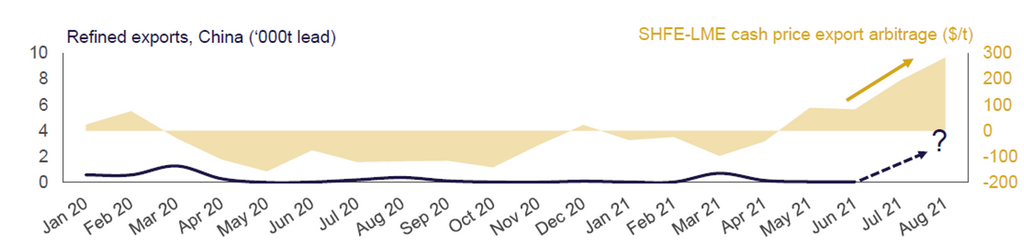

SHANGHAI, Sep 3 (SMM) – SHFE/LME lead price ratio kept falling since the beginning of this year. The price ratio hit 7.9 in March, and then slid to around 6.5. The extremely low price ratio led to substantial losses in lead imports, and the export profits of lead ingot gradually increased.

Global supply of lead ingot was tight, while the domestic supply increased this year, and the production capacities of secondary and primary lead expanded simultaneously. However, domestic consumption did not keep up with the supply, and lead ingot inventories kept rising, weighing on lead prices. The gap between domestic and overseas lead ingot inventories has been widened for many weeks. The premiums of three-month LME lead has risen over $100/mt, and the premiums in US is around $400/mt (17-19 cents/lbs).

As spot premiums in Europe, America and Southeast Asia stand at a relatively high level, the profits of lead ingot exports will be slightly higher than that of the delivery in LME market.

After SHFE/LME price ratio fell below 7 in May, the exports of lead ingot did not reported significant increase from June to August, which meant that the actual trade and transportation was impeded. The pandemic caused the shortage of containers, which coupled with the longer shipping cycle drove up the ocean freight sharply. The unsmooth operation process led to the lower export volume of lead ingot, and the SHFE/LME price ratio recovered slowly.

According to SMM survey, the ocean freight for 20GP containers exported to Europe in September is about $8,300, and the ocean freight for exports to the United States is about $16,500. The scheduled period is about half a month. This means that the actual export costs to Europe and the United States around $374/mt and $717/mt respectively. Therefore, the soaring ocean freights have curbed the large-scale exports in the trade market despite the high premiums in Europe and US. The freight rate for 20GP containers to Southeast Asia is about $850. However, due to the high premiums of local deliveries, there is increase in the warrants in the LME delivery warehouses in Singapore, and the warrants is expected to stay flat.

Therefore, amid the recent imbalance between the domestic and overseas markets, the decrease in the imports of lead concentrate and silver concentrate is the main adjustment method. The insufficient supplement of imported concentrates has caused the TCs for domestic lead concentrate to remain low, giving domestic lead prices a certain degree of support. If the ocean freights fall back from high levels, lead ingots may still be exported in large scales with the export tariffs removed. Trade market is paying attention to the logistics conditions. SMM expects that the export volume of lead ingot from August to October may not exceed 20,000 mt, which will have a limited impact on the domestic lead ingot balance.

LME lead may also surge and fall back if the overseas pandemic is controlled and the demand recovers. The recent fund disturbance is worth attention. SHFE/LME lead price ratio is expected to rebound slightly with the transfer of lead ingots, but the decline in domestic inventories is limited, which still weighs on lead prices. LME prices may continue to exceed SHFE prices. Prices of the most traded SHFE lead contract is expected to fluctuate between 14,800-15,800 yuan/mt in the short term, and three-month LME lead is expected to move between $2,150-2,350/mt.

![Secondary Lead Prices Inverted Against Primary Lead Prices, Lead Market Fluctuated Amid a Tug-of-War Between Sellers and Buyers [SMM Lead Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/xVUpr20251217171722.jpg)

![LME lead fluctuated upward to close higher, while SHFE lead moved downwards after a higher opening and remained in the doldrums [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)