SHANGHAI, Sep 30 (SMM) - This is a roundup of China's metals weekly inventory as of September 30.

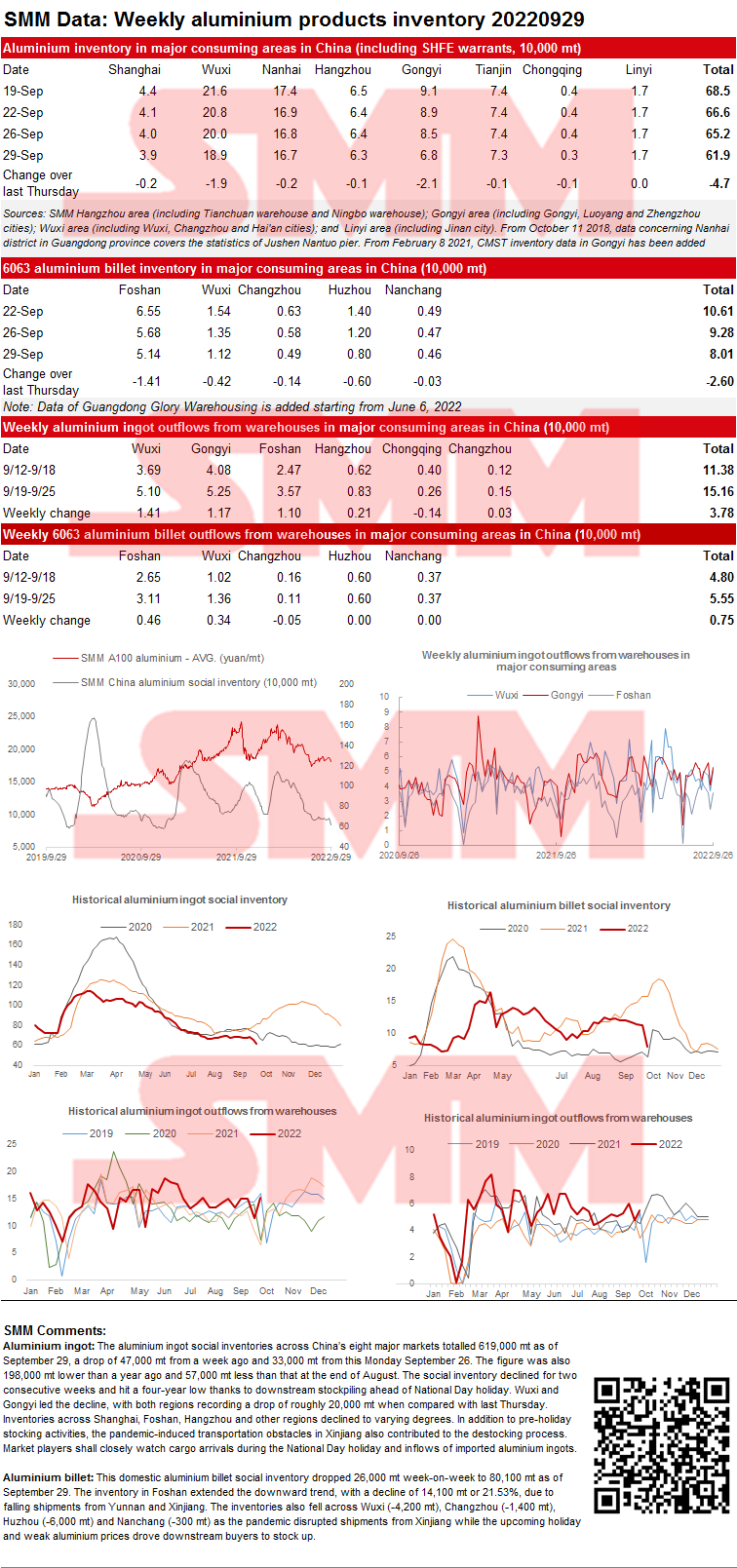

SMM China Aluminium Ingot and Billet Social Inventories as of September 29

Aluminium ingot: The aluminium ingot social inventories across China’s eight major markets totalled 619,000 mt as of September 29, a drop of 47,000 mt from a week ago and 33,000 mt from this Monday September 26. The figure was also 198,000 mt lower than a year ago and 57,000 mt less than that at the end of August. The social inventory declined for two consecutive weeks and hit a four-year low thanks to downstream stockpiling ahead of National Day holiday. Wuxi and Gongyi led the decline, with both regions recording a drop of roughly 20,000 mt when compared with last Thursday. Inventories across Shanghai, Foshan, Hangzhou and other regions declined to varying degrees. In addition to pre-holiday stocking activities, the pandemic-induced transportation obstacles in Xinjiang also contributed to the destocking process. Market players shall closely watch cargo arrivals during the National Day holiday and inflows of imported aluminium ingots.

