SHANGHAI, Jun 24 (SMM) - This is a roundup of China's metals weekly inventory as of June 24.

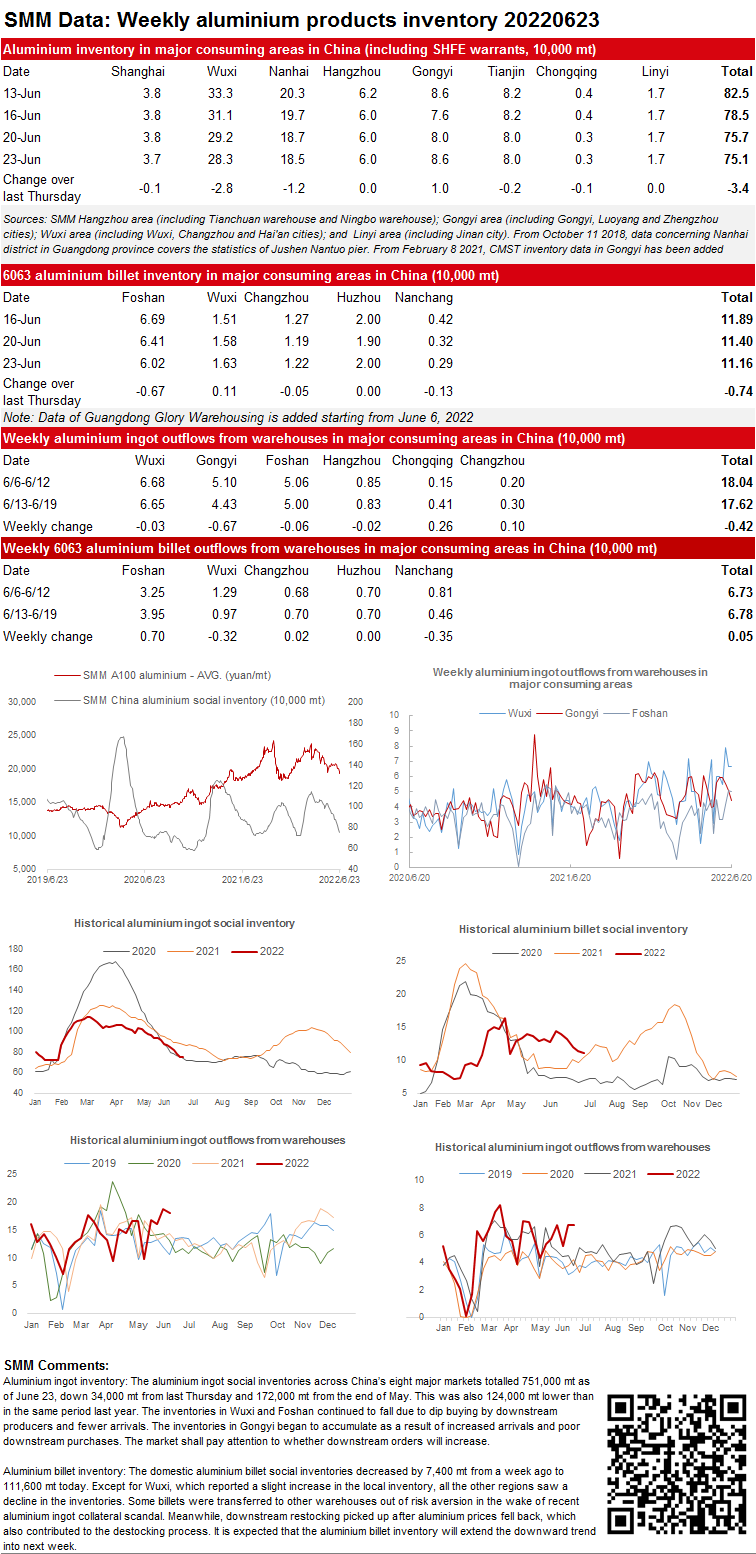

Aluminium Ingot and Billet Inventories both Extended Decline

Aluminium ingot inventory: The aluminium ingot social inventories across China’s eight major markets totalled 751,000 mt as of June 23, down 34,000 mt from last Thursday and 172,000 mt from the end of May. This was also 124,000 mt lower than in the same period last year. The inventories in Wuxi and Foshan continued to fall due to dip buying by downstream producers and fewer arrivals. The inventories in Gongyi began to accumulate as a result of increased arrivals and poor downstream purchases. The market shall pay attention to whether downstream orders will increase.

Aluminium billet inventory: The domestic aluminium billet social inventories decreased by 7,400 mt from a week ago to 111,600 mt today. Except for Wuxi, which reported a slight increase in the local inventory, all the other regions saw a decline in the inventories. Some billets were transferred to other warehouses out of risk aversion in the wake of recent aluminium ingot collateral scandal. Meanwhile, downstream restocking picked up after aluminium prices fell back, which also contributed to the destocking process. It is expected that the aluminium billet inventory will extend the downward trend into next week.

