SHANGHAI, Nov 18 (SMM) - This is a roundup of China's metals weekly inventory as of November 18.

Weekly Review of Aluminium Ingot and Billet Inventory

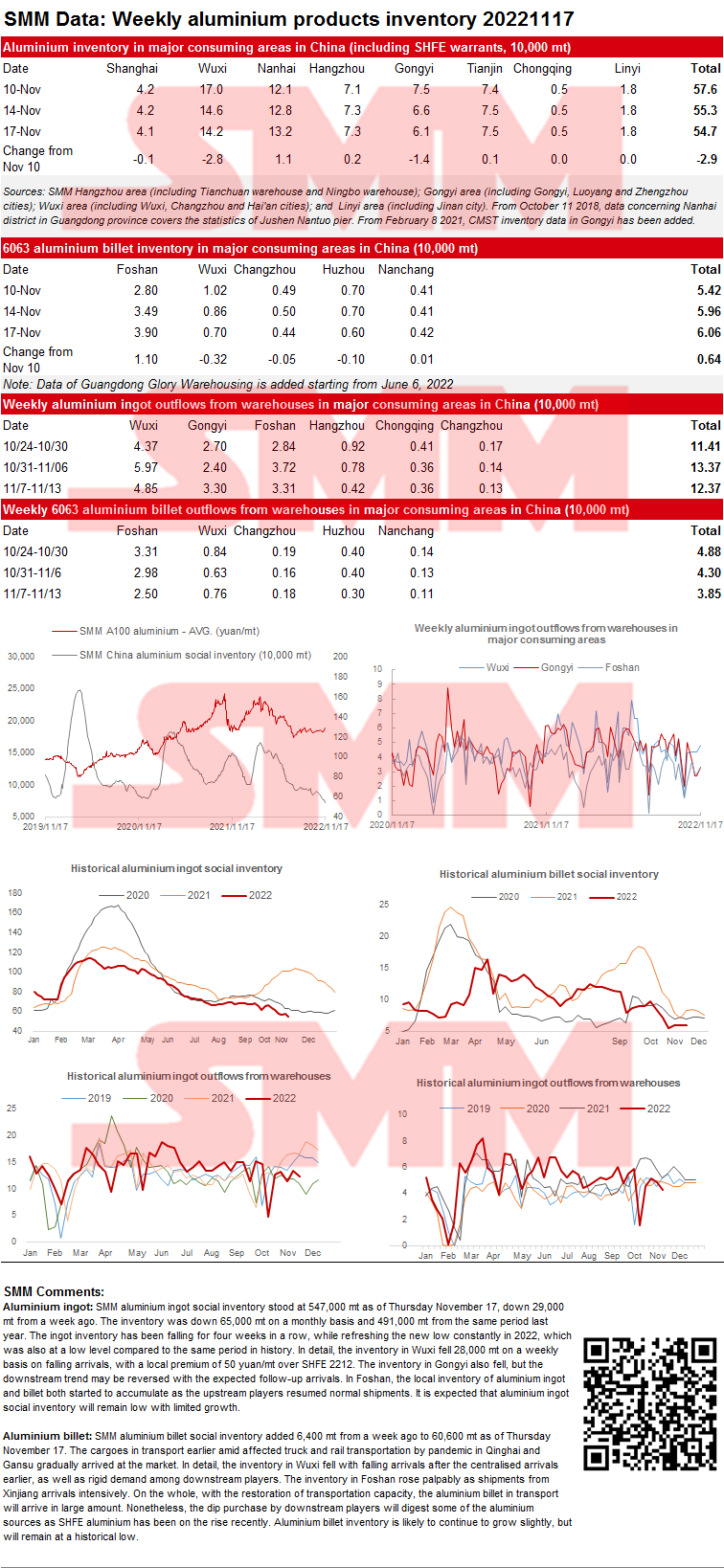

Aluminium ingot: SMM aluminium ingot social inventory stood at 547,000 mt as of Thursday November 17, down 29,000 mt from a week ago. The inventory was down 65,000 mt on a monthly basis and 491,000 mt from the same period last year. The ingot inventory has been falling for four weeks in a row, while refreshing the new low constantly in 2022, which was also at a low level compared to the same period in history. In detail, the inventory in Wuxi fell 28,000 mt on a weekly basis on falling arrivals, with a local premium of 50 yuan/mt over SHFE 2212. The inventory in Gongyi also fell, but the downstream trend may be reversed with the expected follow-up arrivals. In Foshan, the local inventory of aluminium ingot and billet both started to accumulate as the upstream players resumed normal shipments. It is expected that aluminium ingot social inventory will remain low with limited growth.

