SHANGHAI, Jun 17 (SMM) - This is a roundup of China's metals weekly inventory as of June 17.

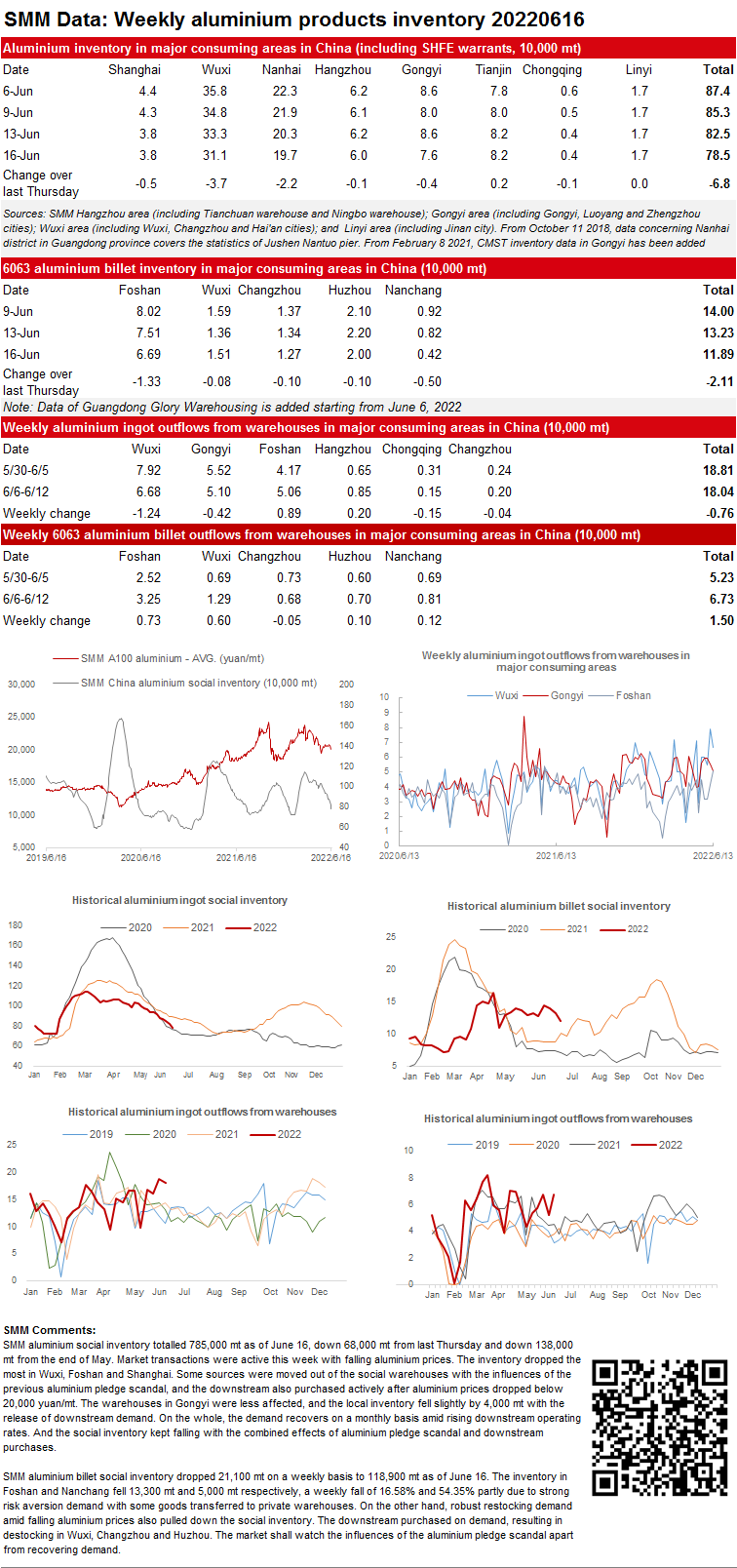

Both Aluminium and Aluminium Billet Inventories Dropped on A Weekly Basis

SMM aluminium social inventory totalled 785,000 mt as of June 16, down 68,000 mt from last Thursday and down 138,000 mt from the end of May. Market transactions were active this week with falling aluminium prices. The inventory dropped the most in Wuxi, Foshan and Shanghai. Some sources were moved out of the social warehouses with the influences of the previous aluminium pledge scandal, and the downstream also purchased actively after aluminium prices dropped below 20,000 yuan/mt. The warehouses in Gongyi were less affected, and the local inventory fell slightly by 4,000 mt with the release of downstream demand. On the whole, the demand recovers on a monthly basis amid rising downstream operating rates. And the social inventory kept falling with the combined effects of aluminium pledge scandal and downstream purchases.

SMM aluminium billet social inventory dropped 21,100 mt on a weekly basis to 118,900 mt as of June 16. The inventory in Foshan and Nanchang fell 13,300 mt and 5,000 mt respectively, a weekly fall of 16.58% and 54.35% partly due to strong risk aversion demand with some goods transferred to private warehouses. On the other hand, robust restocking demand amid falling aluminium prices also pulled down the social inventory. The downstream purchased on demand, resulting in destocking in Wuxi, Changzhou and Huzhou. The market shall watch the influences of the aluminium pledge scandal apart from recovering demand.