Copper Inventory in Major Chinese Markets Decreased 1,300 mt from Monday

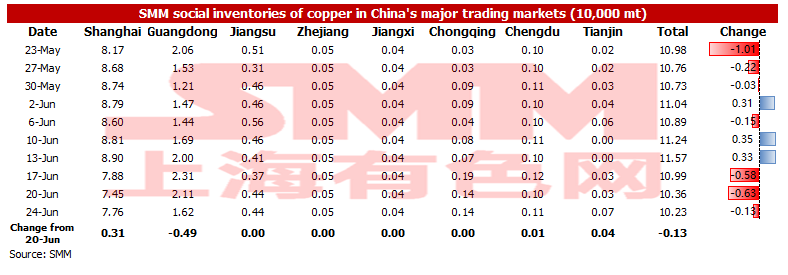

As of Friday June 24, SMM copper inventory across major Chinese markets decreased by 1,300 mt from Monday to 102,300 mt, down by 7,600 mt from last Friday. Compared with Monday's data, the inventories in most regions of China increased, only the inventory in Guangdong decreased. The total inventory dropped by 141,400 mt compared with the same period last year when the inventory was recorded at 243,700 mt. Among them, the inventory in Guangdong dropped by 75,300 mt, the inventory in Shanghai dipped by 42,300 mt, and the inventory in Jiangsu fell by 15,600 mt. Operating rates of copper rod plants in Guangdong were raised with the falling copper prices, thus the inventory in Guangdong decreased the most. In other regions, the sharp drop in copper prices aroused fear in terminal enterprises, hence the inventory in these areas rose.

In detail, the inventory in Shanghai increased by 3,100 mt to 77,600 mt, the inventory in Guangdong fell by 4,900 mt to 16,200 mt, the inventory in Chengdu increased by 100 mt to 1,100 mt, and the inventory in Tianjin added by 400 mt to 700 mt due to the eased pandemic.

Looking forward, all industries are required to withdraw funds approaching the end of June, so the market will see more sellers and less buyers, and the weekly inventory next week will stop falling and rise.

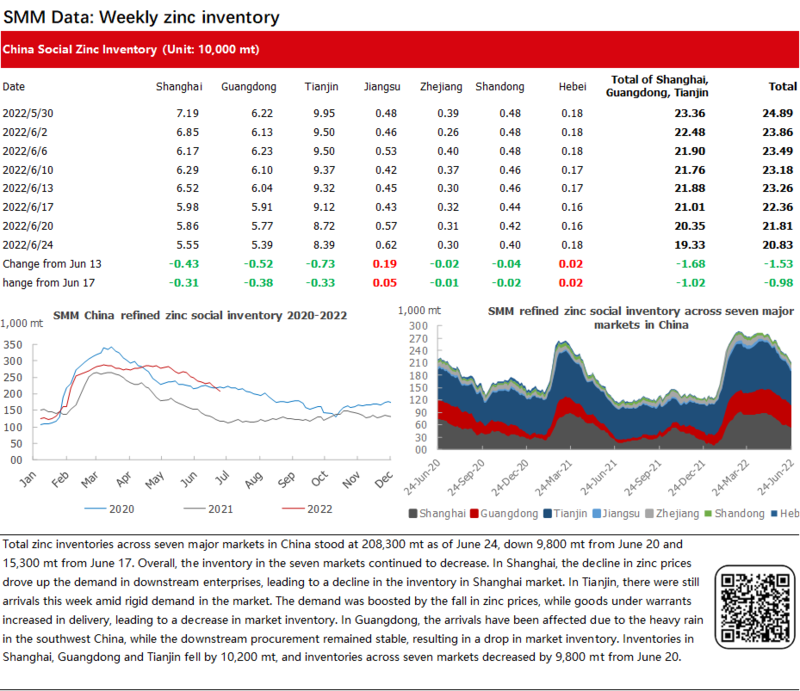

Inventories of Zinc Ingot across Seven Major Markets in China Decreased 9,800 mt from June 20

Total zinc inventories across seven major markets in China stood at 208,300 mt as of June 24, down 9,800 mt from June 20 and 15,300 mt from June 17.

Overall, the inventory in the seven markets continued to decrease.

In Shanghai, the decline in zinc prices drove up the demand in downstream enterprises, leading to a decline in the inventory in Shanghai market. In Tianjin, there were still arrivals this week amid rigid demand in the market. The demand was boosted by the fall in zinc prices, while goods under warrants increased in delivery, leading to a decrease in market inventory. In Guangdong, the arrivals have been affected due to the heavy rain in the southwest China, while the downstream procurement remained stable, resulting in a drop in market inventory.

Inventories in Shanghai, Guangdong and Tianjin fell by 10,200 mt, and inventories across seven markets decreased by 9,800 mt from June 20.

