SHANGHAI, Dec 9 (SMM) - This is a roundup of China's metals weekly inventory as of December 9.

SMM Weekly Review of Aluminium Ingot and Billet Social Inventory

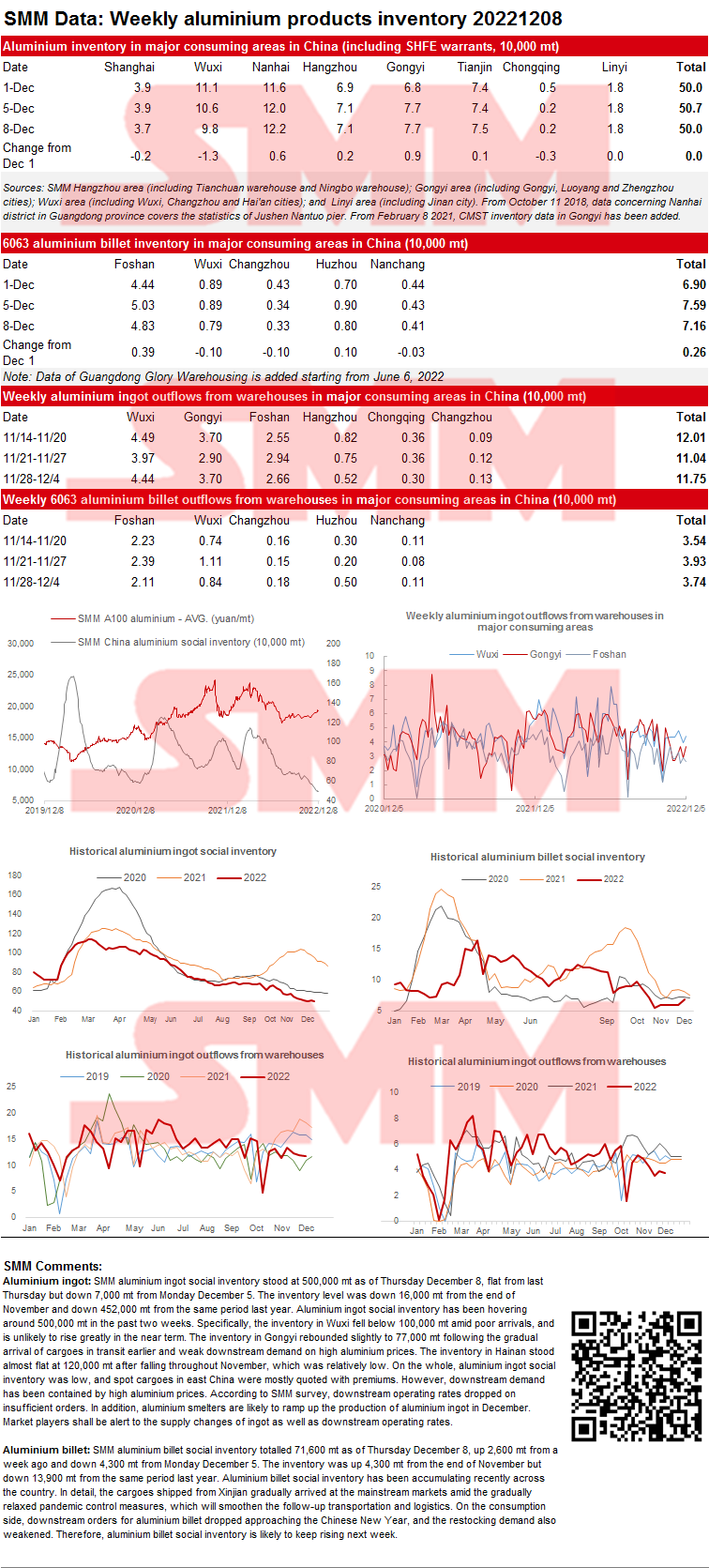

Aluminium ingot: SMM aluminium ingot social inventory stood at 500,000 mt as of Thursday December 8, flat from last Thursday but down 7,000 mt from Monday December 5. The inventory level was down 16,000 mt from the end of November and down 452,000 mt from the same period last year. Aluminium ingot social inventory has been hovering around 500,000 mt in the past two weeks. Specifically, the inventory in Wuxi fell below 100,000 mt amid poor arrivals, and is unlikely to rise greatly in the near term. The inventory in Gongyi rebounded slightly to 77,000 mt following the gradual arrival of cargoes in transit earlier and weak downstream demand on high aluminium prices. The inventory in Hainan stood almost flat at 120,000 mt after falling throughout November, which was relatively low. On the whole, aluminium ingot social inventory was low, and spot cargoes in east China were mostly quoted with premiums. However, downstream demand has been contained by high aluminium prices. According to SMM survey, downstream operating rates dropped on insufficient orders. In addition, aluminium smelters are likely to ramp up the production of aluminium ingot in December. Market players shall be alert to the supply changes of ingot as well as downstream operating rates.

Aluminium billet: SMM aluminium billet social inventory totalled 71,600 mt as of Thursday December 8, up 2,600 mt from a week ago and down 4,300 mt from Monday December 5. The inventory was up 4,300 mt from the end of November but down 13,900 mt from the same period last year. Aluminium billet social inventory has been accumulating recently across the country. In detail, the cargoes shipped from Xinjian gradually arrived at the mainstream markets amid the gradually relaxed pandemic control measures, which will smoothen the follow-up transportation and logistics. On the consumption side, downstream orders for aluminium billet dropped approaching the Chinese New Year, and the restocking demand also weakened. Therefore, aluminium billet social inventory is likely to keep rising next week.

Copper Inventory in Major Chinese Markets Dips 2,600 mt from Monday

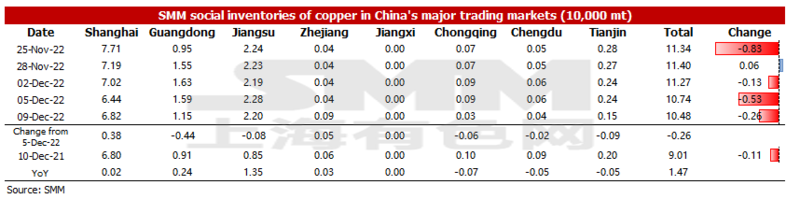

