SHANGHAI, Oct 12 (SMM)—In this special report we present you our inventory and price movement updates on the China Metals industry after the National Day long holidays.

For more information on the China ferrous or nonferrous metals updates , please visit our website www.metal.com and our social media channels on Facebook, Linkedin and Twitter. We also encourage you to subscribe to our new weekly email newsletter updates- The SMM Midweek Roundup and the SMM China Inventory Summary & Data Wrap.

Steel: Overall inventories higher on expectation but prices to have upward momentum

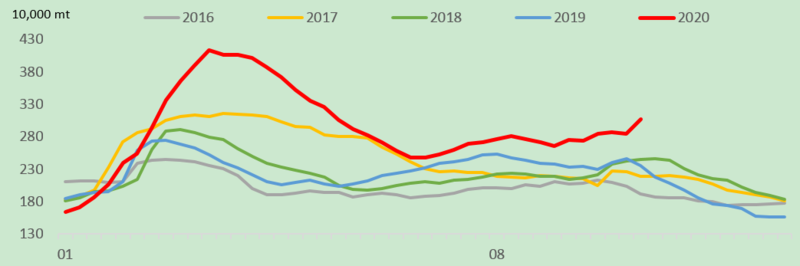

Inventories of hot-rolled coils (HRC) and plates across social warehouses and steelmakers, which are used in automobiles and home appliances, increased 6.94% or 281,900 mt from September 24 in the week ended October 9 to 4.06 million mt. Stocks were 27.3% higher than the same period last year.

HRC stocks across social warehouses increased 7.04% or 201,700 mt from September 24 in the week ended October 9 to 3.07 million mt. The stocks were 24.9% higher than the same period last year.

In-plant HRC inventories increased 6.69% or 80,300 mt from September 24 and rose 33.4% year on year to 1.28 million mt in the week ended October 9, showed SMM data.

End-user purchasing was more cautious, and the demand for restocking before the holidays was sluggish. Traders lacked confidence in the post-holiday market and procured cautiously, which led to the weak destocking of social and in-plant inventories.

HRC Social Inventory

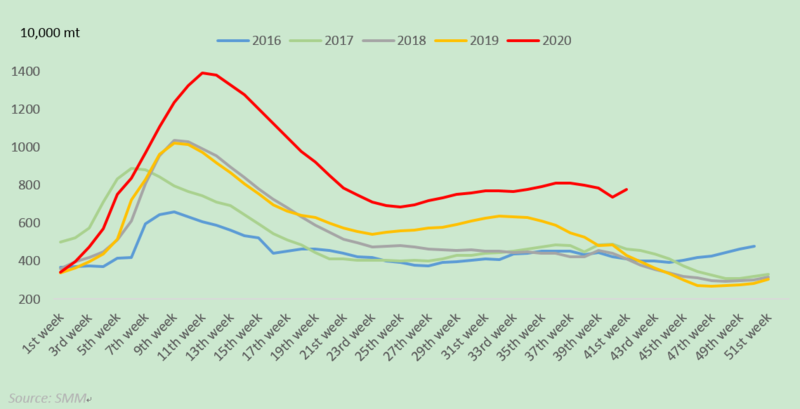

On the other hand, inventories of steel rebar across Chinese steelmakers and social warehouses also rose significantly during the National Day holidays. Inventories at Chinese steelmakers jumped 11.4% on the week and stood at 3.54 million mt. This was up 40.3% year on year.

Overall inventories of rebar, including stocks across steelmakers and social warehouses, grew 7.4% on the week and posted 11.33 million mt as of October 9.

Tougher environmental protection measures lifted steel billet prices in Tangshan by 70 yuan/mt, steel scrap prices by 50 yuan/mt and strip steel prices by 100 yuan/mt during the holidays, which in turn boosted the prices of finished steel products.

Because of tightening production restrictions, the weekly output of rebar and hot-rolled coil fell 133,000 mt and 45,000 mt respectively, which may ease supply pressure in coming weeks, while downstream consumers should look to restock after the holidays.

