SHANGHAI, Aug 5 (SMM) - This is a roundup of China's metals weekly inventory as of August 5.

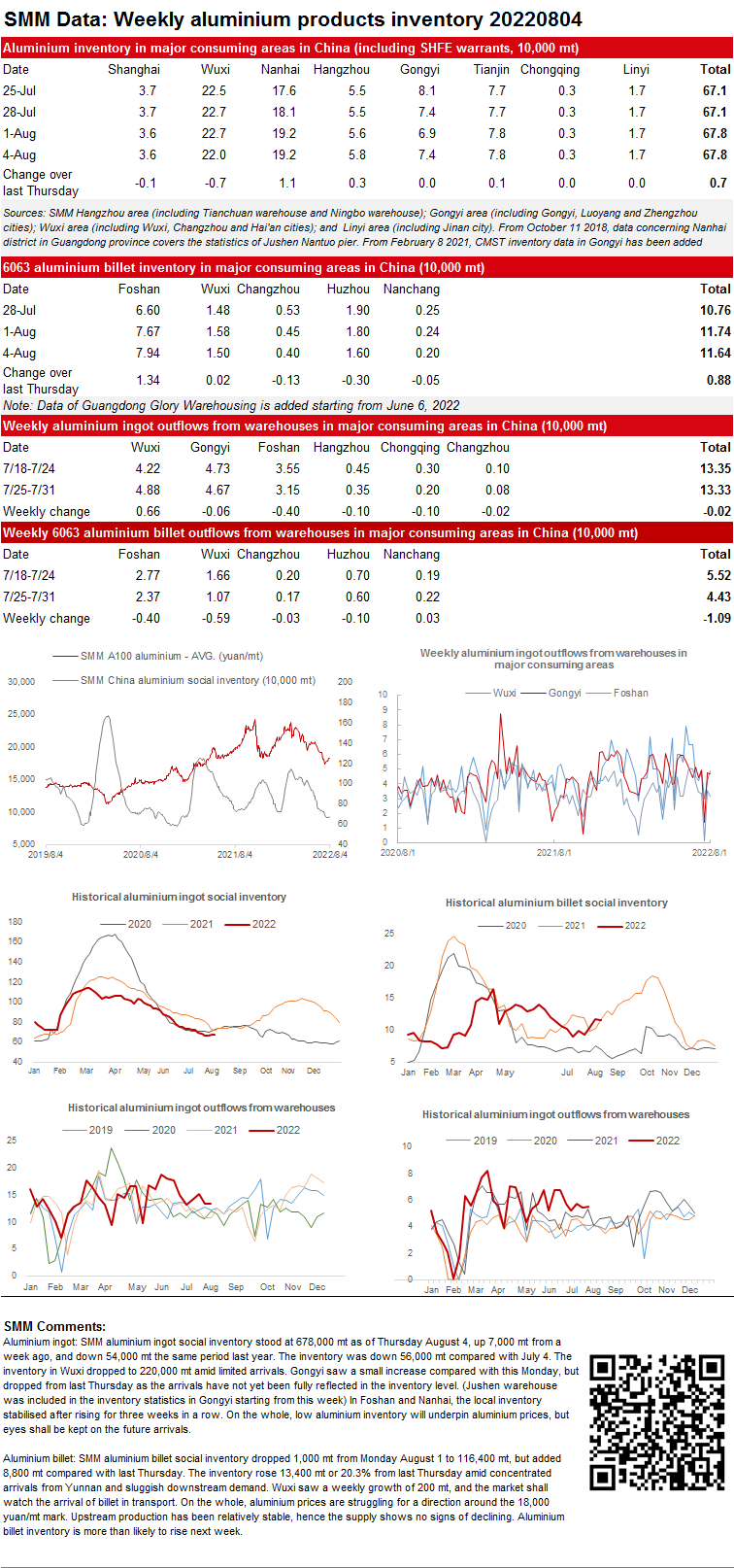

Aluminium Ingot and Billet Inventory both Rose on Weekly Basis

SMM aluminium ingot social inventory stood at 678,000 mt as of Thursday August 4, up 7,000 mt from a week ago, and down 54,000 mt the same period last year. The inventory was down 56,000 mt compared with July 4. The inventory in Wuxi dropped to 220,000 mt amid limited arrivals. Gongyi saw a small increase compared with this Monday, but dropped from last Thursday as the arrivals have not yet been fully reflected in the inventory level. (Jushen warehouse was included in the inventory statistics in Gongyi starting from this week) In Foshan and Nanhai, the local inventory stabilised after rising for three weeks in a row. On the whole, low aluminium inventory will underpin aluminium prices, but eyes shall be kept on the future arrivals.

