SHANGHAI, Aug 20 (SMM) - This is a roundup of China's metals weekly inventory as of August 20.

Primary Aluminium Inventories Rose 2,000 mt on Week

SMM data showed that China's social inventories of aluminium across eight consumption areas increased 2,000 mt on the week to 741,000 mt as of August 19.

The inventory increase mainly came from Gongyi. The inventories in Wuxi kept falling due to the lower arrivals.

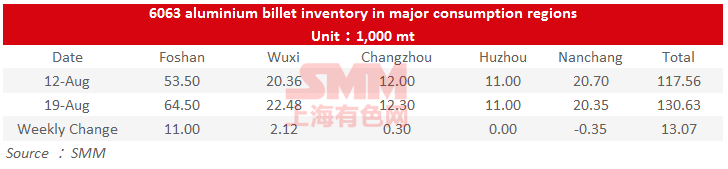

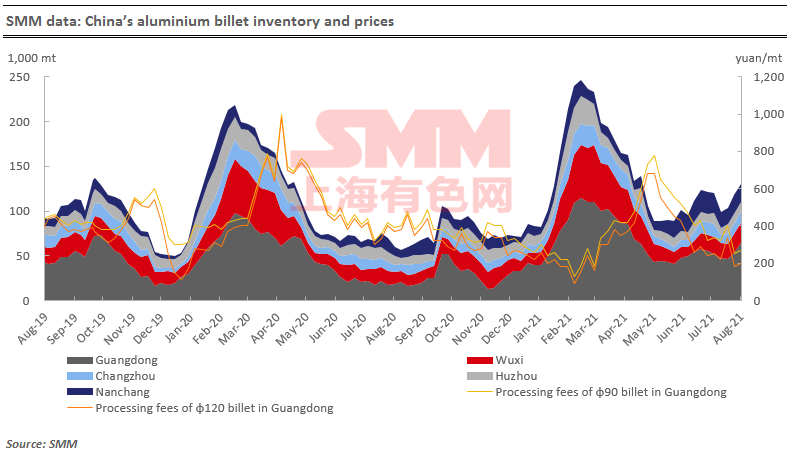

Aluminium Billet Inventories Up to 130,600 mt on Week

The stocks of aluminium billet in five major consumption areas increased by 13,100 mt to 130,600 mt on Thursday August 19 from the previous week, an increase of 11.1%.

Among them, only inventories in Nanchang fell on the week, while that in Huzhou was basically flat. Foshan saw the greatest increase of 11,000 mt or 20.56% on the week, followed by Wuxi with a rising volume of 2100 mt or 10.40%.

China HRC Inventory Up 17,900 mt on Week

SMM data showed that HRC stocks across social warehouses and steel makers rose 17,900 mt or 0.44% on the week, an increase of 3.64% than a year ago, to 4.04 million mt in the week ended August 19.

Inventories across social warehouses decreased 6,200 mt or 0.2% week on week to 3.07 million mt. This was 13.31% higher than the same period last year.

Stocks at Chinese steel makers came in at 973,000 mt, up 24,000 mt or 2.53% week on week but down 18.33% year on year.

Chinese Steel Rebar Fell 121,000 mt on Week

Inventories of rebar across Chinese steelmakers and social warehouses stood at 11.36 million mt as of August 19, down 121,000 mt or 1.1% from a week ago. Stocks are up 54,100 mt or 0.5% from a year earlier.

Inventories at Chinese steel makers fell 6,300 mt or 0.2% on the week and stood at 3.51 million mt. Stocks are down 12,600 mt or 0.4% from a year earlier.

Inventories at social warehouses declined 114,700 mt or 1.44% on the week and stood at 7.85 million mt, but up 66,700 mt or 0.9% from a year ago.

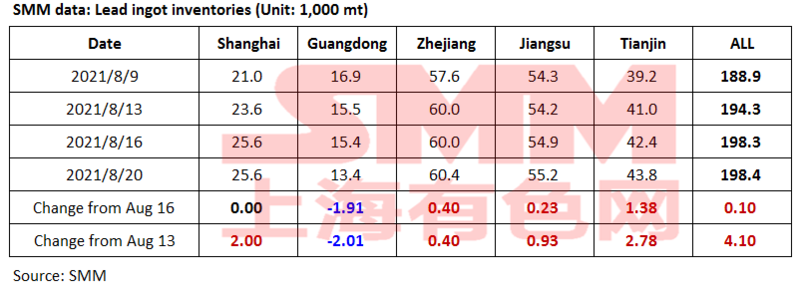

Lead Ingot Social Inventories Up 4,100 mt on Week

Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin increased 4,100 mt from August 13 and rose only 100 mt from August 16 to 198,400 mt as of August 20.