Coking plants across Shanxi, Hebei, Shandong started a new round of price increase of 50 yuan/mt. Some coal mines are bullish on coal prices as shutdowns during the holidays leave them with low inventories and as they expect tougher safety inspections in the future. Firm raw material prices also supported the prices of finished steel products.

In the short-term, steel prices still have upward momentum, but face risks of falling back from highs after market optimism fades if the destocking falls short of expectations.

Rebar Social Inventory

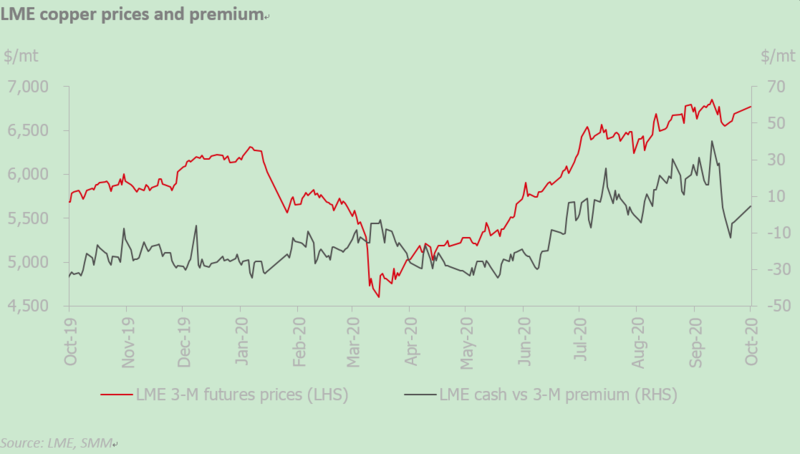

Copper: Prices met resistance amid high LME inventory

SMM data showed that copper stocks added 9,000 mt from September 30 to 309,000 mt as of Friday October 9. Stocks of copper in Shanghai bonded areas increased for the ninth consecutive week ahead of the long holidays. Stocks are expected to rise further after warehouses resume operations from the holidays.

Base metals weakened across the board on October 1, but subsequently recovered while China was on holiday and closed at $6,648/mt as of October 9, down $38/mt from September 30, a decrease of 0.57%.

Risk appetite is likely to bolster copper prices in the near term, however, copper fundamentals are not so strong currently. LME copper inventory increased for three consecutive days to 166,000 mt before National Day holidays and cancelled warrants fell to around 20%. LME copper inventory dipped during the holiday but high inventories continued to weigh on copper prices. Weak consumption is likely to grow domestic inventory pressure amid the absence of market optimism over copper semis in October.