Aluminium billet: This domestic aluminium billet social inventory dropped 26,000 mt week-on-week to 80,100 mt as of September 29. The inventory in Foshan extended the downward trend, with a decline of 14,100 mt or 21.53%, due to falling shipments from Yunnan and Xinjiang. The inventories also fell across Wuxi (-4,200 mt), Changzhou (-1,400 mt), Huzhou (-6,000 mt) and Nanchang (-300 mt) as the pandemic disrupted shipments from Xinjiang while the upcoming holiday and weak aluminium prices drove downstream buyers to stock up.

Copper Inventory in Major Chinese Markets Dipped 10,100 mt from Monday

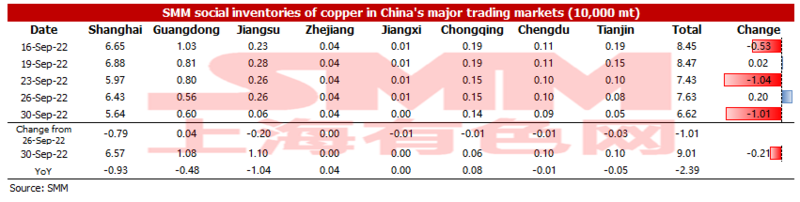

As of Friday September 30, SMM copper inventory across major Chinese markets stood at 66,200 mt, down 10,100 mt from Monday and 8,100 mt from last Friday. Compared with Monday's data, the inventories in most regions of China fell except that in Guangdong. The total inventory dipped 23,900 mt compared with the same period last year when the data was 90,100 mt. Among them, the inventory in Jiangsu dropped 10,400 mt, that in Shanghai fell 9,300 mt, and that in Guangdong dipped 4,800 mt. The decrease in inventory this week was contributed by the downstream pre-holiday restocking. Besides, the customs clearance of imported copper this week was not too much.

In detail, the inventory in Shanghai dropped 7,900 mt to 56,400 mt from Monday, and that in Jiangsu fell 2,000 mt to 600 mt. SMM survey showed that the pre-holiday restocking in east China was favourable, thus the downstream manufacturers will not have a long holiday during the National Day. Inventories in Guangdong added 400 mt to 6,000 mt amid the increase in imported copper and poor downstream consumption, which can also be reflected in the lower average daily shipments flowing out of the warehouses in Guangdong than in the same period last year.

Looking forward, SHFE 2210 copper contract will be delivered a few days after the National Day holiday. The spot prices will be quoted at discounts before the delivery amid the wide spread between the front-month and next-month contracts, thus the smelters may be more willing to deliver. Therefore, SMM believes that the inventory next week will rise sharply.