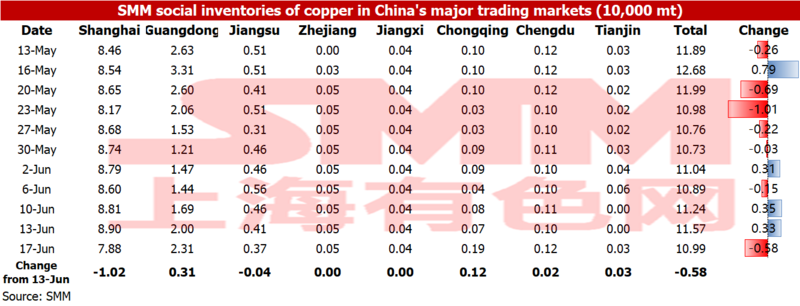

Copper Inventory in Major Chinese Markets Dipped 5,800 mt from Monday

As of Friday June 17, SMM copper inventory across major Chinese markets stood at 109,900 mt, down by 5,800 mt from Monday and down by 2,500 mt from last Friday. Compared with Monday's data, the inventories in most regions of China increased, but only the inventory in Shanghai and Jiangsu decreased. The total inventory dropped by 170,200 mt compared with the same period last year when the inventory was recorded at 280,100 mt. Among them, the inventory in Guangdong dropped by 72,100 mt, the inventory in Shanghai dipped by 67,400 mt, and the inventory in Jiangsu dropped by 20,200 mt. The inventory in Shanghai and Jiangsu dropped sharply this week as the copper prices plummeted and the downstream companies in these areas were active in restocking with the improvement of the pandemic. While the inventory in other places of China increased slightly because the recovery of consumption was less than expected.

In detail, the inventory in Shanghai dropped by 10,200 mt to 78,800 mt, the inventory in Guangdong increased by 3,100 mt to 23,100 mt, the inventory in Jiangsu fell by 400 mt to 3,700 mt, the inventory in Chongqing increased by 1,200 mt to 1,900 mt, and the inventory in Tianjin rose by 300 mt to 300 mt as the pandemic in this city has been eased somewhat.

Looking forward, the arrival next week will still increase. If the consumption continues to recover, the inventory will fall further.