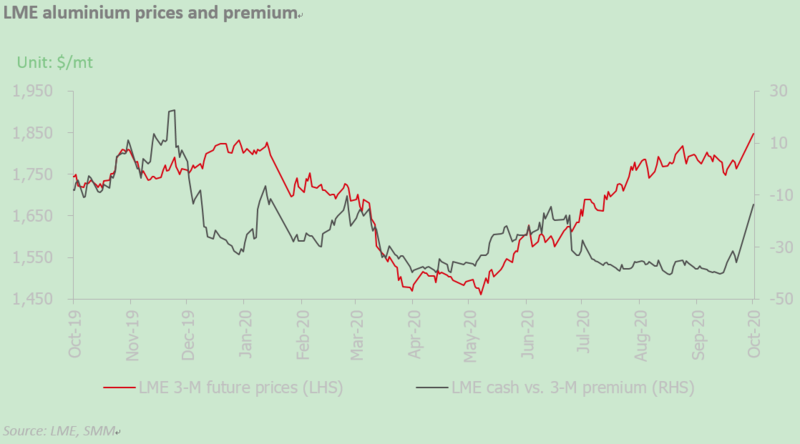

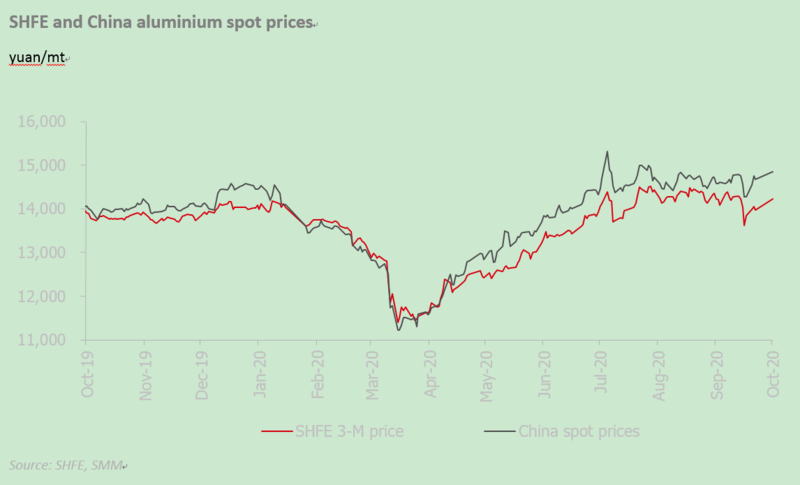

Aluminium: Consumption weaker than expectations

SMM data showed that aluminium ingot social inventories totalled 715,000 mt on October 9, an increase of 60,000 mt during the holidays, but the increase was smaller than the growth of 75,000 mt recorded in the same period last year. Major consumption hubs, such as Wuxi and Gongyi, saw limited arrivals.

On the cost side, alumina market was quiet before the holidays and overseas alumina prices continued to drop slightly. Based on demand from aluminium smelters and alumina production, alumina market is expected to maintain stable supply and demand and prices. SMM will monitor the impact on alumina prices from policies regarding production controls in the winter heating season.

Consumption across the aluminium extrusion, aluminium plate/sheet, strip, foil, wire and cable sectors was weaker than expected in the traditional high season of September. The latest SMM survey shows that downstream producers are not optimistic over consumption in October.

Domestic aluminium prices are likely to remain firm in the first week after the holidays amid low social inventories.

In the post-holiday spot market, spot premiums remained high at around 200/mt over the SHFE front-month aluminium contract. SHFE aluminium maintained a backwardation structure. SHFE aluminium prices fluctuated at highs after holidays as aluminium inventory accumulation during the holiday was weaker than the same period last year

LME aluminium fell to $1,725/mt on October 1 before drifting higher in the following days. As of CST 4 pm on October 8, LME aluminium hit a high of $1,805.5/mt, recovering all the losses during the holidays and refreshing the highest level since mid-September, with a cumulative increase of over 0.9%.

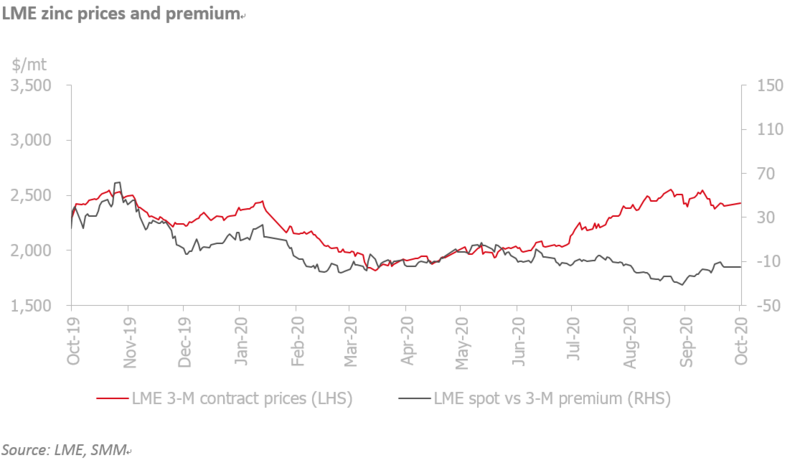

Zinc: Inventories to decline amid increase in consumption

Zinc inventories across seven Chinese markets rose sharply after the National Day holidays, especially in Guangdong and Tianjin.

