SHANGHAI, Jun 10 (SMM) - This is a roundup of China's metals weekly inventory as of June 10.

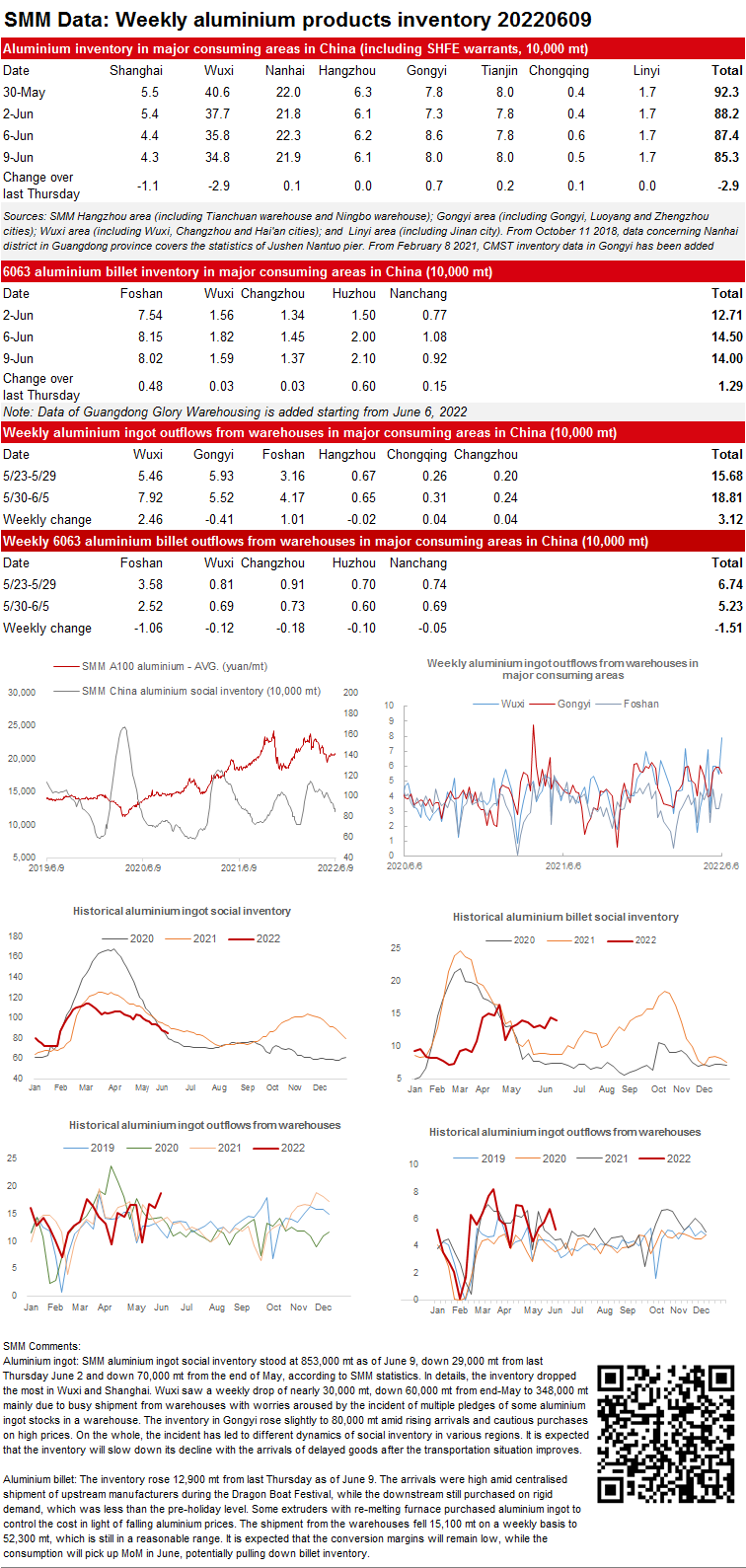

Aluminium Ingot Inventory Dropped while Billet Stocks Rose WoW

Aluminium ingot: SMM aluminium ingot social inventory stood at 853,000 mt as of June 9, down 29,000 mt from last Thursday June 2 and down 70,000 mt from the end of May, according to SMM statistics. In details, the inventory dropped the most in Wuxi and Shanghai. Wuxi saw a weekly drop of nearly 30,000 mt, down 60,000 mt from end-May to 348,000 mt mainly due to busy shipment from warehouses with worries aroused by the incident of multiple pledges of some aluminium ingot stocks in a warehouse. The inventory in Gongyi rose slightly to 80,000 mt amid rising arrivals and cautious purchases on high prices. On the whole, the incident has led to different dynamics of social inventory in various regions. It is expected that the inventory will slow down its decline with the arrivals of delayed goods after the transportation situation improves.

Aluminium billet: The inventory rose 12,900 mt from last Thursday as of June 9. The arrivals were high amid centralised shipment of upstream manufacturers during the Dragon Boat Festival, while the downstream still purchased on rigid demand, which was less than the pre-holiday level. Some extruders with re-melting furnace purchased aluminium ingot to control the cost in light of falling aluminium prices. The shipment from the warehouses fell 15,100 mt on a weekly basis to 52,300 mt, which is still in a reasonable range. It is expected that the conversion margins will remain low, while the consumption will pick up MoM in June, potentially pulling down billet inventory.