Aluminium billet: SMM aluminium billet social inventory added 6,400 mt from a week ago to 60,600 mt as of Thursday November 17. The cargoes in transport earlier amid affected truck and rail transportation by pandemic in Qinghai and Gansu gradually arrived at the market. In detail, the inventory in Wuxi fell with falling arrivals after the centralised arrivals earlier, as well as rigid demand among downstream players. The inventory in Foshan rose palpably as shipments from Xinjiang arrivals intensively. On the whole, with the restoration of transportation capacity, the aluminium billet in transport will arrive in large amount. Nonetheless, the dip purchase by downstream players will digest some of the aluminium sources as SHFE aluminium has been on the rise recently. Aluminium billet inventory is likely to continue to grow slightly, but will remain at a historical low.

Copper Inventory in Major Chinese Markets Add 10,900 mt from Monday

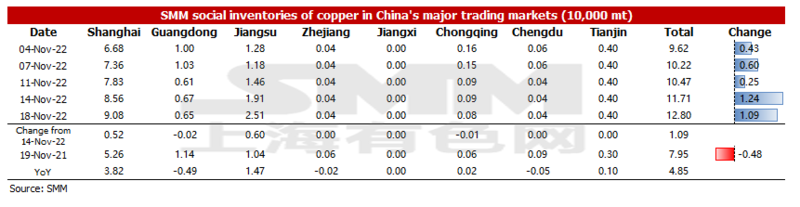

As of Friday November 18, SMM copper inventory across major Chinese markets stood at 128,000 mt, up 10,900 mt from Monday and 23,300 mt from last Friday. Compared with Monday’s data, the inventory in east China grew, while that in the south and south-west declined. The total inventory was 48,500 mt higher than in the same period last year when the figure was 79,500 mt. Among them, the inventory in Shanghai added 38,200 mt, that in Guangdong dipped 4,900 mt, and that in Jiangsu grew 14,700 mt. The sharp increase in inventory this week was caused by the delivery of SHFE 2211 copper.

In detail, the inventory in Shanghai grew 5,200 mt to 90,800 mt from Monday, and that in Jiangsu added 6,000 mt to 25,100 mt, which were contributed by the delivery of SHFE 2211 copper. Inventory in Guangdong dipped 200 mt to 6,500 mt. Arrivals of imported copper were fewer this week, and those of domestic copper was also low due to the maintenance of smelters. The market once witnessed a supply deficit of spots on Thursday and Friday. SMM presumes that in the near future, the inventory in Guangdong will remain low.

Looking forward, the arrival of imported copper next week will not be high, and the domestic smelters’ shipments will also decrease after the centralised delivery of warrants. Consumption is expected to be better than this week, and downstream companies will increase their purchases amid the falling copper prices. Besides, the narrow spread between the copper cathode and copper scrap will also boost copper cathode consumption to a certain extent. SMM believes that the inventory will fall next week.