Stocks in Shanghai, Guangdong and Tianjin rose 15,300 mt and inventories across the seven domestic markets increased sharply by 19,500 mt. Stocks in Shanghai, Guangdong and Tianjin rose 15,300 mt. Stocks across the three major trading hubs (Shanghai, Tianjin and Guangdong) rose 15,300 mt this week, after a 12,200 mt decrease last week.

Output at smelters in Guangdong remained high and price spread between Shanghai and Guangdong shrank sharply before the holidays.

Inventories in Tianjin declined but the overall stocks rose sharply as part of pricing cargo resource directly shipped to downstream buyers before the holidays.

Inventories are likely to decline further amid post-holiday restocking by downstream buyers and bullish infrastructure sector consumption. Zinc supply was tight as domestic TCs (treatment charges) declined further. Zinc prices are expected to fluctuate at highs in the short term.

LME zinc stocks rose for 3 consecutive days during the holidays, and the current stocks rose 2,150 mt to 218,400 mt compared with pre-holiday.

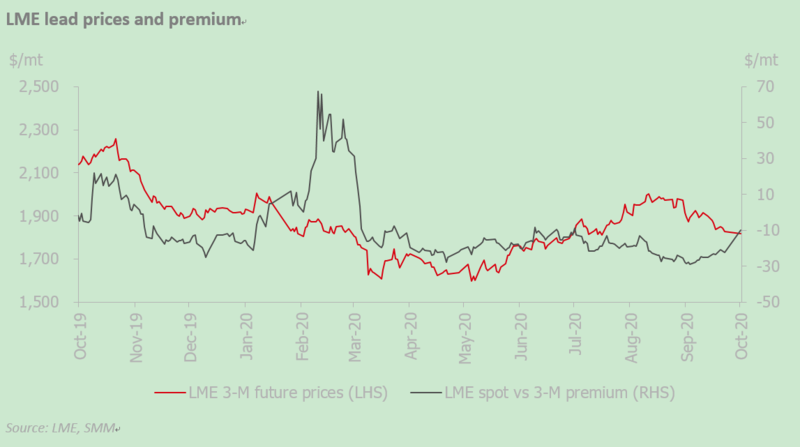

Lead: Secondary lead capacity expanded and consumption weakened

Fundamentals have weakened over the long holidays. Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin rose 2,700 mt from September 30 to 25,700 mt as of Friday October 9.

Lead-acid battery makers took 1-3 days off during the National Day holidays, while most of the lead smelters kept normal deliveries, reducing shipments from social warehouses. Some sellers became more willing to deliver cargoes to social warehouses as they lowered expectations for strong consumption after the holidays.

Treatment charges (TCs) for domestic lead concentrate fell 100 yuan/mt(in lead content) to 2,050 yuan/mt(in lead content). The increase in supply was mainly form secondary lead rather than primary lead. The new capacity of secondary lead in Anhui and Inner Mongolia expanded gradually after holidays.

Most of the battery makers completed stockpiling before holidays and lead-acid battery consumption weakened. Restocking and purchasing at producers will be follow.

Lead prices are expected to decrease amid higher supply from new capacity of secondary lead, and weak downstream consumption.