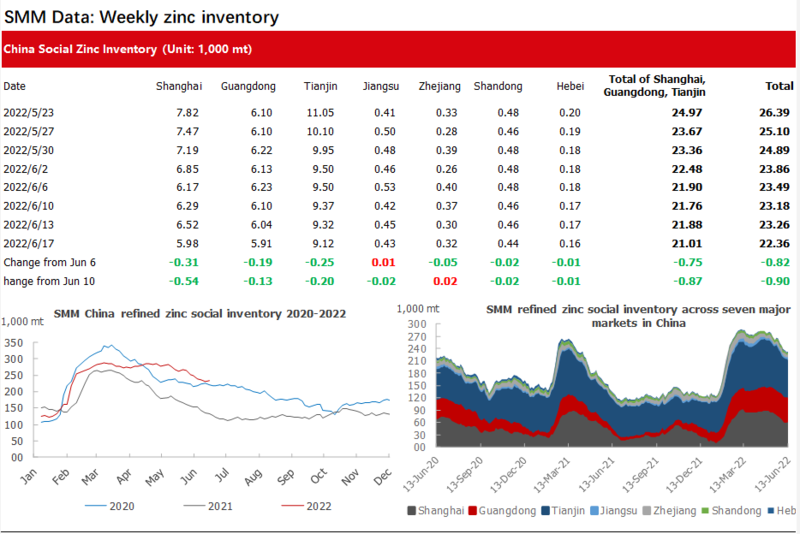

Inventories of Zinc Ingot across Seven Major Markets in China Dropped 9,000 mt from June 13

Total zinc inventories across seven major markets in China stood at 223,600 mt as of June 17, down 9,000 mt from June 13 and 8,200 mt from June 10.

Overall, the inventory in the seven markets decreased slightly.

In Shanghai, when the zinc prices moved in a downward trend, most downstream enterprises restocked actively, driving down the inventory in Shanghai. In Tianjin, due to the resurgence of the pandemic in Inner Mongolia, the arrivals in the Tianjin market decreased, and inventory in Tianjin market dropped amid stable purchases. In Guangdong, the arrivals decreased slightly in the market after the maintenance at Mengzi smelter, and the fall in zinc prices encouraged downstream companies to restocking, leading to the decrease in the inventory of Guangdong.

Inventories in Shanghai, Guangdong and Tianjin fell by 8,700 mt, and inventories across seven markets decreased by 9,000 mt.

