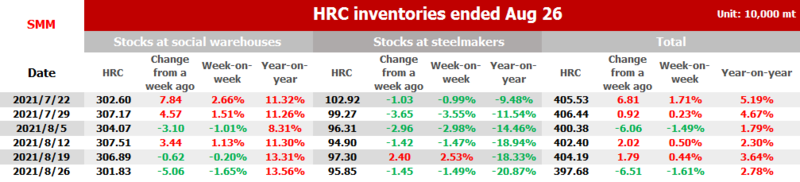

SHANGHAI, Aug 27 (SMM) – HRC stocks across Chinese social warehouses and steel makers declined 65,100 mt or 1.61% on the week, but increased 2.78% from a year ago, to 3.98 million mt as of August 26, according to SMM data.

Some steel mills in north China conducted maintenance on rolling lines this week, while several steel mills in south China slightly recovered production. The overall HRC output declined. At the same time, HRC prices rebounded from low levels, spot transactions improved slightly, and total HRC inventories fell again.

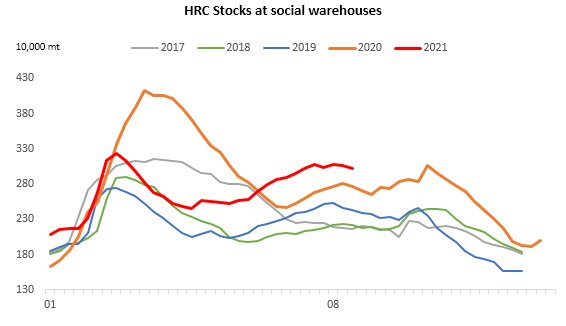

Inventories across social warehouses decreased 50,600 mt or 1.65% from a week earlier to 3.02 million mt. This is up 13.56% from the same period last year.

The COVID-19 pandemic eased in east China, where the social inventories dropped significantly amid the recovered transportation and high restocking demand by end users. The social inventories in central and south-west China increased slightly, and the stocks in other regions across the country all fell.

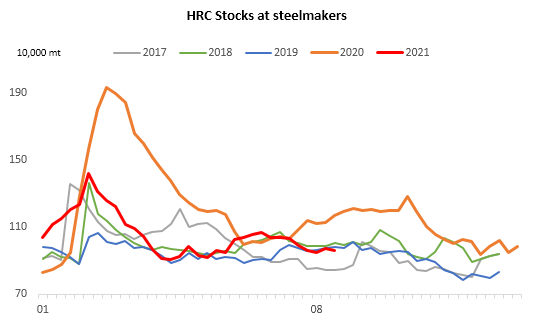

Stocks at Chinese steel makers came in at 958,500 mt, down 14,500 mt or 1.49% from a week earlier and 20.87% year on year.

The logistics were smooth in most regions amid the alleviated pandemic impact, and steel mills were actively shipping goods. The stocks in plants were transferred more rapidly to social warehouses, especially in east China. The inventory decline was significant in the plants in north-east China due to the maintenance.

HRC inventories declined amid rebounding end demand this week. According to SMM survey, the HRC output affected by maintenance is expected to be 1.06 million mt in September, up 92,000 mt from August. HRC output is likely to remain low.

On the demand side, the production in automobile industry is limited due to the chip shortage. The purchasing intentions of industries such as home appliances and machinery have not improved significantly, and the downstream has a weaker acceptance of high prices. The supply and demand of HRC is expected to remain low in the short term, and the downward room for inventories will be limited.