Social Inventory of Lead Ingots Increased Amid the Delivery of SHFE 2211 Lead Contract and the High Lead Prices

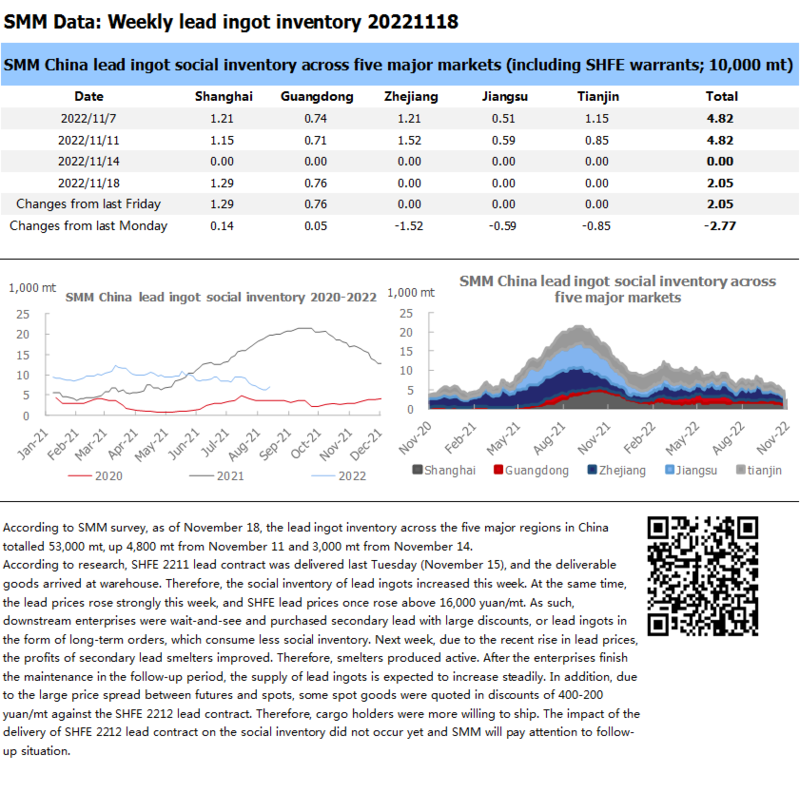

According to SMM survey, as of November 18, the lead ingot inventory across the five major regions in China totalled 53,000 mt, up 4,800 mt from November 11 and 3,000 mt from November 14.

According to research, SHFE 2211 lead contract was delivered last Tuesday (November 15), and the deliverable goods arrived at warehouse. Therefore, the social inventory of lead ingots increased this week. At the same time, the lead prices rose strongly this week, and SHFE lead prices once rose above 16,000 yuan/mt. As such, downstream enterprises were wait-and-see and purchased secondary lead with large discounts, or lead ingots in the form of long-term orders, which consume less social inventory. Next week, due to the recent rise in lead prices, the profits of secondary lead smelters improved. Therefore, smelters produced active. After the enterprises finish the maintenance in the follow-up period, the supply of lead ingots is expected to increase steadily. In addition, due to the large price spread between futures and spots, some spot goods were quoted in discounts of 400-200 yuan/mt against the SHFE 2212 lead contract. Therefore, cargo holders were more willing to ship. The impact of the delivery of SHFE 2212 lead contract on the social inventory did not occur yet and SMM will pay attention to follow-up situation.