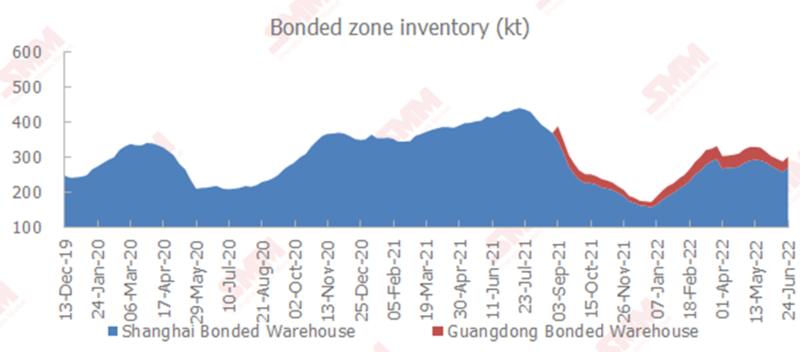

Copper Inventories in Domestic Bonded Zones Increased 2,400 mt over Weekend

Copper inventories in domestic bonded zones increased by 2,400 mt from last Friday June 17 to 303,600 mt as of June 24, according to SMM survey. The inventory in the Shanghai bonded zone rose by 1,200 mt to 271,500 mt WoW, and that in Guangdong added 1,200 mt to 32,100 mt WoW. Last week, shipments flowing in and out of the bonded warehouses increased. Spot imports have remained profitable since two weeks ago. Domestic importers have actively moved the goods in the bonded warehouses into China, including many non-standard and unregistered goods. Last week, goods arrived at ports in a centralised way, so the arrival increased WoW.

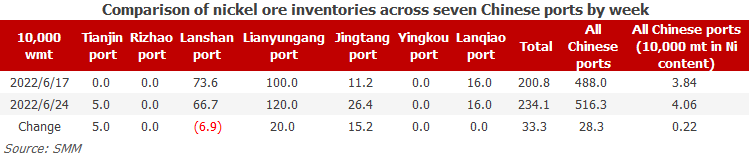

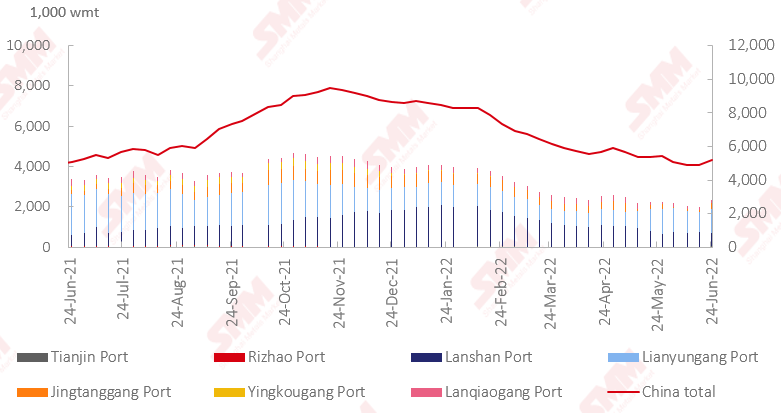

Nickel Ore Inventories at Chinese Ports up 283,000 wmt WoW

As of June 24, port inventories of nickel ore in China increased by 283,000 wmt to 5.163 million wmt compared with last week. The total Ni content added by 2,000 mt to 40,600 mt. The total inventory was still at a historically low level. The port inventory of nickel ore across seven major Chinese ports stood at 2.341 million wmt, 333,000 wmt higher than last week. Shipments from the Philippines were gradually recovering. However, due to the impact of the rainy season in the first half of the year, the imports of nickel ore fell short of expectations, which further led to the continuous decline in nickel ore inventory at ports and the limited in-plant inventories in the factories. Previous orders of nickel ores are delivered, and goods are picked up in the factory, hence the port inventory cannot increase. In addition, on the demand side, NPI plants and steel mills purchased on rigid demand in the poor NPI and stainless steel markets, which suppressed the shipments from mines. Upstream and downstream mainly held a wait-and-see sentiment. In the short term, port inventory of nickel ore is expected to increase gradually. However, the overall inventory will still remain low, and the tight supply of nickel ore is difficult to ease in the short term.

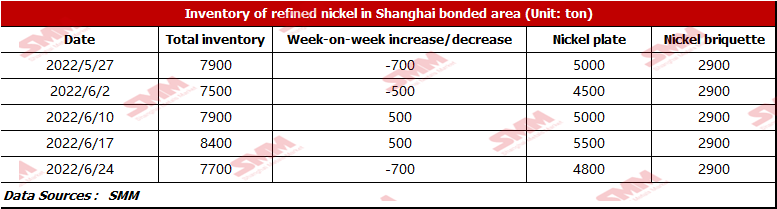

Bonded Zone Inventory Increased Slightly due to Weak Demand for Pure Nickel

Because of the macro factors, nickel prices in domestic and overseas markets continued to fall this week, and the imports of pure nickel spot remained profitable. According to SMM research, the bonded zone inventory stood at 7,700 mt this week. The inventory of nickel briquette was 2,900 mt, and that of nickel plate was 4,800 mt, a decrease of 700 mt WoW. The decrease in nickel plate inventory was caused by the less arrival of pure nickel and the downstream’s purchases on rigid demand. SMM expects that the spot imports will remain profitable next week, and some overseas nickel plates will flow into the bonded zone warehouses.