Aluminium billet: SMM aluminium billet social inventory dropped 1,000 mt from Monday August 1 to 116,400 mt, but added 8,800 mt compared with last Thursday. The inventory in Foshan rose 13,400 mt or 20.3% from last Thursday amid concentrated arrivals from Yunnan and sluggish downstream demand. Wuxi saw a weekly growth of 200 mt, and the market shall watch the arrival of billet in transport. On the whole, aluminium prices are struggling for a direction around the 18,000 yuan/mt mark. Upstream production has been relatively stable, hence the supply shows no signs of declining. Aluminium billet inventory is more than likely to rise next week.

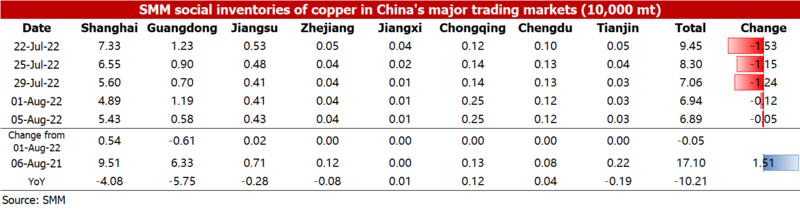

Copper Inventory in Major Chinese Markets Decreased by 500 mt from Monday

As of Friday August 5, SMM copper inventory across major Chinese markets decreased by 500 mt from Monday to 68,900 mt, down 1,700 mt from last Friday. The weekly inventory has been declining for three consecutive weeks, but the decrease rate has lowered significantly.

In detail, the inventory in Shanghai rose by 5,400 mt to 54,300 mt as the imported copper that arrived last week when the import window opened flowed into the Shanghai market this week. In Guangdong, the inventory kept falling, hitting an SMM record low, mainly due to the overhaul of a smelter in Guangxi, the temporary shutdown of the old production lines of a smelter in Guangdong, and the limited inflow of imported goods. Affected by the high spot premiums, some copper rod producers in Guangdong will suspend their production for maintenance this weekend, so the consumption may fall. The inventory in other regions of China changed little.

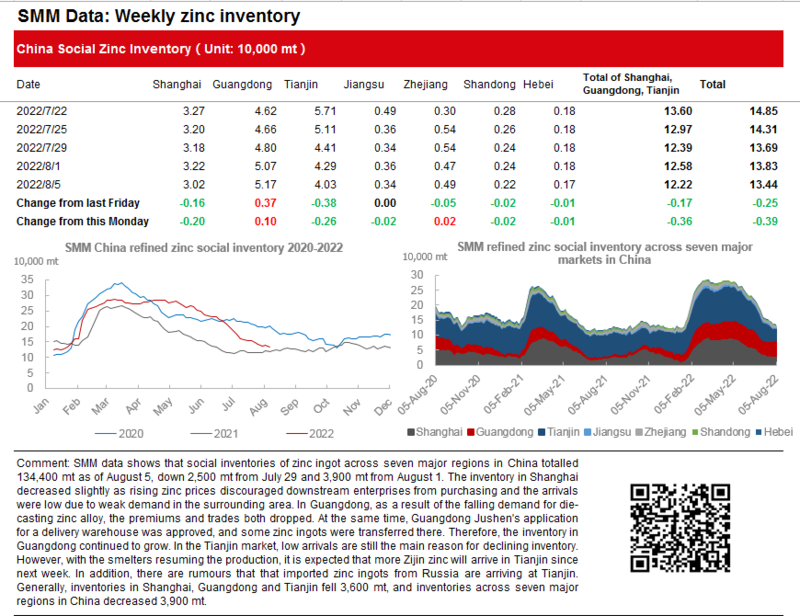

Zinc Ingot Inventory across Seven Major Regions in China Dropped 3,900 mt over the Week

SMM data shows that social inventories of zinc ingot across seven major regions in China totalled 134,400 mt as of August 5, down 2,500 mt from July 29 and 3,900 mt from August 1. The inventory in Shanghai decreased slightly as rising zinc prices discouraged downstream enterprises from purchasing and the arrivals were low due to weak demand in the surrounding area. In Guangdong, as a result of the falling demand for die-casting zinc alloy, the premiums and trades both dropped. At the same time, Guangdong Jushen's application for a delivery warehouse was approved, and some zinc ingots were transferred there. Therefore, the inventory in Guangdong continued to grow. In the Tianjin market, low arrivals are still the main reason for declining inventory. However, with the smelters resuming the production, it is expected that more Zijin zinc will arrive in Tianjin since next week. In addition, there are rumours that that imported zinc ingots from Russia are arriving at Tianjin. Generally, inventories in Shanghai, Guangdong and Tianjin fell 3,600 mt, and inventories across seven major regions in China decreased 3,900 mt.

