysis] Domestic Weakness Meets Overseas Strength, Scrap Tungsten Drags on Sentiment](https://imgqn.smm.cn/production/admin/news/cn/thumb/gsyYF20180628085444.jpeg?imageView2/1/w/176/h/110/q/100)

![Baiyin Nonferrous Group Co., Ltd. Held a Competitive Sale of 33 mt of Crude Selenium on the 27th [SMM Selenium Report]](https://imgqn.smm.cn/usercenter/FHiZE20251217171722.jpeg)