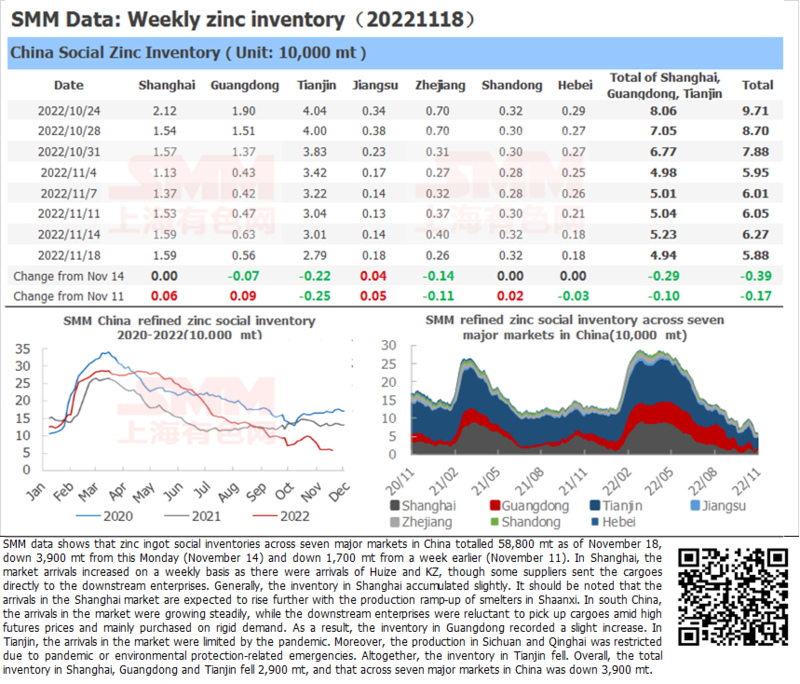

Zinc Ingot Social Inventory Down 3,900 mt from this Monday

SHANGHAI, Nov 18 (SMM) - SMM data shows that zinc ingot social inventories across seven major markets in China totalled 58,800 mt as of November 18, down 3,900 mt from this Monday (November 14) and down 1,700 mt from a week earlier (November 11). In Shanghai, the market arrivals increased on a weekly basis and there were arrivals of Huize and KZ, though some suppliers sent the cargoes directly to the downstream enterprises. Generally, the inventory in Shanghai accumulated slightly. It should be noted that the arrivals in the Shanghai market are expected to rise further with the production ramp-up of smelters in Shaanxi. In south China, the arrivals in the market were growing steadily, while the downstream enterprises were reluctant to pick up cargoes amid high futures prices and mainly purchased on rigid demand. As a result, the inventory in Guangdong recorded a slight increase. In Tianjin, the arrivals in the market were limited by the pandemic. Moreover, the production in Sichuan and Qinghai was restricted due to pandemic or environmental protection-related emergencies. Altogether, the inventory in Tianjin fell. Overall, the total inventory in Shanghai, Guangdong and Tianjin fell 2,900 mt, and that across seven major markets in China was down 3,900 mt.

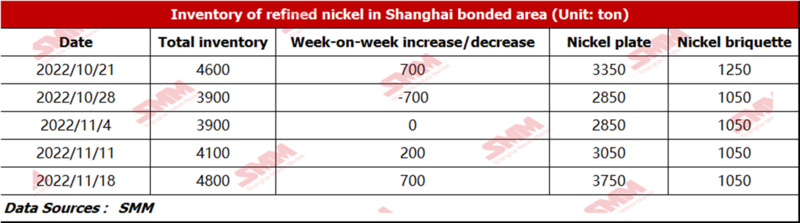

Bonded Zone Inventory of Nickel Increased Slightly from November 11

According to SMM research, the bonded zone inventory rose slightly to 4,800 mt this week. The inventory of nickel briquette was 1,050 mt, and that of nickel plate stood at 3,750 mt. Spot import losses soared to around 35,800 yuan/mt as the SHFE/LME nickel price ratio fell to 7.04 affected by the price difference between the domestic and overseas futures prices, thus only a small amount of nickel plates were moved into the bonded zone warehouses to wait for customs clearance.