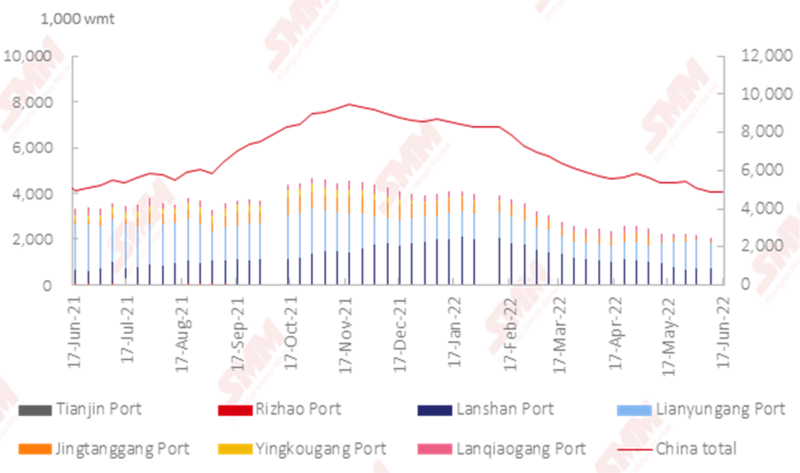

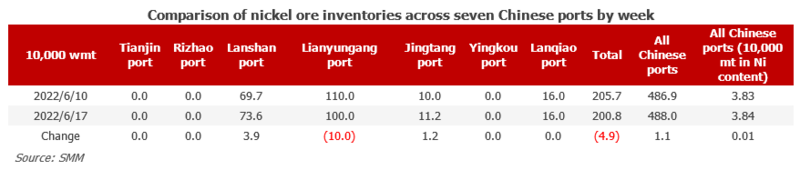

Nickel Ore Inventories at Chinese Ports Fell 11,000 wmt WoW

As of June 17, port inventories of nickel ore in China dropped by 11,000 wmt to 4.88 million wmt compared with last week. The total Ni content stood at 38,000 wmt. The port inventory of nickel ore across seven major Chinese ports stood at 2,008,000 wmt, 49,000 wmt lower than last week. Nickel ore supply still did not become sufficient when the rainy season ended in the Philippines. According to SMM research, the supply gap of nickel ore is mainly contributed by the poor weather conditions in the Philippines in the first half of 2022. The falling nickel ore inventory at ports indicates that the supply of nickel ore this year is always tight, which can hardly be eased in the short term. According to some traders, the shipment of nickel ore from the Philippines in the first half of 2022 was far lower than expected, and the damage to local infrastructure in the Philippines caused by poor weather conditions needed time to be repaired. In China, the production of NPI keeps releasing demand, while the falling nickel ore prices may not boost shipments from the mines, hence the market cannot see a short-term supply surplus of nickel ore.

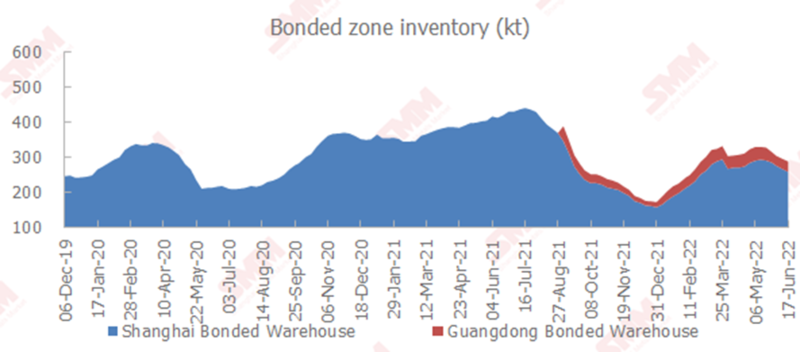

Copper Inventory in Domestic Bonded Zone up 13,800 mt

Copper inventories in domestic bonded zones increased by 13,800 mt from last Friday June 10 to 301,200 mt as of June 17, according to SMM survey. The inventory in the Shanghai bonded zone rose by 12,500 mt to 270,300 mt WoW, and that in Guangdong added 1,300 mt to 30,900 mt WoW. The increase in bonded zone inventory was contributed by the inflow of cancelled warrants of LME Asian warehouses to China. Besides, there are still some goods waiting to be moved into warehouses. It is expected that the bonded zone inventory will further increase. In addition, the working efficiency of Shanghai bonded zone warehouses has completely returned to normal.

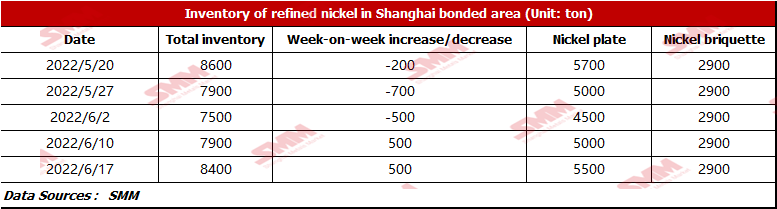

Imports of Nickel Spot Gained Profits and Bonded Zone Inventory of Nickel Plate Increased

Due to the Fed's interest rate hikes, the prices of LME and SHFE nickel kept falling this week, and the imports of pure nickel spot continued to gain profits. According to SMM research, the bonded zone inventory stood at 8,400 mt this week. The inventory of nickel briquette was 2,900 mt, and that of nickel plate was 5,500 mt, an increase of 500 mt WoW. This week, the increase in nickel plate inventory was mainly due to the arrival of nickel plates from domestic traders. In addition, the falling nickel prices picked up the downstream purchase. SMM expects that the spot imports will remain profitable this week, and there will be some overseas nickel plates flowing into the bonded zone warehouses.