Copper Inventory across Major Chinese Markets Added 3,500 mt from Monday

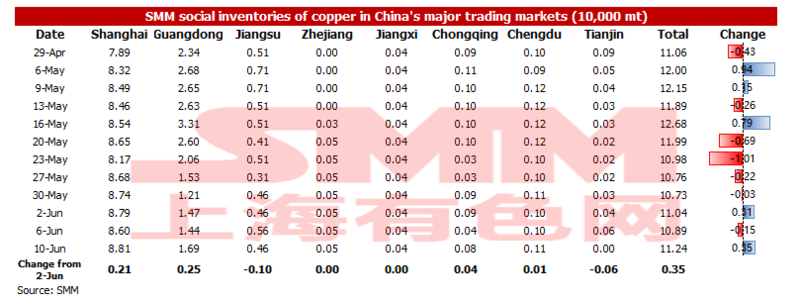

As of Friday June 10, SMM copper inventory across major Chinese markets increased by 3,500 mt from Monday to 112,400 mt, up by 2,000 mt from last Friday. The increase in inventory was contributed by the production resumption of smelters and the poor downstream consumption. Compared with Monday's data, the inventories in most regions of China increased, while the inventory in Jiangsu and Tianjin decreased slightly. The total inventory dropped by 181,400 mt compared with the same period last year when the inventory was recorded at 293,800 mt. Among them, the inventory in Guangdong dropped by 82,400 mt, the inventory in Shanghai dipped by 66,500 mt, and the inventory in Jiangsu dropped by 19,300 mt. In June 2022, the inventory bottomed out, while during the same period last year, the inventory kept declining. SMM expects that the inventory will continue to rise. On one hand, the market has not seen any improvement in downstream consumption at present. On the other hand, the supply is increasing as smelters have resumed their production.

In detail, the inventory in Shanghai increased by 2,100 mt to 88,100 mt, the inventory in Guangdong rose by 2,500 mt to 16,900 mt, the inventory in Chongqing increased by 400 mt to 800 mt, while the inventory in Tianjin decreased by 600 mt to 0 mt due to the pandemic outbreak in Chifeng.

Looking forward, approaching the delivery of the 2206 copper contract, smelters will increase their shipments, but the downstream consumption cannot improve. Therefore, the inventory will still increase next week.

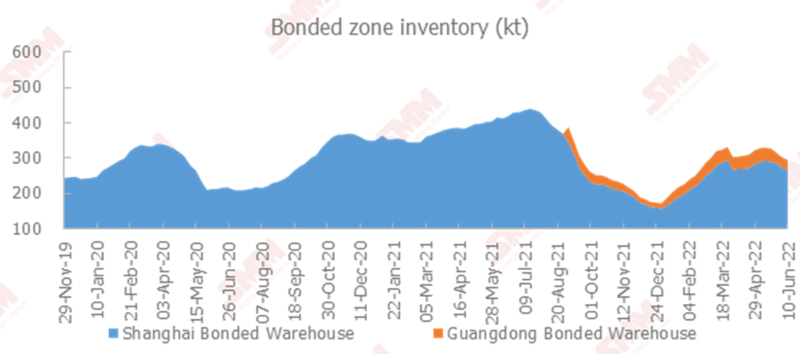

Copper Inventory in China Bonded Zone Dropped by 7,400 mt on Week

Copper inventories in domestic bonded zones decreased by 7,400 mt from last Thursday June 2 to 287,400 mt as of June 10, according to SMM survey. The inventory in Shanghai bonded zone decreased by 7,500 mt to 257,800 mt, while that in Guangdong added 100 mt to 29,600 mt. The price ratio was favourable for imports this week, and some warrants were declared and imported into China, resulting in a further decline in the bonded zone inventory. In addition, the efficiency of pick-up at bonded warehouses continued to improve. The market should pay attention to the flowing of cancelled warrants of LME Asia warehouses into China, which may end the decline in bonded zone inventory.

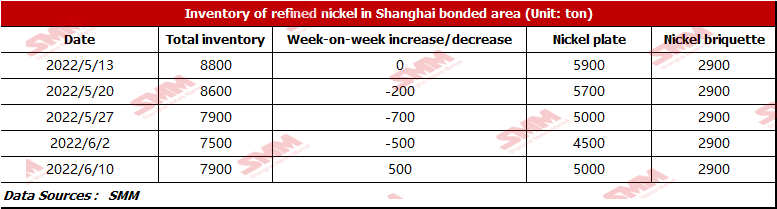

Imports of Pure Nickel Spots Remained Profitable, and Bonded Zone Inventory Increased Slightly

LME nickel prices kept falling this week, while SHFE nickel prices remained rangebound at high levels, hence the spot imports of pure nickel gained profits. According to SMM research, the bonded zone inventory stood at 7,900 mt this week. The inventory of nickel briquette was 2,900 mt, and that of nickel plate was 5,000 mt, an increase of 500 mt WoW. The increase in inventory of nickel plate was contributed by the arrival of domestic traders' nickel plate. However, due to the high SHFE nickel prices and the high pure nickel spot prices, the downstream purchase was less than expected, and the customs clearance volume decreased this week.