As of Friday December 9, SMM copper inventory across major Chinese markets stood at 104,800 mt, down 2,600 mt from Monday and 7,900 mt from last Friday. Compared with Monday’s data, the inventories in Guangdong, Jiangsu, south-west China and Tianjin declined, while those in Shanghai and Zhejiang grew slightly. The total inventory was 14,700 mt higher than in the same period last year when the figure was 90,100 mt. Among them, the inventory in Shanghai added 200 mt, that in Guangdong grew 2,400 mt, and that in Jiangsu rose 13,500 mt.

In detail, the inventory in Shanghai added 3,800 mt to 68,200 mt from Monday because arrivals of imported copper increased. Inventory in Guangdong dipped 4,400 mt to 11,500 mt. On one hand, shipments from the three surrounding smelters decreased due to maintenance. On the other hand, downstream companies bought goods from warehouses as the volume of goods shipped directly to factories dropped, which was reflected in the continuous increase in the daily average shipments flowing out of the warehouses in Guangdong. The decline in inventory in Tianjin was caused by the growing shipments from smelters in north-east China to the east.

Looking forward, the arrival of imported copper will be flat WoW next week, but that of domestic copper will grow, the SMM survey shows. The overall supply will be higher than this week. Some factories will restock raw materials and ramp up their production with the relaxation of COVID-19 control measures in various regions. But the situation will only last shortly, and the mushrooming copper prices also suppress the recovery of consumption. Therefore, the supply and demand will improve somewhat next week, and the inventory will rise slightly.

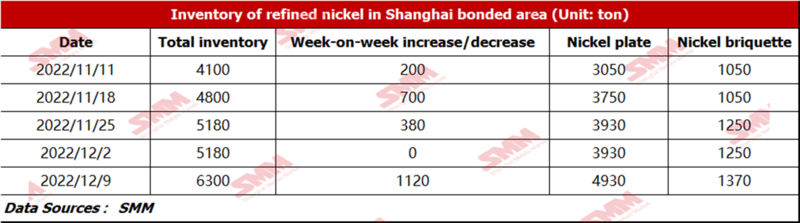

Nickel Inventories in Domestic Bonded Zone Up 1,120 mt from December 2

As of December 9, bonded zone inventory of nickel stood at 6,300 mt, with the inventory of nickel briquette and nickel plate of 1,370 mt and 4,930 mt respectively. Spot import losses surged to 30,000 yuan/mt in the week as the price difference between domestic and overseas futures prices did not show signs of narrowing and the SHFE/LME nickel price ratio fell to 7. Sources of the imported spot were scarce amid the lower-than-expected customs clearance volume and the domestic pure nickel rigid demand, thus some pure nickel was shipped to ports to clear customs in the week.