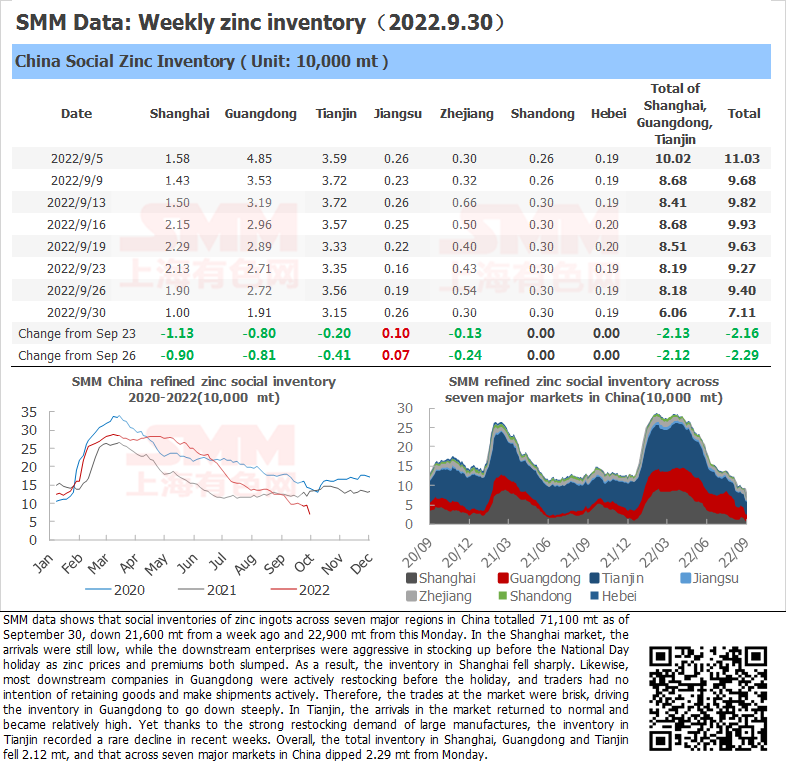

SMM Zinc Ingot Social Inventories Down 22,900 mt from Monday

SMM data shows that social inventories of zinc ingots across seven major regions in China totalled 71,100 mt as of September 30, down 21,600 mt from a week ago and 22,900 mt from this Monday. In the Shanghai market, the arrivals were still low, while the downstream enterprises were aggressive in stocking up before the National Day holiday as zinc prices and premiums both slumped. As a result, the inventory in Shanghai fell sharply. Likewise, most downstream companies in Guangdong were actively restocking before the holiday, and traders had no intention of retaining goods and make shipments actively. Therefore, the trades at the market were brisk, driving the inventory in Guangdong to go down steeply. In Tianjin, the arrivals in the market returned to normal and became relatively high. Yet thanks to the strong restocking demand of large manufactures, the inventory in Tianjin recorded a rare decline in recent weeks. Overall, the total inventory in Shanghai, Guangdong and Tianjin fell 2.12 mt, and that across seven major markets in China dipped 2.29 mt from Monday.

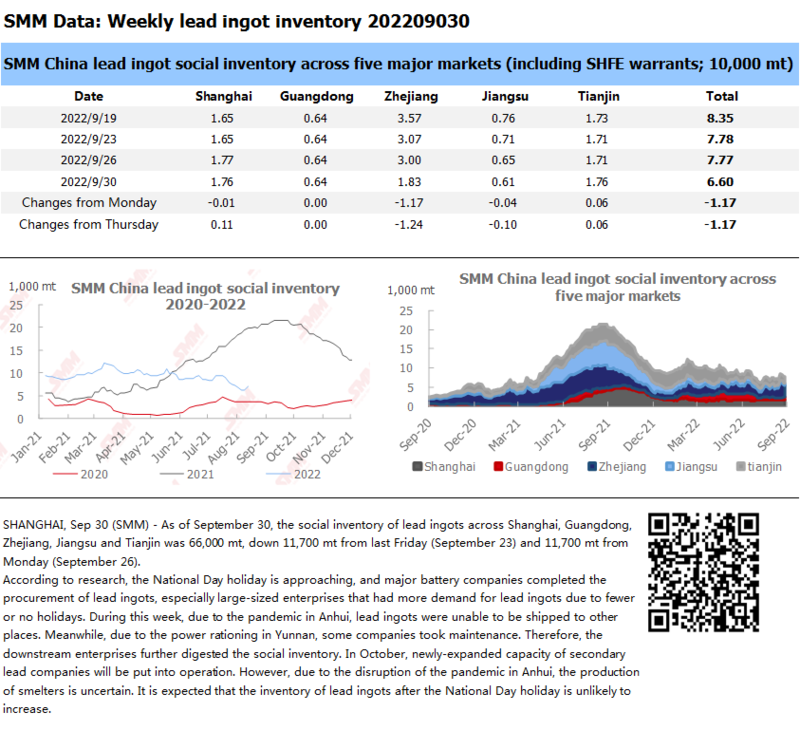

Social Inventory of Lead Ingots Fell More Than 10,000 mt amid Regional Supply Difference and Stockpiling Before National Day Holiday

As of September 30, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 66,000 mt, down 11,700 mt from last Friday (September 23) and 11,700 mt from Monday (September 26).

According to research, the National Day holiday is approaching, and major battery companies completed the procurement of lead ingots, especially large-sized enterprises that had more demand for lead ingots due to fewer or no holidays. During this week, due to the pandemic in Anhui, lead ingots were unable to be shipped to other places. Meanwhile, due to the power rationing in Yunnan, some companies took maintenance. Therefore, the downstream enterprises further digested the social inventory. In October, newly-expanded capacity of secondary lead companies will be put into operation. However, due to the disruption of the pandemic in Anhui, the production of smelters is uncertain. It is expected that the inventory of lead ingots after the National Day holiday is unlikely to increase.

