SHANGHAI, Dec 10 (SMM) - SMM believes that in 2021, the domestic zinc mining side will still maintain a tight balance, and the shortage of domestic zinc ore supply may ease by 2023.

Recovery from COVID-19 pandemic

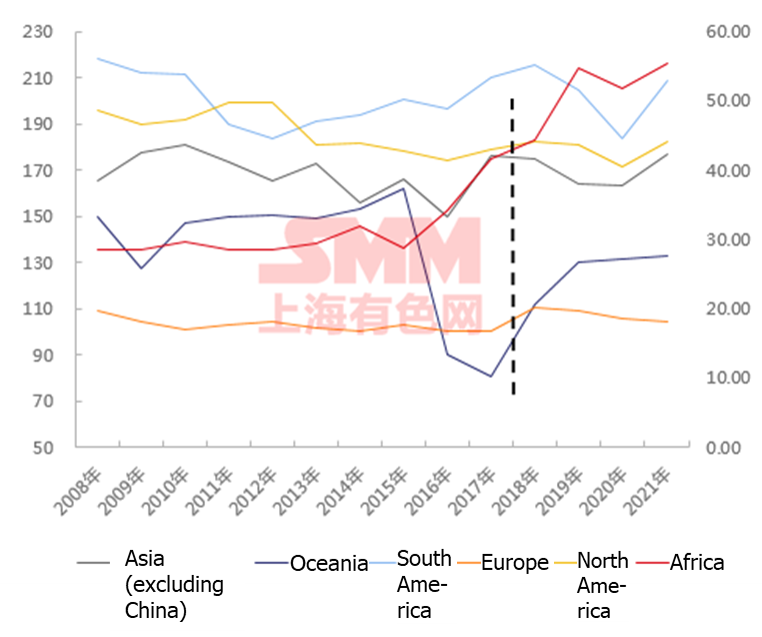

2021 is the first year of economic recovery after breakout of COVID-19 pandemic. The recovery of global production is mainly contributed by the resumed production from COVID. According to SMM statistics on the output of overseas mines from 2008 to 2021, although the mines have resumed production after the pandemic, the output of zinc mines in 2021 has not returned to the level of 2019 due to factors like repeating pandemic and falling grade.

Entering 2022, as the global vaccination rate increases further, more small mines in Peru, Bolivia and other regions are expected to resume production, bringing additional output.

Production recovery in Oceania and Europe fell short of expectations

SMM has been monitoring the zinc output changes in Asia (excluding China), Oceania, South America, Europe, North America and Africa, and it can be concluded that the recovery of production in Oceania and Europe has obviously fallen short of expectations.

Overseas mines were put into production one after another, but the ore grade has been falling as well

Statistics on the output of major mines from 2016 to 2021 show that in recent years, there have been overseas mines being put into production, but the ore grade was also falling.

According to SMM survey, in the upcoming 2022, the total output of overseas mines is expected to reach 215,700 mt.

Domestic mines’ output demonstrated palpable seasonal fluctuations

In 2021, the resumption of domestic zinc mines’ production was basically in line with expectations. However, due to the dual control of energy consumption and power rationing this year, the increase in output did not meet the estimate at the beginning of the year. Both the domestic mines’ output and treatment charges showed palpable seasonal fluctuations.

Measuring the inflow of imported ore by observing the inventory changes at Lianyungang Port

As China's Lianyungang Port is the main storage place for imported zinc concentrates, there is a strong correlation between the import volume of zinc concentrates and the inventory at Lianyungang Port. The inflow of imported ore can be estimated by looking at the inventory changes at this port.

In November, as the losses of imported ore expanded, the imports were restrained to some point. However, the output of domestic smelters continued to increase, hence the demand for zinc concentrate was robust. Meanwhile, the overseas supplies of goods under long-term contracts will arrive in China from November to December. Therefore, SMM predicts that the import volume of zinc concentrate in November may be around 300,000 mt.

Recovery of domestic zinc ore output was slow due to COVID and dropped grade

According to SMM statistics, the output of domestic mines in 2020 increase slightly by 24,000 mt from 2019. The recovery of domestic zinc ore output was slow in 2020 mainly due to problems such as the repeating COVID and the decline in zinc ore grade.

Under the rise of auxiliary materials prices, the domestic ore cost curve has been raised by 700-1000 yuan/mt in metal content

Against the background of rising prices of chemical auxiliary materials, it is not difficult to see from SMM statistics that China's zinc ore cost curve in 2021 has been raised by 700 to 1,000 yuan per metal ton.

In addition, SMM also made some statistics on the variables of the new and expaded domestic zinc mines from 2020 to 2022. In 2021, the new projects or expansion of domestic zinc mines will bring another 60,000 mt of capacity in metal content, and the number will reach 169,000 mt in 2022 in metal content.

Domestic smelters’ annual output fell short

According to SMM statistics, in 2021, due to power restrictions and shrinking profits, the annual increase in domestic refined zinc output was seriously lower than expected.

Looking into 2022, if the impact of the power cut is lifted and some smelters are put into operation, SMM expects that the increase in zinc ingot production can reach about 200,000 mt.

Production progress of domestic smelters

According to SMM statistics on the commissioning of domestic smelters, the total production capacity of hot-dip galvanised alloy is 950,000 mt/year, and the total production capacity of die-casting zinc alloy is 280,000 mt/year. In addition, from 2022 to 2026, many refined zinc smelters also have their own expansion plans with varying increment targets.

Overseas zinc output increased YoY in post-COVID era

In 2021, overseas smelters gradually resumed production after serious COVID-19 pandemic in 2020, which will drive up the production of overseas zinc ingots slightly year-on-year. However, in Europe, with the rapid rise in electricity prices since September, the comprehensive smelting profits of smelters in the region have declined severely.

Output changes of some overseas zinc smelters in 2022

According to SMM statistics on the output changes of some overseas zinc smelters in 2022, the output of some overseas zinc smelters in 2022 is expected to increase by about 135,100 mt compared with 2021.

Demand-supply balance

SMM believes that in 2021, the domestic mining side will still maintain a tight balance, and the shortage of domestic supply may ease by 2023.

![Supply-Side Support Pushed the Zinc Price Center Higher [SMM Weekly Zinc Commentary]](https://imgqn.smm.cn/usercenter/tAyyp20251217171754.jpg)

![[SMM Conference] PbZn Conference 2026 Gathers Global Leaders to Navigate Evolving Market Dynamics](https://imgqn.smm.cn/production/admin/votes/imagesbznIX20260330170246.jpeg)