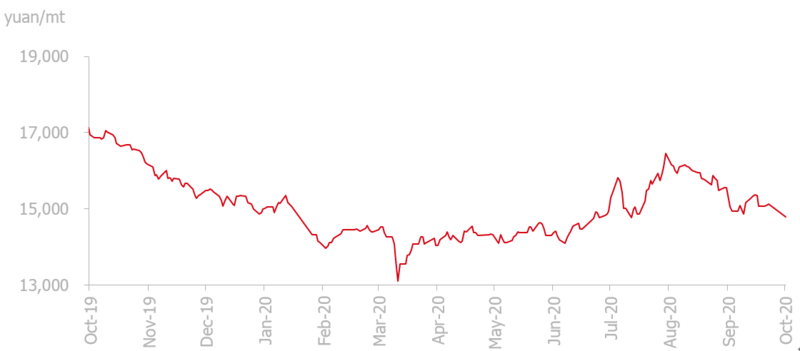

Lead domestic spot prices

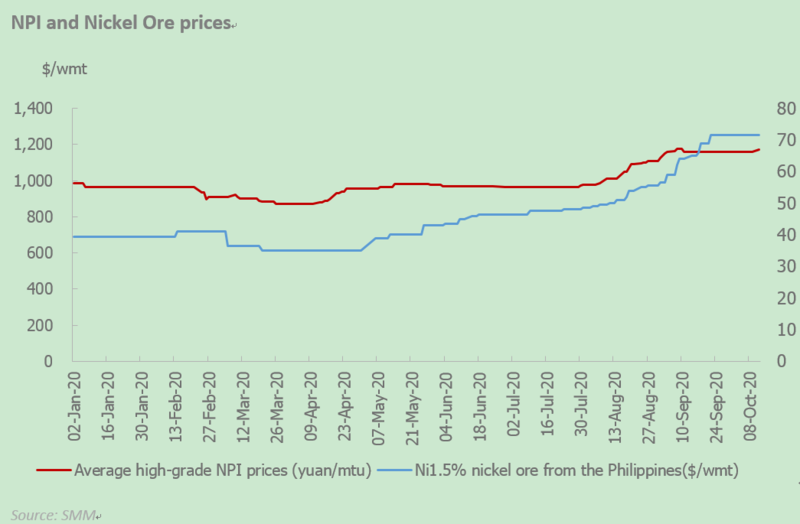

Nickel : Nickel ore supply tightened, high stainless steel demand supported prices

Nickel fundamentals strengthened in short term. Nickel ore prices were offered at high prices and supply is likely to tighten amid wet weather in Philippines, though port inventory of ore stocks has grown in recent weeks. NPI prices were supported by raw materials, while spot refined nickel destocked with economics of nickel as raw materials improving and stockpiling before the National Day holidays.

The purchasing manager's index (PMI) for downstream nickel industries was published before holidays. SMM data showed that PMI for stainless steel stood at 50.14 in September, down 2.54 points from August.

Stainless steel inventories were high as consumption was less than expected on the back of high output. Stainless steel plants are expected to stockpile in October as low inflow of nickel raw materials in September.

Tin: Overseas supply to decline

Downstream plants have suspended production for 3-8 days during the National Day holidays and have resumed operations. Tin supply in Myanmar is expected to decline amid rainy season and the increase in Covid-19 cases.

On the other hand, the most-traded SHFE tin prices over the December contract rose two days before the National Day holiday due to risk aversion sentiment, the exit of short-seller as well as pre-holiday restocking.

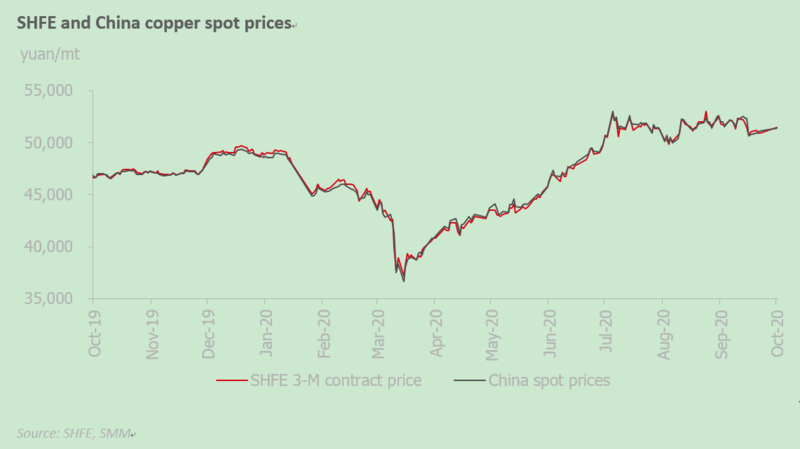

![Supply-demand Rebalancing Continues to Advance SHFE Copper Spot Discounts Gradually Stabilize [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/CaDcj20251217171711.jpg)