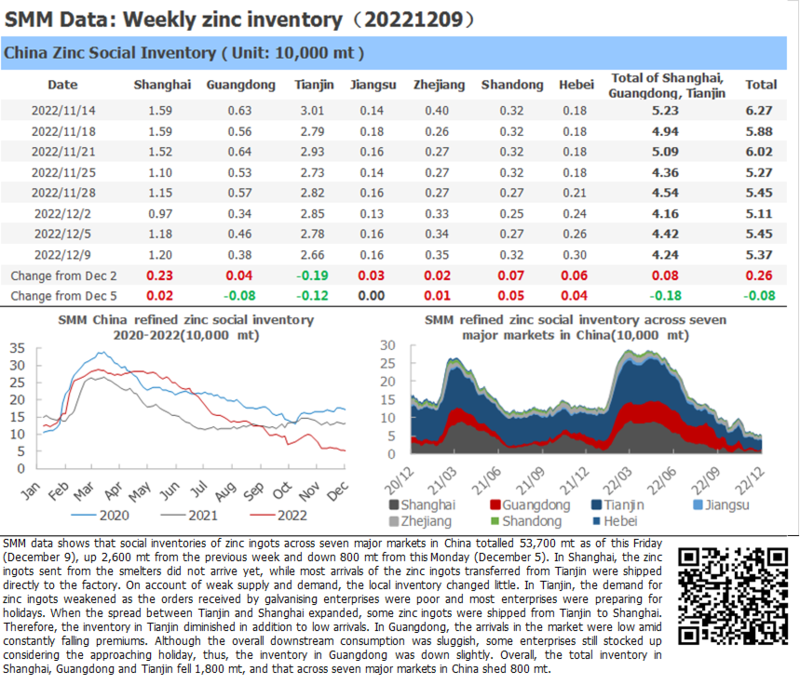

Zinc Ingot Social Inventory Down 800 mt from Monday

SMM data shows that social inventories of zinc ingots across seven major markets in China totalled 53,700 mt as of this Friday (December 9), up 2,600 mt from the previous week and down 800 mt from this Monday (December 5). In Shanghai, the zinc ingots sent from the smelters did not arrive yet, while most arrivals of the zinc ingots transferred from Tianjin were shipped directly to the factory. On account of weak supply and demand, the local inventory changed little. In Tianjin, the demand for zinc ingots weakened as the orders received by galvanising enterprises were poor and most enterprises were preparing for holidays. When the spread between Tianjin and Shanghai expanded, some zinc ingots were shipped from Tianjin to Shanghai. Therefore, the inventory in Tianjin diminished in addition to low arrivals. In Guangdong, the arrivals in the market were low amid constantly falling premiums. Although the overall downstream consumption was sluggish, some enterprises still stocked up considering the approaching holiday, thus, the inventory in Guangdong was down slightly. Overall, the total inventory in Shanghai, Guangdong and Tianjin fell 1,800 mt, and that across seven major markets in China shed 800 mt.