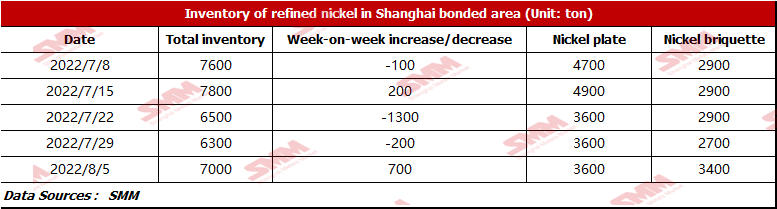

Bonded Zone Inventory of Nickel Increased Slightly as the SHFE/LME Price Ratio Narrowed

Affected by the domestic and overseas nickel futures prices, The SHFE/LME price ratio narrowed this week. According to SMM research, the bonded zone inventory of nickel stood at 7,000 mt this week. The inventory of nickel briquette was 3,400 mt, up 700 mt WoW, and that of nickel plate was 3,600 mt. In the peak season of the new energy industry, the demand from the ternary battery rose slightly, and the nickel sulphate output increased. In addition, some salt plants still purchased nickel briquette on rigid demand based on their long-term orders.

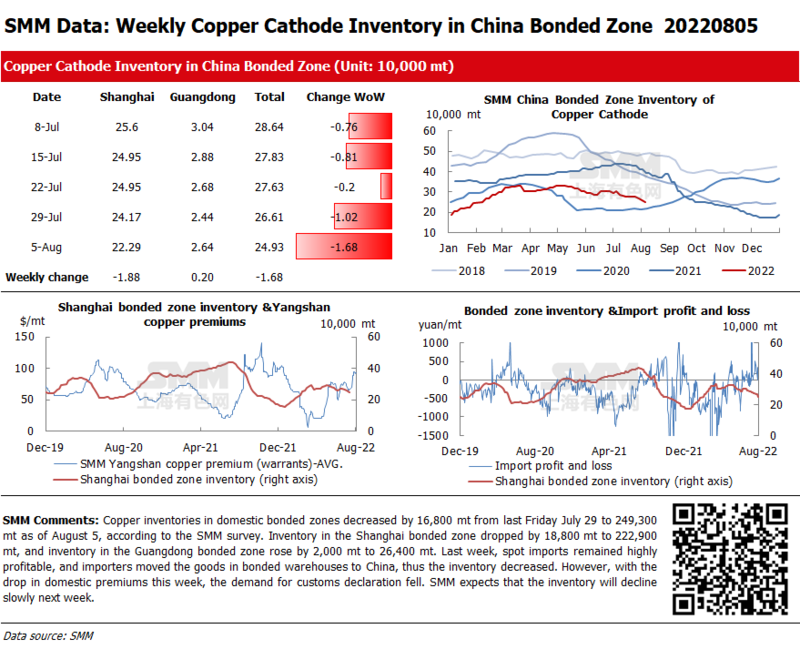

Copper Inventories in Domestic Bonded Zones Decreased by 16,800 mt from Last Friday

Copper inventories in domestic bonded zones decreased by 16,800 mt from last Friday July 29 to 249,300 mt as of August 5, according to the SMM survey. Inventory in the Shanghai bonded zone dropped by 18,800 mt to 222,900 mt, and inventory in the Guangdong bonded zone rose by 2,000 mt to 26,400 mt. Last week, spot imports remained highly profitable, and importers moved the goods in bonded warehouses to China, thus the inventory decreased. However, with the drop in domestic premiums this week, the demand for customs declaration fell. SMM expects that the inventory will decline slowly next week.

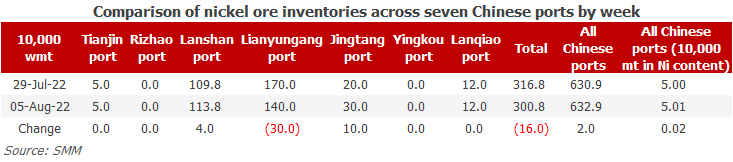

Nickel Ore Inventories at Chinese Ports up 20,000 wmt WoW

As of August 5, port inventories of nickel ore in China increased by 20,000 wmt to 6.32 million wmt compared with last week. The total Ni content stood at around 50,000 mt. Port inventory of nickel ore across seven major Chinese ports stood at 3,008,000 wmt, 160,000 wmt lower than last week. Ore inventory at Lianyungang port declined sharply, while inventory at other ports rose. According to the SMM survey, shipments of ores from the mines were poor owing to the falling ore prices. However, the ocean freight was high, thus the mines cut their production amid the narrow profit margin. Downstream NPI prices remained rangebound at low levels due to the oversupply, putting pressure on the ore prices. The short-term port inventory of nickel ore will hover around the current level, and the supply and demand may be weak.