Lead prices fluctuated lower this week, while prices of lead-acid battery scrap stood high amid limited supply and higher transportation costs in the pandemic, so secondary lead prices were close to the costs. Secondary lead smelters held back cargoes, and some small plants in Anhui and Jiangxi reduced production, urging some downstream users with rigid demand to purchase primary lead. The increase in the lead ingot social inventories slowed down.

If lead prices continue to fluctuate at low levels, secondary lead smelters will be hard to regain profits, and the shipments and production will be slowed down simultaneously. The increase in the lead ingot inventories are expected to narrow further.

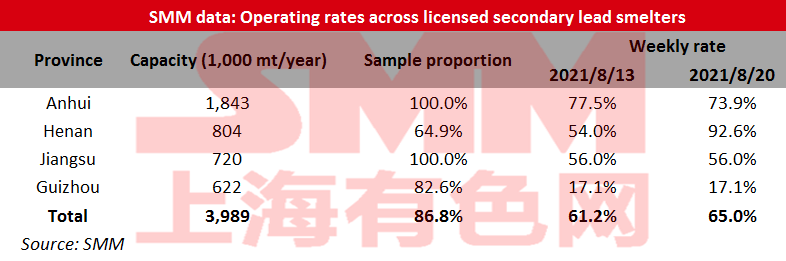

Operating Rates of Secondary Lead Smelters Up 3.84% on Week

Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 65.02% in the week ended August 20, up 3.84 percentage points from the previous week, showed an SMM survey.

The operating rates recovered on the week mainly due to the weakened impact of power curtailment in Henan, and Jinli resumed production early this week.

Lead prices fell this week, and some smelters in Anhui reduced production amid high battery scrap prices and lower profits. However, the production is recovering overall.

In addition to the sample companies, some smelters in Hebei also cut production due to the low profits, while the smelters in Jiangxi basically maintained normal production as the power curtailment was alleviated.

The companies under power rationing may continue to resume production next week. However, the inventories of lead ingots continued to rise this week, and lead prices fell, which may urge secondary lead smelters adjust production depending on the orders. The operating rate may not further increase next week.

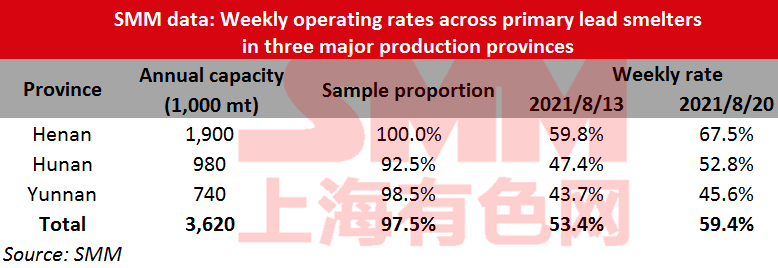

Operating Rates of Primary Lead Smelters Up 6% on Week

Operating rates across primary lead smelters in Henan, Hunan and Yunnan provinces gained 6 percentage points from the previous week to 59.4% in the week ended August 20, showed an SMM survey.

In Henan, Shibin, Yongning Gold Lead, and Wanyang resumed production after the power curtailment. Jinli recovered crude lead smelting and maintained normal production of refined lead.

Yongxing Zhongde in Hunan recovered production as the power rationing ended last week.

Yunnan Hongqian reduced production slightly for the maintenance next week. Another smelter in Yunnan resumed production this week. The production and supply of crude lead was suspended due to the accident in Chihong (Hulunbuir), but Chihong Yunnan still maintained normal production this week.

Anhui Tongguan resumed production as planned this week.

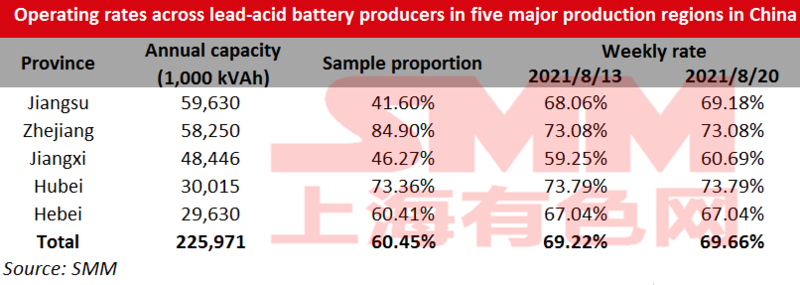

Operating Rates of Lead-acid Battery Plants Up 0.44% on Week

Operating rates across lead-acid battery producers in Jiangsu, Zhejiang, Jiangxi, Hubei and Hebei provinces gained 0.44 percentage point from August 13 to 69.66% as of August 20.