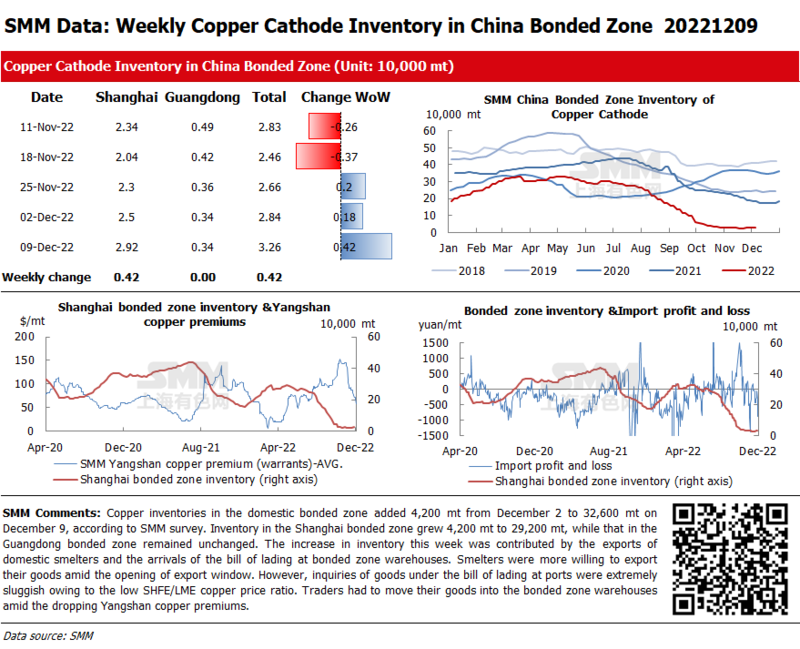

Copper Inventories in Domestic Bonded Zones Add 4,200 mt from Last Friday

Copper inventories in the domestic bonded zone added 4,200 mt from December 2 to 32,600 mt on December 9, according to SMM survey. Inventory in the Shanghai bonded zone grew 4,200 mt to 29,200 mt, while that in the Guangdong bonded zone remained unchanged. The increase in inventory this week was contributed by the exports of domestic smelters and the arrivals of the bill of lading at bonded zone warehouses. Smelters were more willing to export their goods amid the opening of the export window. However, inquiries of goods under the bill of lading at ports were extremely sluggish owing to the low SHFE/LME copper price ratio. Traders had to move their goods into the bonded zone warehouses amid the dropping Yangshan copper premiums.

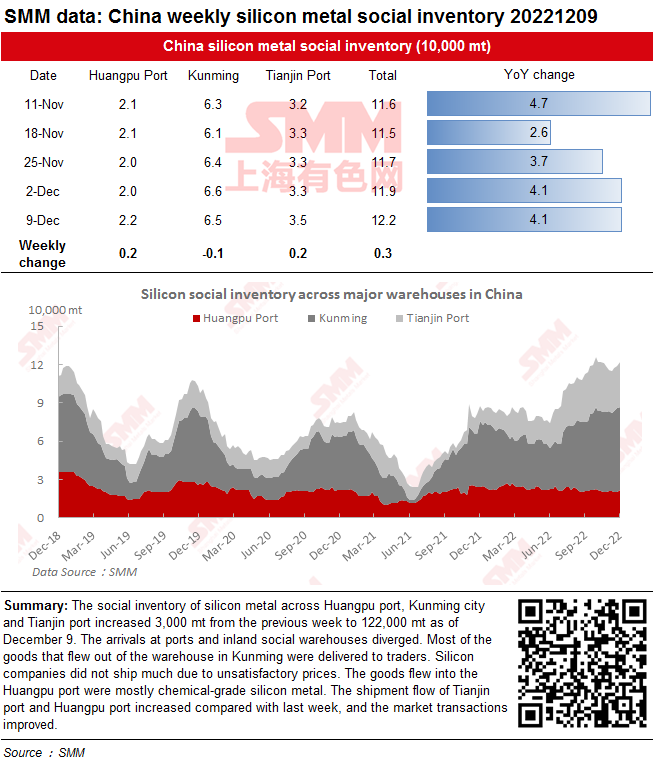

Social Inventory of Silicon Metal Increased as Arrivals at Ports Rose

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port increased 3,000 mt from the previous week to 122,000 mt as of December 9. The arrivals at ports and inland social warehouses diverged. Most of the goods that flew out of the warehouse in Kunming were delivered to traders. Silicon companies did not ship much due to unsatisfactory prices. The goods flew into the Huangpu port were mostly chemical-grade silicon metal. The shipment flow of Tianjin port and Huangpu port increased compared with last week, and the market transactions improved.