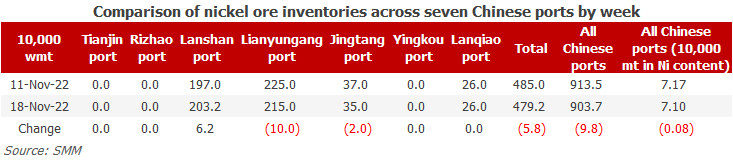

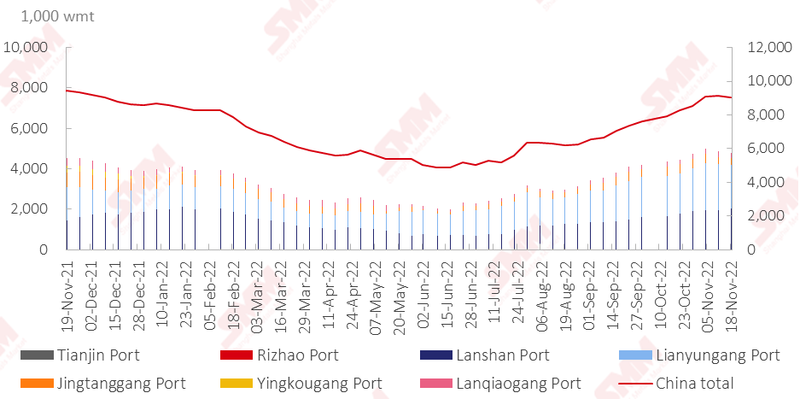

Nickel Ore Inventories at Chinese Ports Down 98,000 wmt WoW

As of November 18, inventory of nickel ore across Chinese ports decreased by 98,000 wmt to 9.04 million wmt compared with last Friday. The total Ni content stood at 71,000 mt. Port inventory of nickel ore across seven major Chinese ports stood at 4,792,000 wmt, 58,000 wmt lower than last week. Poor weather conditions in the Philippines and the transportation problems reduced the nickel ore supply. On the demand side, NPI output is expected to increase in November, and the consumption of raw materials will grow, which will accelerate the destocking of nickel ore. Short-term port inventory of nickel ore will remain rangebound with gradual declines.

Social Inventory of Silicon Metal Decline This Week as the Pandemic Eases

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjing port declined 1,000 mt to 115,000 mt as of November 18. After the pandemic eased in Kunming, the shipment of warehouses resumed to the normal level and the orders placed in the previous stage were shipped. Coupled with the decline in arrivals, the inventory remained low. In Tianjing port, the inflow and outflow of goods were both weak, but the increase in arrivals was more significant, hence the inventory increased slightly. The inventory of Huangpu port remained stable and about 1,000 mt goods will be delivered this weekend.

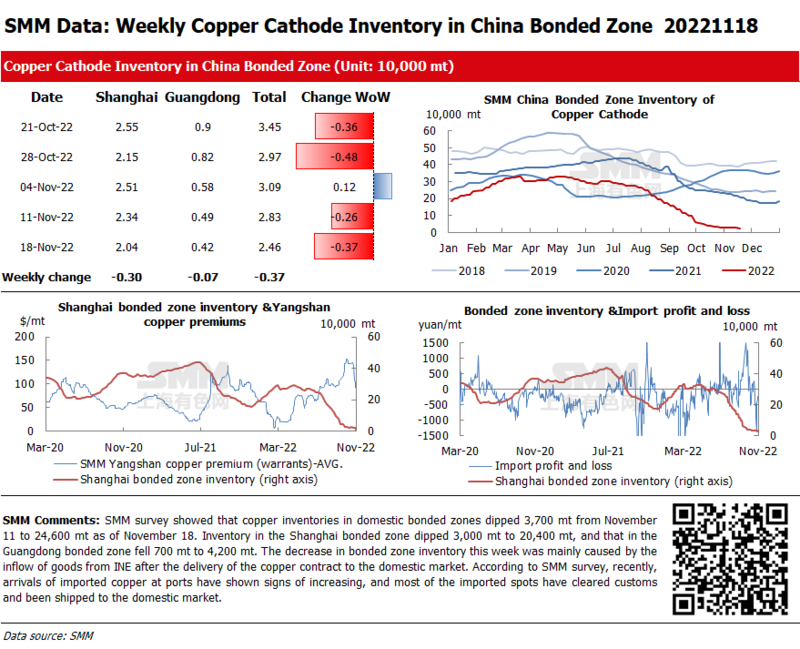

Copper Inventories in Domestic Bonded Zones Dip 3,700 mt from November 11

SMM survey showed that copper inventories in domestic bonded zones dipped 3,700 mt from November 11 to 24,600 mt as of November 18. Inventory in the Shanghai bonded zone dipped 3,000 mt to 20,400 mt, and that in the Guangdong bonded zone fell 700 mt to 4,200 mt. The decrease in bonded zone inventory this week was mainly caused by the inflow of goods from INE after the delivery of the copper contract to the domestic market. According to SMM survey, recently, arrivals of imported copper at ports have shown signs of increasing, and most of the imported spots have cleared customs and been shipped to the domestic market.