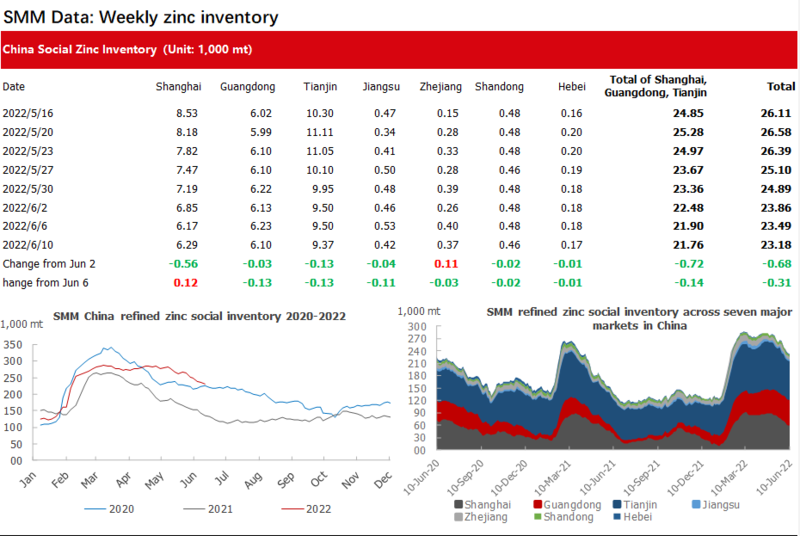

Inventories of Zinc Ingots across Seven Major Markets in China Decreased 3,100 mt from June 6

Total zinc inventories across seven major markets in China stood at 231,800 mt as of June 10, down 3,100 mt from June 6 and 6,800 mt from June 2.

Overall, the inventory in the seven markets continued to decrease.

In Shanghai, the market were reluctant to restock cargoes. Traders and downstream companies mostly remained wait-and-see with poor transactions. At the same time, inventories were transferred to other warehouses in Shanghai, and the market inventory increased slightly. In Tianjin, the market arrivals decreased slightly, while the downstream was restrained by high zinc prices. Enterprises mainly consumed raw material inventories and were less active in purchasing. But the purchases on rigid demand still led to a small reduction in the inventory of Tianjin market. In Guangdong area, some stockholders were active in selling off goods affected by the repeated pledge of goods, and the downstream sector restocked on rigid demand occasionally. But the inventory reduced slightly amid sluggish orders.

Inventories in Shanghai, Guangdong and Tianjin fell by 1,400 mt, and inventories across seven markets decreased by 3,100 mt.

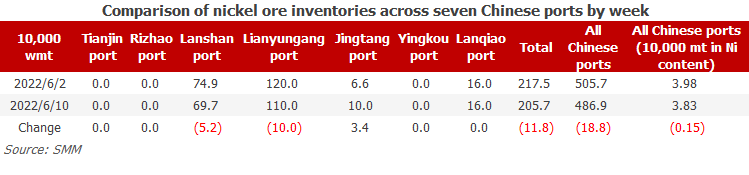

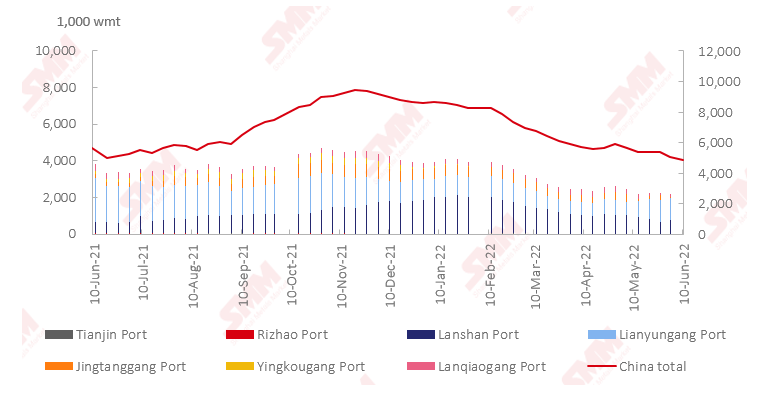

Nickel Ore Inventories at Chinese Ports Fell 188,000 wmt WoW

As of June 10, port inventories of nickel ore in China dropped by 188,000 wmt to 4,869,000 wmt compared with last week. The total Ni content fell by 1,000 mt to 38,300 mt. The nickel ore inventory was at a historically low level last week. The port inventory of nickel ore across seven major Chinese ports stood at 2.057 million wmt, 118,000 wmt lower than last week. At present, the shipment of nickel ore from the Philippines has resumed as the impact of the rainy season in the country has disappeared. However, the arrival of some nickel ores is less than expected, and the supply of ships is tight. On the demand side, the NPI plants picked up goods in time, and they mainly consumed the nickel ore at ports to secure their in-plant inventory. In the short term, the port inventory of nickel ore will remain rangebound at low levels.