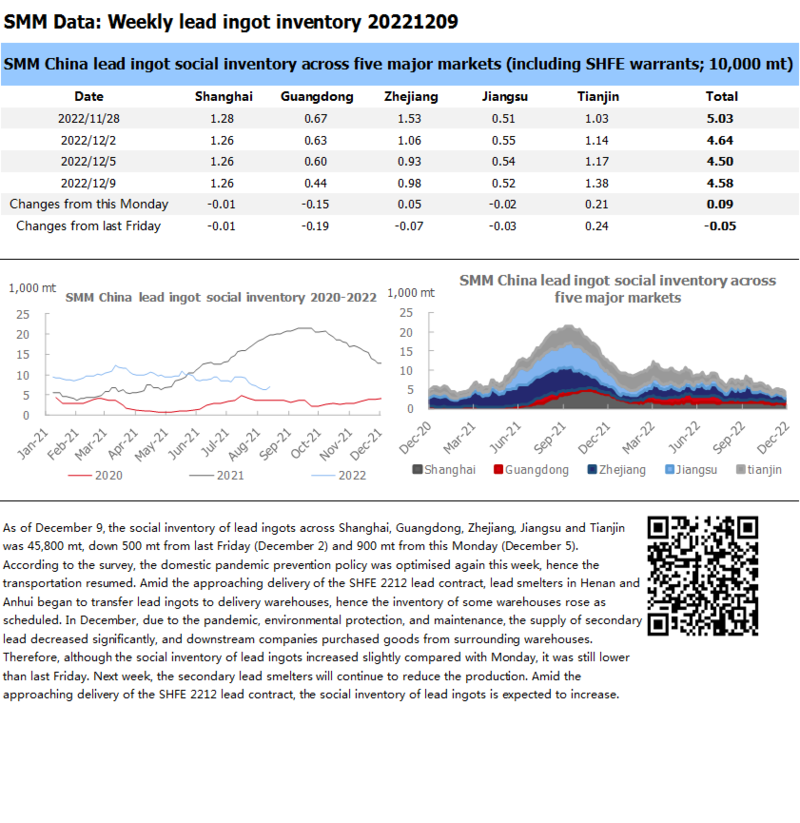

Output Cut of Secondary Lead VS Delivery of SHFE Lead Contract, Social Inventory of Lead Ingot will Further Increase

As of December 9, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 45,800 mt, down 500 mt from last Friday (December 2) and 900 mt from this Monday (December 5).

According to the survey, the domestic pandemic prevention policy was optimised again this week, hence the transportation resumed. Amid the approaching delivery of the SHFE 2212 lead contract, lead smelters in Henan and Anhui began to transfer lead ingots to delivery warehouses, hence the inventory of some warehouses rose as scheduled. In December, due to the pandemic, environmental protection, and maintenance, the supply of secondary lead decreased significantly, and downstream companies purchased goods from surrounding warehouses. Therefore, although the social inventory of lead ingots increased slightly compared with Monday, it was still lower than last Friday. Next week, the secondary lead smelters will continue to reduce the production. Amid the approaching delivery of the SHFE 2212 lead contract, the social inventory of lead ingots is expected to increase.

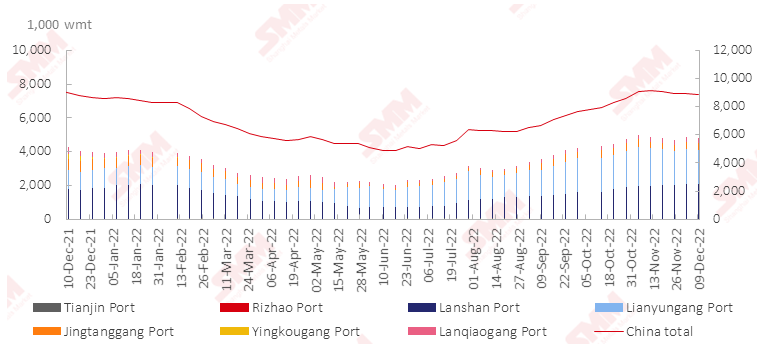

Nickel Ore Inventories at Chinese Ports Down 29,000 wmt WoW

As of December 9, inventory of nickel ore across Chinese ports dipped 29,000 wmt to 8.89 million wmt compared with last Friday. The total Ni content stood at around 70,000 mt. Port inventory of nickel ore across seven major Chinese ports stood at 4.78 million wmt, 59,000 wmt lower than last week. Nickel ore supply remained low as the Philippines is in the rainy season. Besides, the NPI plants demanded less nickel ore amid the slack NPI market. Nickel ore prices trended lower in China, which could not stimulate the imports of nickel ore. On the demand side, some NPI plants’ production will fall in December, and the consumption of nickel ore will slow down. Port inventory of nickel ore will continue to drop in the rainy season.