Replacement demand in the lead-acid battery market gradually improved, ad the orders for electric bicycle batteries increased. Operating rates mainly rose in Jiangsu and Jiangxi. The rebound in the consumption of car batteries was limited, and most car battery companies maintained the operating rates between 70-90%. Whether the lead-acid battery companies in Jiangsu will resume production after the pandemic control is loosened will be monitored.

Silicon Social Inventories Up 2,000 mt on Week

Social inventories of silicon metal across Huangpu port, Kunming city and Tianjin port shrank increased 2,000 mt from the previous week to 46,000 mt as of Friday August 20.

The stocks in Kunming increased seasonally, but the increment was lower than expected as most silicon plants were delivering goods for orders. The overall stocks in Tianjin Port and Huangpu Port stood flat on the week. The social inventories of silicon is expected to increase slightly next week.

Copper inventory in major Chinese markets fell 8,900 mt

As of Friday August 20, copper inventory across major Chinese markets fell 8,900 mt from Monday to 150,800 mt.

Copper inventories in Shanghai decreased 5,100 mt from Monday to 90,000 mt; copper inventories in Guangdong decreased by 4,800 mt from Monday to 43,500 mt; inventories in Chongqing and Tianjin both fell slightly; copper inventories in Jiangsu and Zhejiang grew 1,000 mt and 1,300 mt, respectively, from Monday.

Shanghai and Guangdong drove most of the decline. Limited influx of imported copper and stronger downstream buying interest amid lower copper prices accounted for the inventory decline in Shanghai area. Although power restrictions in Guangxi have improved, two smelters in the neighbouring regions of Guangdong halted production for maintenance. This combined with limited inflows of imported copper kept arriving shipments in Guangdong at low levels. This drove inventory declines in Guangdong.

SMM expects inventory declines to continue next week in view of strong copper cathode consumption amid a narrow price spread between copper cathode and copper scrap and an absence of sharp growth in arriving shipments.

Zinc Social Inventories Expanded 4500 mt on Week

Total zinc inventories across seven Chinese markets stood at 128,600 mt as of August 20, up 6,100 mt from August 16 and 4,500 mt from August 13.

Inventories in Shanghai increased as arrivals at smelters rose and imported zinc also flew into the market. Stocks in Guangdong increased as the power curtailment was eased at smelters and operating rates gradually rose. Inventories in Tianjin continued to decline as arrivals of cargoes fell and downstream producers properly restocked goods.

Inventories in Shanghai, Guangdong and Tianjin rose 3,800 mt, and inventories across seven Chinese markets increased 4,500 mt.

Copper Inventory in Shanghai Bonded Zone down 12,200 mt

Copper inventories in the Shanghai bonded zone decreased 12,200 mt from August 13 to 368,500 mt as of August 20, the sixth straight week of decline.

An improved SHFE/LME copper price ratio, driven by domestic electricity curtailment, shortage of copper scrap and limited inflow of imported cargoes, has incentivised customs clearances. Yangshan copper premiums surged amid tight supply, with the average premium under warrants surging over $50/mt in three trading days.

Continued imports under warrants are likely to drive further declines in bonded zone inventories.

Nickel Ore Inventories at Chinese Ports Increased to 5.92 Million wmt

Nickel ore inventory at Chinese ports grew 410,000 wmt to 5.92 million wmt as of August 20. Total Ni content stood at 46,500 mt. Total inventory at seven major ports stood at around 3.81 million wmt, an increase of 300,000 wmt from a week earlier.

This week, crew members at Tieshan port of Guangxi and Lianyungang port were infected with the COVID-19 pandemic. The vessels are currently quarantined. Affected by the pandemic, shipping schedules have been extended, and port offloading speed has slowed, limiting inventory growth.

In August, imports are likely to decline from July as some mining areas in the Philippines have gradually entered the wet season. As such, the possibility of significant accumulation in port inventory will be low.

Tight Domestic Supply of Nickel Plates Bolstered SHFE/LME Nickel Price Ratio

The SHFE/LME nickel price ratio rose this week amid tight spot supply of nickel plates. Lower nickel prices incentivised downstream buyers to restock, and this pushed spot premiums of nickel plate higher.

The opening of the import window drove inflows of nickel plate from bonded zone inventories. Meanwhile, arriving shipments of nickel briquette in the bonded zone stood at over 1,000 mt which are expected to enter the domestic warehouses next week. Spot premiums of nickel briquette are unlikely to improve.

Shipments of nickel plate that were expected to arrive have been delayed due to recent congestion at ports. Import premiums under warrants currently stand at high levels amid tight nickel plate supply. The current mainstream quotes stand at $220-250/mt, with $220-250/mt for Norwegian nickel under warrants. Import premiums for nickel briquette in the bonded zone stand at $230-240/mt.

![[SMM Analysis] Futures Lack Momentum to Rise Further, Pre-Holiday Demand Stalls, and Stainless Steel Social Inventory Accumulation Intensifies](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)