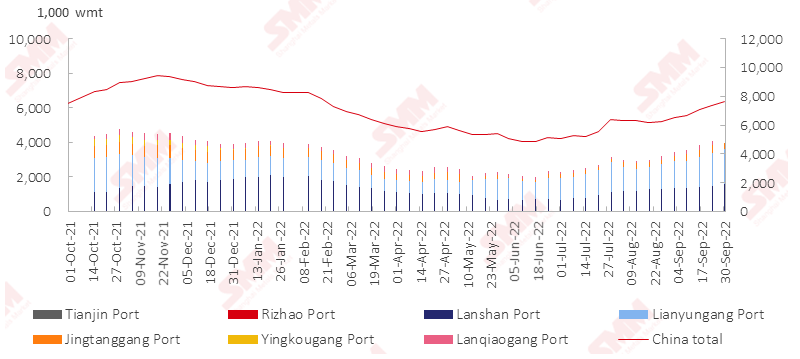

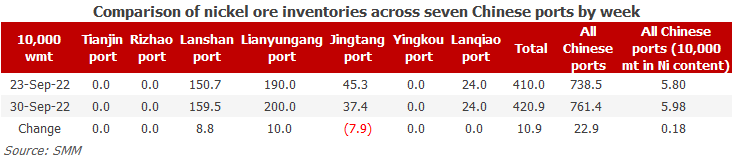

Nickel Ore Inventories at Chinese Ports up 229,000 wmt WoW

As of September 30, port inventories of nickel ore in China added 229,000 wmt to 7.61 million wmt compared with the previous week. The total Ni content stood at 60,000 mt. Port inventory of nickel ore across seven major Chinese ports stood at 4.21 million wmt, 109,000 wmt higher than last week. Nickel ore prices rose slightly amid the restocking demand approaching the rainy season, and the mines became more willing to ship. Besides, the production of domestic NPI plants was still lower than expected even though the plants resumed their operation somewhat, and the consumption of nickel ore stayed stable amid the rising arrival. Therefore, the port inventory began to grow. However, the inventory rose limitedly before the rainy season amid the declined overall shipments in 2022 caused by the poor weather condition and the slack demand. Port inventory of nickel ore may reach 8 million wmt.

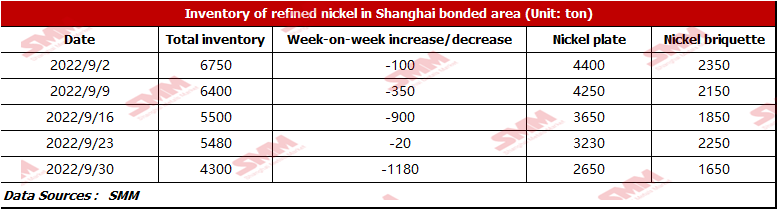

Bonded Zone Inventory of Pure Nickel Decreased this Week with the Improvement of Downstream Demand

SMM research showed that the bonded zone inventory stood at 4,300 mt this week. The inventory of nickel briquette was 1,650 mt, and that of nickel plate was 2,650 mt. In late September, nickel prices surged before dropping, thus the domestic spot trading improved, and the spot imports gained profits this week, pushing up the clearance volume. In addition, before the National Day holiday, downstream companies were busy in restocking, thus the bonded zone inventory of nickel plates and nickel briquettes decreased.

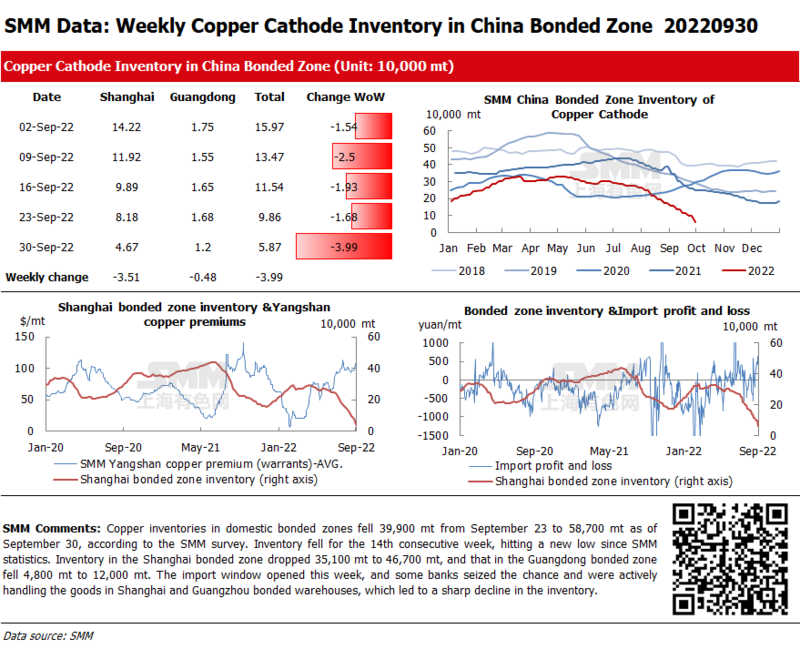

Copper Inventories in Domestic Bonded Zones Dipped 39,900 mt from Last Friday

Copper inventories in domestic bonded zones fell 39,900 mt from September 23 to 58,700 mt as of September 30, according to the SMM survey. Inventory fell for the 14th consecutive week, hitting a new low since SMM statistics. Inventory in the Shanghai bonded zone dropped 35,100 mt to 46,700 mt, and that in the Guangdong bonded zone fell 4,800 mt to 12,000 mt. The import window opened this week, and some banks seized the chance and were actively handling the goods in Shanghai and Guangzhou bonded warehouses, which led to a sharp decline in the inventory.

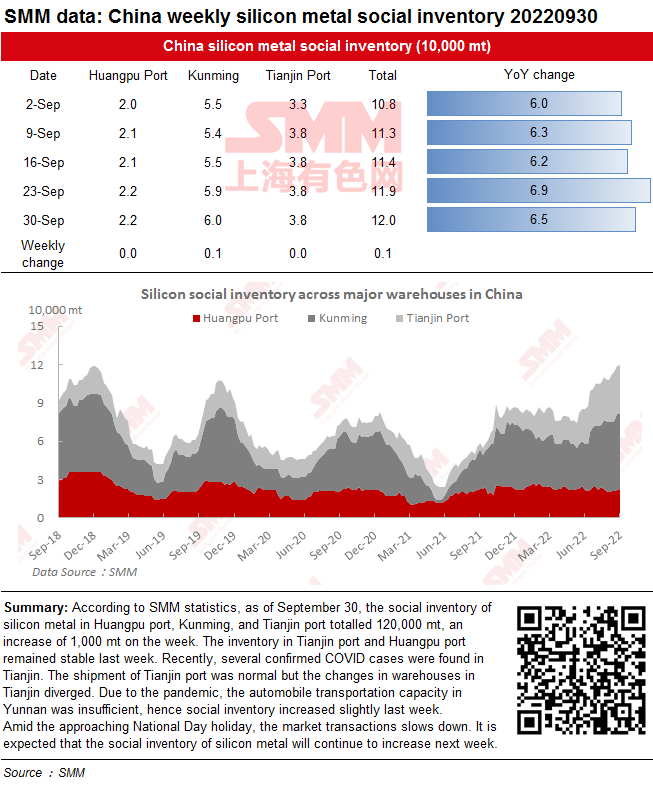

Social Inventory of Silicon Metal Increased This Week and may Further Increase Next Week

According to SMM statistics, as of September 30, the social inventory of silicon metal in Huangpu port, Kunming, and Tianjin port totalled 120,000 mt, an increase of 1,000 mt on the week. The inventory in Tianjin port and Huangpu port remained stable last week. Recently, several confirmed COVID cases were found in Tianjin. The shipment of Tianjin port was normal but the changes in warehouses in Tianjin diverged. Due to the pandemic, the automobile transportation capacity in Yunnan was insufficient, hence social inventory increased slightly last week.

Amid the approaching National Day holiday, the market transactions slows down. It is expected that the social inventory of silicon metal will continue to increase next week.

![Strong Wait-and-See Sentiment; the Tungsten Market Awaited Transaction Stabilization [SMM Tungsten Daily Review]](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)

![Magnesium Ingot Transactions Increased, Rigid Demand Support Became More Evident, and a One-Sided Market Trend Was Unlikely in the Short Term [SMM Spot Magnesium Ingot Flash Report]](https://imgqn.smm.cn/usercenter/hSSxt20251217171722.jpeg)